Request Customisation

Request Customisation

Home Healthcare Market Size, Growth, Share & Trends Analysis

Report Code

MD 1160

Published in

Aug, 2025, By MarketsandMarkets™

Home Healthcare Market by Product (Therapeutic, Testing, Screening, Monitoring, Mobility Care), Service (Nursing, Infusion Therapy, Rehabilitation, Palliative Care), Indication (Cancer, Diabetes, CVD, Respiratory, Wound Care) - Global Forecast to 2030

USD 473.76 Billion

MARKET SIZE, 2030

CAGR 8.9%

(2025-2030)

300

REPORT PAGES

295

MARKET TABLES

OVERVIEW

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

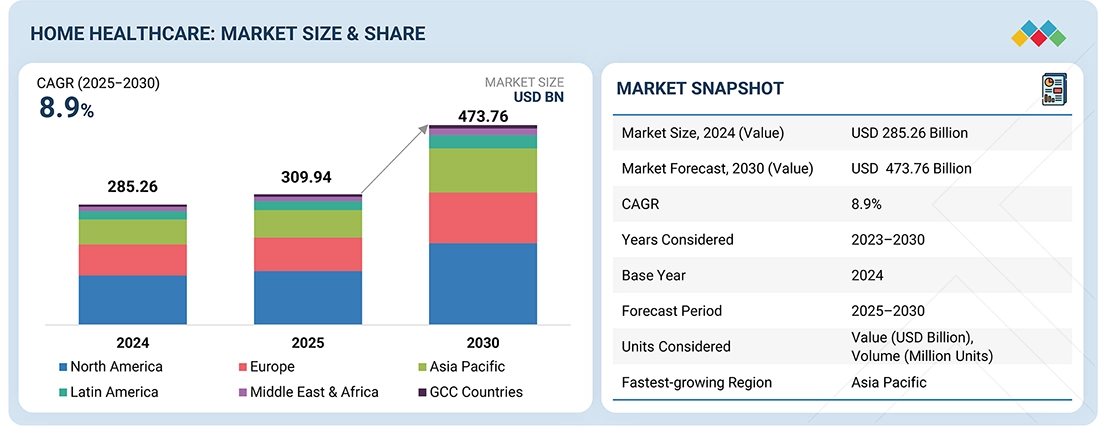

The global home healthcare market is projected to grow from USD 309.94 billion in 2025 to USD 473.76 billion by 2030, registering a strong CAGR of 8.9% during the forecast period. This growth is primarily driven by the expanding elderly population, which is at higher risk for chronic conditions such as hypertension, diabetes, and cardiovascular diseases, thereby increasing the demand for continuous care at home. The widespread adoption of telehealth and remote patient monitoring solutions is enhancing accessibility and convenience, while rising awareness of the importance of early diagnosis and preventive care is further fueling market demand. Moreover, innovations in home healthcare devices are improving ease of use and affordability, supporting greater adoption across both developed and emerging markets.

KEY TAKEAWAYS

-

BY REGIONThe Asia Pacific region is projected to register the highest CAGR during the forecast period. This growth is fueled by a rising prevalence of chronic diseases, an aging population, and increasing healthcare costs, which make home-based care a more practical and cost-effective option.

-

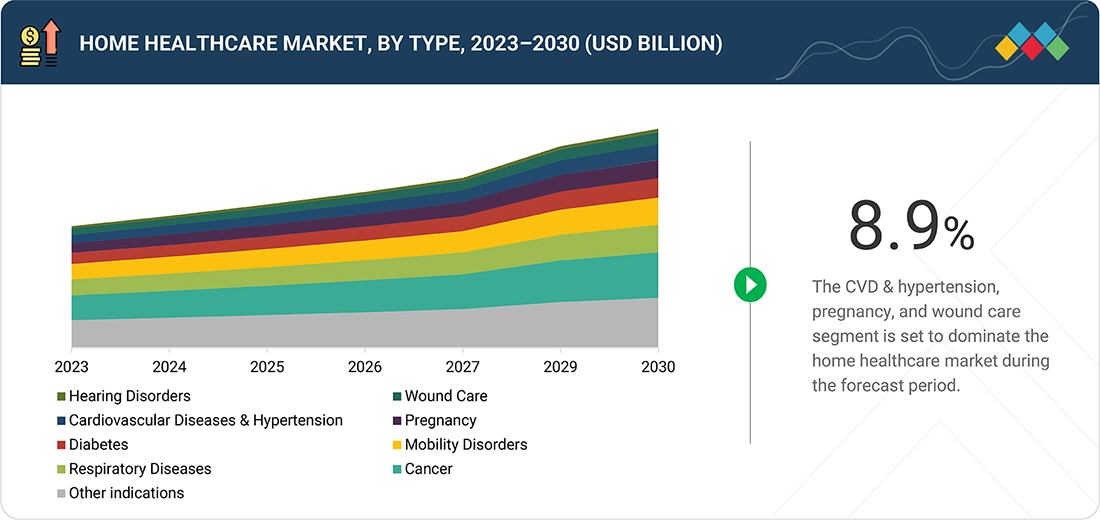

BY PRODUCTThe therapeutic products segment dominates, driven by the rising prevalence of chronic conditions such as kidney disease, sleep disorders, and respiratory illnesses like COPD.

-

BY SERVICESkilled nursing is estimated to account for the largest share, driven by growing demand for professional medical care at home.

-

BY indicationCancer is estimated to account for the largest share, driven by the increasing number of patients needing long-term treatment, palliative care, and symptom management at home.

-

COMPETITIVE LANDSCAPEKey market players have adopted a combination of organic and inorganic strategies, including product launches, partnerships, and acquisitions. Leading companies, such as Fresenius, Abbott, and Linde PLC, have expanded their service offerings and formed strategic collaborations to enhance home healthcare solutions and meet the growing demand for advanced, patient-centric care at home.

The home healthcare market is estimated to experience substantial growth over the coming decade, driven by the increasing elderly population and the rising incidence of chronic diseases. Older adults are particularly vulnerable to conditions such as heart disease, diabetes, arthritis, and respiratory disorders, which often necessitate continuous care and routine monitoring. Moreover, lifestyle changes, poor nutrition, and insufficient physical activity are contributing to a growing prevalence of chronic health issues across all age groups. These factors are fueling demand for personalized, cost-efficient healthcare that can be provided in the comfort of patients’ homes. As a result, home healthcare is becoming a favored solution, delivering convenience, affordability, and an improved quality of life for individuals managing long-term health conditions.

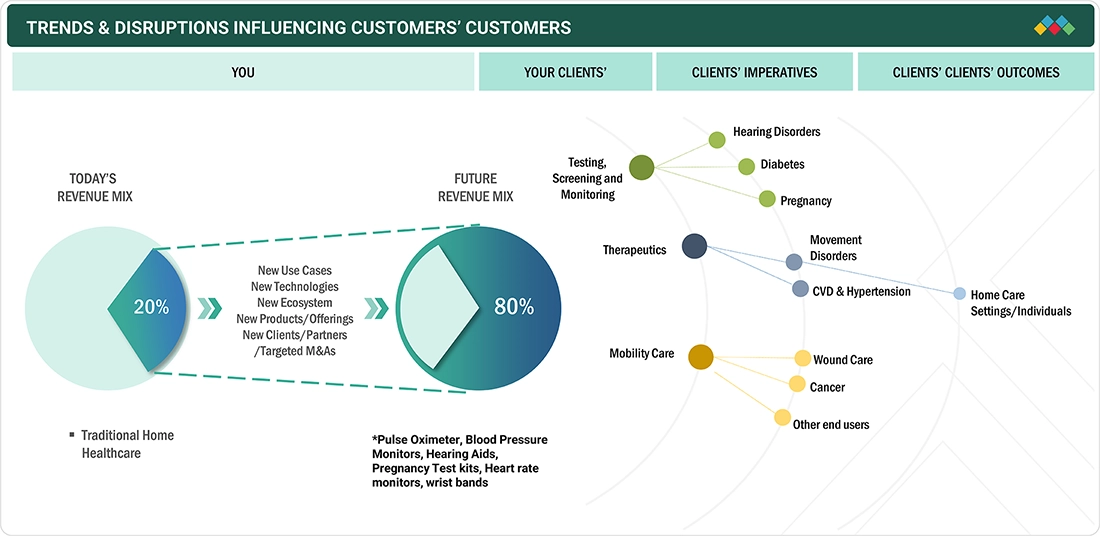

TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' CUSTOMERS

The impact on service providers arises from evolving customer trends and market disruptions. Home healthcare service providers/individuals are the primary clients of home healthcare solution manufacturers. Changes in healthcare delivery models, patient preferences, and technological adoption can directly influence the revenues of both end users and home healthcare product and service providers.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

MARKET DYNAMICS

Drivers

Impact

Level

Level

-

Growing elderly population and rising incidence of chronic disease

-

Rapid technological advancements

RESTRAINTS

Impact

Level

Level

-

Changing reimbursement policies

-

Limited insurance Coverage

OPPORTUNITIES

Impact

Level

Level

-

Rising focus on telehealth

-

Growing preference for home-based treatments

CHALLENGES

Impact

Level

Level

-

Shortage of home care workers

-

Lack of supporting infrastructure

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Driver: Growing elderly population and rising incidence of chronic disease

The global elderly population, especially those over 85, is set to more than double, driving demand for healthcare services. Home healthcare is increasingly preferred for its ability to reduce hospital visits, lower costs, and provide care at home. Chronic diseases like cardiovascular conditions, cancer, diabetes, and respiratory disorders affect many patients, and home-based care helps manage these illnesses, improve quality of life, and ease the burden on hospitals. Rising geriatric populations and chronic disease prevalence are expected to accelerate global demand for home healthcare and continuous monitoring.

Restraint: Changing reimbursement policies

CMS has revised home healthcare reimbursement through the Patient-Driven Groupings Model, focusing on patient acuity and clinical needs while reducing payment rates, which can impact smaller and rural providers. Value-based programs now emphasize outcomes, social factors, and discharge planning. Durable medical equipment, like home ventilators, is reimbursed on a rental basis, but gaps remain between actual costs and coverage. Reduced reimbursement for diagnostic testing has also slowed technology adoption and delayed accurate diagnoses, creating challenges for patient care.

Opportunity: Rising focus on telehealth

Telehealth is reshaping home healthcare by enabling remote patient monitoring, virtual consultations, and early interventions. Tools like mHealth apps, video consultations, and connected devices allow providers to assess conditions, prescribe treatments, and follow up without in-person visits, improving convenience and reducing costs by shifting care from expensive settings to virtual platforms. Globally, supportive policies and digital infrastructure—such as 5G, high-resolution devices, and electronic health records—are accelerating telehealth adoption, creating new opportunities for providers to enhance care and expand services.

Challenge: Shortage of home care workers

The home healthcare industry is expanding rapidly, driving strong demand for personal care and home health aides. Despite this growth, attracting and retaining workers remains a challenge due to low compensation, making the profession less appealing, especially to younger job seekers. As a result, the supply of qualified home care workers often falls short of demand, posing challenges for providers in delivering consistent, high-quality care.

Home Healthcare Market: COMMERCIAL USE CASES ACROSS INDUSTRIES

| COMPANY | USE CASE DESCRIPTION | BENEFITS |

|---|---|---|

|

Home dialysis systems (peritoneal dialysis and home hemodialysis) | Improves patient convenience, reduces hospital visits, enhances quality of life, and lowers long-term treatment costs |

|

Remote cardiac monitoring and glucose monitoring devices for home use | Enables continuous monitoring, supports early detection, empowers self-management of chronic conditions, and improves clinical outcomes |

|

Home oxygen therapy and respiratory support solutions | Provides reliable long-term respiratory care, increases mobility and independence for patients, and reduces hospital readmissions |

|

Home-based diagnostic tests (e.g., diabetes and infectious disease self-testing kits) | Facilitates early diagnosis, expands patient access to testing, enhances treatment adherence, and reduces pressure on healthcare facilities |

|

Home sleep apnea therapy devices, including CPAP and BiPAP systems | Improves sleep quality, reduces cardiovascular risks, enhances patient compliance, and delivers real-time data for remote clinician monitoring |

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

MARKET ECOSYSTEM

The home healthcare market ecosystem comprises raw material suppliers (DuPont, Qmed, Avantor), device and equipment manufacturers (Fresenius Medical Care AG, Abbott, Linde PLC), and end users (Care UK, LHC Group). Raw materials, including plastics, electronic components, and specialized medical-grade materials, are processed into reliable, high-performance home healthcare devices. End users drive demand for safety, durability, and ease of use, while manufacturers deliver precision-engineered solutions that meet these needs. Collaboration across the value chain is crucial for fostering innovation and driving market growth.

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

MARKET SEGMENTS

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Home Healthcare Market, by Product

The therapeutic products segment leads, driven by the growing prevalence of chronic diseases like kidney failure, respiratory disorders, cardiovascular conditions, and diabetes. Home-based therapeutic equipment reduces hospital visits, improves patient comfort and compliance, and enhances quality of life. Advances in compact, user-friendly medical devices, along with supportive reimbursement policies, are further boosting adoption, making this segment a key growth driver in the home healthcare market.

Home Healthcare Market, by Service

Skilled nursing services hold the largest share of the home healthcare market, driven by the growing need for professional medical care at home. Licensed nurses provide services such as medication administration, wound care, chronic condition monitoring, and post-surgical support. Rising elderly populations and an increasing number of patients with complex health needs are fueling demand. As healthcare systems emphasize cost-effective, patient-centered care, the shift toward home-based services is accelerating, making skilled nursing a central component of the expanding home healthcare industry.

Home Healthcare Market, by Indication

Among various medical indications, the cancer segment held the largest share of the home healthcare market in 2024, driven by the rising global cancer burden and increasing preference for home-based care. Home oncology services are particularly important for patients in advanced stages or those recovering after treatment. Growing awareness of palliative and supportive care is also encouraging families to opt for at-home services, providing a more personalized and dignified experience for patients.

REGION

Asia Pacific to be fastest-growing region in global home healthcare market during forecast period

During the forecast period, Asia Pacific is projected to experience the fastest growth in home healthcare, driven by a surge in chronic illnesses, an aging demographic, and escalating healthcare costs, which favor home-based care solutions. Enhanced government initiatives, improved access to rural healthcare, and rising investments in healthcare infrastructure and digital technologies are further boosting the uptake of home healthcare across nations.

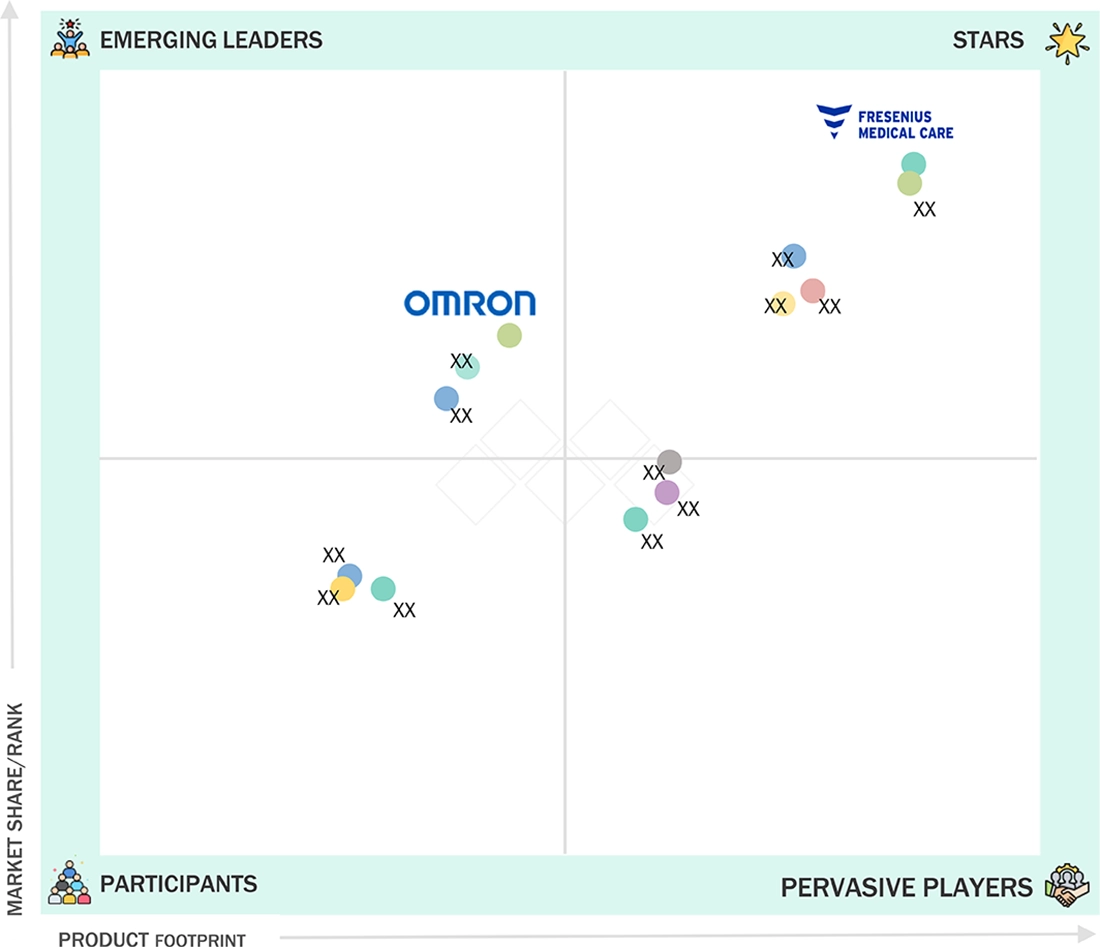

Home Healthcare Market: COMPANY EVALUATION MATRIX

In the home healthcare market matrix, Fresenius Medical Care (Star) leads with a strong market share and a wide-ranging product portfolio, driven by its advanced and reliable home healthcare devices widely adopted in hospitals and home care settings. Omron (Emerging Leader) is gaining recognition with its innovative and specialized home healthcare solutions, strengthening its position through targeted product offerings and technology advancements. While Fresenius dominates through scale and a diverse portfolio, Omron shows significant potential to move toward the leaders’ quadrant as demand for high-quality, user-friendly home healthcare devices continues to grow.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

KEY MARKET PLAYERS

- Fresenius Medical Care AG (Germany)

- Abbott (US)

- Linde plc (Ireland)

- F. Hoffmann-La Roche, Ltd. (Switzerland)

- ResMed (US)

- Koninklijke Philips N.V. (Netherlands)

- GE Healthcare (US)

- A&D HOLON Holdings Company, Limited (Japan)

- Convatec Group PLC (UK)

- Amedisys (US)

- OMRON Healthcare Co., Ltd. (Japan)

- Invacare Corporation (US)

- BAYADA Home Health Care (US)

- Drive DeVilbiss Healthcare (UK)

- Sunrise Medical (Germany)

MARKET SCOPE

| REPORT METRIC | DETAILS |

|---|---|

| Market Size, 2024 (Value) | USD 285.26 Billion |

| Market Forecast, 2030 (Value) | USD 473.76 Billion |

| Growth Rate | CAGR of 8.9% from 2025 to 2030 |

| Years Considered | 2023–2030 |

| Base Year | 2024 |

| Forecast Period | 2025–2030 |

| Units Considered | Value (USD Billion), Volume (Million Units) |

| Report Coverage | Revenue Forecast, Company Ranking, Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa, GCC Countries |

WHAT IS IN IT FOR YOU: Home Healthcare Market REPORT CONTENT GUIDE

DELIVERED CUSTOMIZATIONS

We have successfully delivered the following deep-dive customizations:

| CLIENT REQUEST | CUSTOMIZATION DELIVERED | VALUE ADDS |

|---|---|---|

| Healthcare Leader |

|

|

| Major Player in Home Healthcare |

|

Highlight adoption patterns of home healthcare technologies, end-user preferences, and regulatory impacts on product deployment |

RECENT DEVELOPMENTS

- August 2024 : Abbott (US) announced a global partnership with Medtronic (Ireland) to develop an integrated continuous glucose monitoring (CGM) system, strengthening home diabetes care solutions.

- May 2024 : Liberty Dialysis Hawaii, an affiliate of Fresenius Medical Care AG (Germany), opened its first home hemodialysis patient training center in Windward O'ahu, Hawai'i, expanding home care services.

- April 2024 : Fresenius Medical Care AG (Germany) launched the latest generation of its home dialysis system, NxStage Versi HD with GuideMe Software, enhancing patient convenience and monitoring capabilities.

- May 2023 : ResMed (US) acquired Somnoware Software (US), a provider of sleep and respiratory care diagnostics software, to enhance its home care technology offerings.

Table of Contents

![]() Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

TITLE

PAGE NO

1

INTRODUCTION

28

2

RESEARCH METHODOLOGY

32

3

EXECUTIVE SUMMARY

43

4

PREMIUM INSIGHTS

47

5

MARKET OVERVIEW

Evolving healthcare market driven by tech, aging population, and personalized, cost-effective care demands.

51

5.1

INTRODUCTION

5.2

MARKET DYNAMICS

5.2.1

DRIVERS

5.2.1.1

Growing elderly population and rising incidence of chronic diseases

5.2.1.2

Rapid technological advancements

5.2.1.3

Need for cost-effective healthcare delivery

5.2.1.4

Increased preference for personalized care

5.2.2

RESTRAINTS

5.2.2.1

Changing reimbursement policies

5.2.2.2

Limited insurance coverage

5.2.2.3

Patient safety concerns

5.2.3

OPPORTUNITIES

5.2.3.1

Rising focus on telehealth

5.2.3.2

Growing preference for home-based treatments

5.2.4

CHALLENGES

5.2.4.1

Shortage of home care workers

5.2.4.2

Lack of supporting infrastructure

5.3

TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4

PRICING ANALYSIS

5.4.1

AVERAGE SELLING PRICE TREND, BY PRODUCT

5.4.2

AVERAGE SELLING PRICE TREND, BY KEY PLAYER

5.4.3

AVERAGE SELLING PRICE TREND, BY REGION

5.5

VALUE CHAIN ANALYSIS

5.6

SUPPLY CHAIN ANALYSIS

5.7

ECOSYSTEM ANALYSIS

5.8

INVESTMENT AND FUNDING SCENARIO

5.9

TECHNOLOGY ANALYSIS

5.9.1

KEY TECHNOLOGIES

5.9.1.1

Vital sign monitoring devices

5.9.1.2

Wearable devices

5.9.2

COMPLEMENTARY TECHNOLOGIES

5.9.2.1

Health data platforms

5.9.2.2

Medication management system

5.9.3

ADJACENT TECHNOLOGIES

5.9.3.1

Augmented Reality and Virtual Reality (AR/VR)

5.10

PATENT ANALYSIS

5.11

TRADE ANALYSIS

5.11.1

IMPORT DATA (HS CODE 901890)

5.11.2

EXPORT DATA (HS CODE 901890)

5.12

KEY CONFERENCES AND EVENTS, 2025–2026

5.13

REGULATORY LANDSCAPE

5.13.1

REGULATORY ANALYSIS

5.13.1.1

North America

5.13.1.2

Europe

5.13.1.3

Asia Pacific

5.13.2

REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.14

PORTER’S FIVE FORCES ANALYSIS

5.14.1

BARGAINING POWER OF SUPPLIERS

5.14.2

BARGAINING POWER OF BUYERS

5.14.3

THREAT OF NEW ENTRANTS

5.14.4

THREAT OF SUBSTITUTES

5.14.5

INTENSITY OF COMPETITIVE RIVALRY

5.15

KEY STAKEHOLDERS AND BUYING CRITERIA

5.15.1

KEY STAKEHOLDERS IN BUYING PROCESS

5.15.2

BUYING CRITERIA

5.16

IMPACT OF AI ON HOME HEALTHCARE MARKET

5.16.1

INTRODUCTION

5.16.2

MARKET POTENTIAL OF AI IN HOME HEALTHCARE MARKET

5.16.3

AI USE CASES

5.16.4

KEY COMPANIES IMPLEMENTING AI

5.16.5

FUTURE OF AI IN HOME HEALTHCARE MARKET

5.17

ADJACENT MARKETS FOR HOME HEALTHCARE MARKET

5.18

IMPACT OF US TARIFF REGULATION ON HOME HEALTHCARE MARKET

5.18.1

INTRODUCTION

5.18.2

KEY TARIFF RATES

5.18.3

PRICE IMPACT ANALYSIS

5.18.4

KEY IMPACT ON COUNTRY/REGION

5.18.4.1

North America

5.18.4.2

Europe

5.18.4.3

Asia Pacific

5.18.5

IMPACT ON END-USE INDUSTRIES

5.18.5.1

Home healthcare providers

6

HOME HEALTHCARE MARKET, BY PRODUCT

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million and Units | 48 Data Tables

90

6.1

INTRODUCTION

6.2

THERAPEUTIC PRODUCTS

6.2.1

DIALYSIS EQUIPMENT

6.2.1.1

Favorable reimbursement scenario for home dialysis to favor growth

6.2.2

WOUND CARE PRODUCTS

6.2.2.1

Rising geriatric population and subsequent incidence of chronic diseases to amplify growth

6.2.3

IV EQUIPMENT

6.2.3.1

Technological advancements in IV therapy to contribute to growth

6.2.4

SLEEP APNEA THERAPEUTIC DEVICES

6.2.4.1

Increasing patient preference for home-based sleep tests to bolster growth

6.2.5

INSULIN DELIVERY DEVICES

6.2.5.1

High incidence of diabetes to favor growth

6.2.6

OXYGEN DELIVERY SYSTEMS

6.2.6.1

Growing trend of using oxygen therapy for respiratory disorders to propel market

6.2.7

INHALERS

6.2.7.1

High incidence of asthma to stimulate growth

6.2.8

NEBULIZERS

6.2.8.1

Faster relief and longer symptom control to accelerate growth

6.2.9

VENTILATORS

6.2.9.1

Growing use of positive airway pressure devices for sleep apnea therapy to drive market

6.2.10

OTHER THERAPEUTIC PRODUCTS

6.3

TESTING, SCREENING, AND MONITORING PRODUCTS

6.3.1

BLOOD GLUCOSE MONITORS

6.3.1.1

Increasing preference for self-diagnosis to contribute to growth

6.3.2

HEARING AIDS

6.3.2.1

High incidence of hearing impairment to augment growth

6.3.3

ACTIVITY MONITORS & WRISTBANDS

6.3.3.1

Increasing awareness about health and fitness to sustain growth

6.3.4

ECG/EKG DEVICES

6.3.4.1

High prevalence of cardiovascular diseases to support growth

6.3.5

TEMPERATURE MONITORING DEVICES

6.3.5.1

Rising use of digital thermometers for quick and accurate results to aid growth

6.3.6

HEART RATE MONITORS

6.3.6.1

Need for real-time monitoring to advance growth

6.3.7

PULSE OXIMETERS

6.3.7.1

Rising disease incidence and wide usage of pulse oximetry to promote growth

6.3.8

OVULATION & PREGNANCY TEST KITS

6.3.8.1

Privacy, convenience, accessibility, and quick results to facilitate growth

6.3.9

BLOOD PRESSURE MONITORS

6.3.9.1

Growing integration of pressure monitoring devices with digital health platforms to boost market

6.3.10

HIV TEST KITS

6.3.10.1

Increasing number of HIV-infected individuals globally to favor growth

6.3.11

FETAL MONITORING DEVICES

6.3.11.1

Increasing reliance on remote-based care to promote growth

6.3.12

HOLTER & EVENT MONITORS

6.3.12.1

Portability and storage attributes to aid growth

6.3.13

DRUG & ALCOHOL TEST KITS

6.3.13.1

Rise in drug abuse and alcohol consumption to support growth

6.3.14

COAGULATION MONITORING PRODUCTS

6.3.14.1

Rising incidence of deep vein thrombosis, pulmonary embolism, and hemophilia to foster growth

6.3.15

PEAK FLOW METERS

6.3.15.1

High portability and cost-efficiency to increase adoption

6.3.16

COLON CANCER TEST KITS

6.3.16.1

High incidence of colorectal cancer to drive market

6.3.17

EEG DEVICES

6.3.17.1

Wide patient population for epilepsy to fuel market

6.3.18

HOME SLEEP TESTING DEVICES

6.3.18.1

Need for specialized care at home to spur growth

6.3.19

CHOLESTEROL TESTING PRODUCTS

6.3.19.1

Rising obesity levels and cardiovascular incidence to augment growth

6.3.20

HOME HBA1C TEST KITS

6.3.20.1

Increasing recommendations for regular testing and favorable clinical outcomes to aid growth

6.4

MOBILITY CARE PRODUCTS

6.4.1

WHEELCHAIRS

6.4.1.1

Need for patient mobility with less pain and fatigue to fuel market

6.4.2

MOBILITY SCOOTERS

6.4.2.1

Increasing demand for mobility-assisted devices to facilitate growth

6.4.3

WALKERS & ROLLATORS

6.4.3.1

Rising prevalence for gait disorders, osteoarthritis, and other degenerative joint diseases to aid growth

6.4.4

CRUTCHES

6.4.4.1

Increasing use of crutches during post-operative recovery to boost market

6.4.5

CANES

6.4.5.1

Low cost, ease of use, and wide availability to contribute to growth

7

HOME HEALTHCARE MARKET, BY SERVICE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 9 Data Tables

135

7.1

INTRODUCTION

7.2

SKILLED NURSING SERVICES

7.2.1

NEED FOR SPECIFIC PLAN OF CARE TO PROMOTE GROWTH

7.3

REHABILITATION THERAPY SERVICES

7.3.1

RISING DEMAND FOR IN-HOME CARE PERSONNEL TO STIMULATE GROWTH

7.4

HOSPICE & PALLIATIVE CARE SERVICES

7.4.1

INCREASING GERIATRIC POPULATION TO FACILITATE GROWTH

7.5

UNSKILLED CARE SERVICES

7.5.1

HIGHER AFFORDABILITY THAN HOSPITAL OR NURSING HOME SERVICES TO AID GROWTH

7.6

RESPIRATORY THERAPY SERVICES

7.6.1

GROWING PREVALENCE OF RESPIRATORY DISORDERS TO DRIVE MARKET

7.7

INFUSION THERAPY SERVICES

7.7.1

SAFE AND EFFECTIVE ALTERNATIVE TO INPATIENT CARE TO ENCOURAGE GROWTH

7.8

PREGNANCY CARE SERVICES

7.8.1

NEED FOR BETTER MANAGEMENT OF HIGH-RISK PREGNANCIES AND COMPLICATIONS TO ENSURE GROWTH

8

HOME HEALTHCARE MARKET, BY INDICATION

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 12 Data Tables

146

8.1

INTRODUCTION

8.2

CANCER

8.2.1

INCREASING PREFERENCE FOR AT-HOME TREATMENT TO EXPEDITE GROWTH

8.3

RESPIRATORY DISEASES

8.3.1

RISING INCIDENCE OF CHRONIC DISEASES TO SUSTAIN GROWTH

8.4

MOBILITY DISORDERS

8.4.1

GROWING GERIATRIC POPULATION TO BOOST MARKET

8.5

PREGNANCY

8.5.1

RISING FOCUS ON BETTER CARE AND MONITORING DURING PREGNANCY TO AID GROWTH

8.6

CARDIOVASCULAR DISEASES & HYPERTENSION

8.6.1

GROWING HEALTH AWARENESS TO DRIVE MARKET

8.7

WOUND CARE

8.7.1

INCREASING NUMBER OF ROAD ACCIDENTS AND TRAUMA INJURIES TO BOLSTER GROWTH

8.8

DIABETES

8.8.1

SHIFT IN CONSUMER PREFERENCE FROM TRADITIONAL TO MULTIFUNCTIONAL BLOOD GLUCOSE METERS TO SPUR GROWTH

8.9

HEARING DISORDERS

8.9.1

WORLDWIDE INCREASE IN HEARING DISABILITIES TO FOSTER GROWTH

8.10

OTHER INDICATIONS

9

HOME HEALTHCARE MARKET, BY REGION

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 136 Data Tables

158

9.1

INTRODUCTION

9.2

NORTH AMERICA

9.2.1

MACROECONOMIC OUTLOOK FOR NORTH AMERICA

9.2.2

US

9.2.2.1

Significant demographic change to contribute to growth

9.2.3

CANADA

9.2.3.1

Growing elderly population to drive market

9.3

EUROPE

9.3.1

MACROECONOMIC OUTLOOK FOR EUROPE

9.3.2

GERMANY

9.3.2.1

Increasing demand for healthcare services to bolster growth

9.3.3

UK

9.3.3.1

Aging population and rising patient pool to expedite growth

9.3.4

FRANCE

9.3.4.1

Favorable government support to boost market

9.3.5

ITALY

9.3.5.1

Universal eligibility for home care to favor growth

9.3.6

SPAIN

9.3.6.1

Upsurge in elderly population to accelerate growth

9.3.7

REST OF EUROPE

9.4

ASIA PACIFIC

9.4.1

MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

9.4.2

JAPAN

9.4.2.1

High life expectancy and growing healthcare innovations to fuel market

9.4.3

CHINA

9.4.3.1

Increasing cases of diabetes and diabetic foot ulcers to favor growth

9.4.4

INDIA

9.4.4.1

Rising disposable income and focus on personalized care to spur growth

9.4.5

REST OF ASIA PACIFIC

9.5

LATIN AMERICA

9.5.1

RISING HEALTHCARE NEEDS TO AID GROWTH

9.5.2

MACROECONOMIC OUTLOOK FOR LATIN AMERICA

9.6

MIDDLE EAST & AFRICA

9.6.1

GROWING INVESTMENTS IN HEALTHCARE INFRASTRUCTURE TO PROPEL MARKET

9.6.2

MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

9.7

GCC COUNTRIES

9.7.1

DIGITAL TRANSFORMATION AND EXPANDING PUBLIC-PRIVATE PARTNERSHIPS TO FUEL MARKET

9.7.2

MACROECONOMIC OUTLOOK FOR GCC COUNTRIES

10

COMPETITIVE LANDSCAPE

Discover strategic maneuvers and market dominance tactics shaping the competitive landscape in 2024.

258

10.1

OVERVIEW

10.2

KEY PLAYER STRATEGIES/RIGHT TO WIN

10.2.1

OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS

10.3

REVENUE ANALYSIS, 2022–2024

10.4

MARKET SHARE ANALYSIS, 2024

10.5

COMPANY VALUATION AND FINANCIAL METRICS

10.6

BRAND/PRODUCT COMPARISON

10.7

COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

10.7.1

STARS

10.7.2

EMERGING LEADERS

10.7.3

PERVASIVE PLAYERS

10.7.4

PARTICIPANTS

10.7.5

COMPANY FOOTPRINT: KEY PLAYERS, 2024

10.7.5.1

Company footprint

10.7.5.2

Region footprint

10.7.5.3

Product & service footprint

10.7.5.4

Product footprint

10.7.5.5

End-user footprint

10.8

COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

10.8.1

PROGRESSIVE COMPANIES

10.8.2

RESPONSIVE COMPANIES

10.8.3

DYNAMIC COMPANIES

10.8.4

STARTING BLOCKS

10.8.5

COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

10.8.5.1

Detailed list of key startups/SMEs

10.8.5.2

Competitive benchmarking of key startups/SMEs

10.9

COMPETITIVE SCENARIO

10.9.1

PRODUCT LAUNCHES AND APPROVALS

10.9.2

DEALS

10.9.3

EXPANSIONS

11

COMPANY PROFILES

In-depth Company Profiles of Leading Market Players with detailed Business Overview, Product and Service Portfolio, Recent Developments, and Unique Analyst Perspective (MnM View)

280

11.1

KEY PLAYERS

11.1.1

FRESENIUS MEDICAL CARE AG

11.1.1.1

Business overview

11.1.1.2

Products/Solutions/Services offered

11.1.1.3

Recent developments

11.1.1.4

MnM view

11.1.2

ABBOTT

11.1.3

LINDE PLC

11.1.4

F. HOFFMANN-LA ROCHE LTD

11.1.5

RESMED

11.1.6

KONINKLIJKE PHILIPS N.V.

11.1.7

GE HEALTHCARE

11.1.8

A&D HOLON HOLDINGS COMPANY, LIMITED

11.1.9

CONVATEC GROUP PLC

11.1.10

AMEDISYS

11.1.11

OMRON HEALTHCARE CO., LTD.

11.2

OTHER PLAYERS

11.2.1

INVACARE CORPORATION

11.2.2

BAYADA HOME HEALTH CARE

11.2.3

DRIVE DEVILBISS HEALTHCARE

11.2.4

SUNRISE MEDICAL

11.2.5

ROMA MEDICAL

11.2.6

CAREMAX REHABILITATION EQUIPMENT CO., LTD.

11.2.7

VITALOGRAPH

11.2.8

ADVITA PFLEGEDIENST GMBH

11.2.9

THE RENAFAN GROUP

11.2.10

CONTEC MEDICAL SYSTEMS CO., LTD.

11.2.11

B. BRAUN SE

11.2.12

BAXTER

11.2.13

MEDLINE INDUSTRIES

11.2.14

ADVIN HEALTH CARE

12

APPENDIX

341

12.1

DISCUSSION GUIDE

12.2

KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

12.3

CUSTOMIZATION OPTIONS

12.4

RELATED REPORTS

12.5

AUTHOR DETAILS

LIST OF TABLES

TABLE 1

HOME HEALTHCARE MARKET: INCLUSIONS AND EXCLUSIONS

TABLE 2

HOME HEALTHCARE MARKET: RISK ANALYSIS

TABLE 3

GERIATRIC POPULATION, 2022 VS. 2050 (MILLION)

TABLE 4

PRODUCT LAUNCHES BY KEY PLAYERS, 2022–2024

TABLE 5

AVERAGE SELLING PRICING TREND OF HOME HEALTHCARE PRODUCTS, BY TYPE, 2023–2025 (USD)

TABLE 6

AVERAGE SELLING PRICE TREND OF HOME HEALTHCARE PRODUCTS, BY KEY PLAYER, 2023–2025 (USD)

TABLE 7

AVERAGE SELLING PRICE TREND OF HOME HEALTHCARE PRODUCTS, BY REGION, 2023–2025 (USD)

TABLE 8

HOME HEALTHCARE MARKET: ROLE OF COMPANIES IN ECOSYSTEM

TABLE 9

HOME HEALTHCARE MARKET: INNOVATIONS AND PATENT REGISTRATIONS, 2024

TABLE 10

IMPORT DATA FOR HS CODE 901890, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 11

EXPORT DATA FOR HS CODE 901890, BY COUNTRY, 2020–2024 (USD MILLION)

TABLE 12

HOME HEALTHCARE MARKET: KEY CONFERENCES AND EVENTS, 2025–2026

TABLE 13

US FDA: CLASSIFICATION OF MEDICAL DEVICES

TABLE 14

US: MEDICAL DEVICE REGULATORY APPROVAL PROCESS

TABLE 15

CANADA: MEDICAL DEVICE REGULATORY APPROVAL PROCESS

TABLE 16

JAPAN: CLASSIFICATION OF MEDICAL DEVICES AND REVIEWING BODIES

TABLE 17

CHINA: CLASSIFICATION OF MEDICAL DEVICES

TABLE 18

NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 19

EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 20

ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 21

LATIN AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 22

REST OF THE WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 23

HOME HEALTHCARE MARKET: PORTER’S FIVE FORCES ANALYSIS

TABLE 24

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS OF HOME HEALTHCARE PRODUCTS (%)

TABLE 25

KEY BUYING CRITERIA FOR HOME HEALTHCARE PRODUCTS

TABLE 26

US ADJUSTED RECIPROCAL TARIFF RATES

TABLE 27

HOME HEALTHCARE MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 28

KEY THERAPEUTIC PRODUCTS OFFERED

TABLE 29

HOME HEALTHCARE MARKET FOR THERAPEUTIC PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 30

HOME HEALTHCARE MARKET FOR THERAPEUTIC PRODUCTS, BY REGION, 2023–2030 (USD MILLION)

TABLE 31

HOME HEALTHCARE MARKET FOR DIALYSIS EQUIPMENT, BY REGION, 2023–2030 (USD MILLION)

TABLE 32

HOME HEALTHCARE MARKET FOR WOUND CARE PRODUCTS, BY REGION, 2023–2030 (USD MILLION)

TABLE 33

HOME HEALTHCARE MARKET FOR IV EQUIPMENT, BY REGION, 2023–2030 (USD MILLION)

TABLE 34

HOME HEALTHCARE MARKET FOR SLEEP APNEA THERAPEUTIC DEVICES, BY REGION, 2023–2030 (USD MILLION)

TABLE 35

HOME HEALTHCARE MARKET FOR INSULIN DELIVERY DEVICES, BY REGION, 2023–2030 (USD MILLION)

TABLE 36

HOME HEALTHCARE MARKET FOR OXYGEN DELIVERY SYSTEMS, BY REGION, 2023–2030 (USD MILLION)

TABLE 37

HOME HEALTHCARE MARKET FOR INHALERS, BY REGION, 2023–2030 (USD MILLION)

TABLE 38

HOME HEALTHCARE MARKET FOR NEBULIZERS, BY REGION, 2023–2030 (USD MILLION)

TABLE 39

HOME HEALTHCARE MARKET FOR VENTILATORS, BY REGION, 2023–2030 (USD MILLION)

TABLE 40

HOME HEALTHCARE MARKET FOR OTHER THERAPEUTIC PRODUCTS, BY REGION, 2023–2030 (USD MILLION)

TABLE 41

KEY TESTING, SCREENING, AND MONITORING PRODUCTS OFFERED BY MAJOR COMPANIES

TABLE 42

HOME HEALTHCARE MARKET FOR TESTING, SCREENING, AND MONITORING PRODUCTS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 43

HOME HEALTHCARE MARKET FOR TESTING, SCREENING, AND MONITORING PRODUCTS MARKET, BY TYPE, 2023–2030 (MILLION UNITS)

TABLE 44

HOME HEALTHCARE MARKET FOR TESTING, SCREENING, AND MONITORING PRODUCTS MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 45

HOME HEALTHCARE MARKET FOR BLOOD GLUCOSE MONITORS, BY REGION, 2023–2030 (USD MILLION)

TABLE 46

HOME HEALTHCARE MARKET FOR HEARING AIDS, BY REGION, 2023–2030 (USD MILLION)

TABLE 47

HOME HEALTHCARE MARKET FOR ACTIVITY MONITORS & WRISTBANDS, BY REGION, 2023–2030 (USD MILLION)

TABLE 48

HOME HEALTHCARE MARKET FOR ECG/EKG DEVICES, BY REGION, 2023–2030 (USD MILLION)

TABLE 49

HOME HEALTHCARE MARKET FOR TEMPERATURE MONITORING DEVICES, BY REGION, 2023–2030 (USD MILLION)

TABLE 50

HOME HEALTHCARE MARKET FOR HEART RATE MONITORS, BY REGION, 2023–2030 (USD MILLION)

TABLE 51

KEY INNOVATIONS IN PULSE OXIMETERS BY MAJOR COMPANIES

TABLE 52

HOME HEALTHCARE MARKET FOR PULSE OXIMETERS, BY REGION, 2023–2030 (USD MILLION)

TABLE 53

HOME HEALTHCARE MARKET FOR OVULATION & PREGNANCY TEST KITS, BY REGION, 2023–2030 (USD MILLION)

TABLE 54

HOME HEALTHCARE MARKET FOR BLOOD PRESSURE MONITORS, BY REGION, 2023–2030 (USD MILLION)

TABLE 55

NUMBER OF PEOPLE LIVING WITH HIV VS. NEW HIV CASES, BY REGION, 2023

TABLE 56

HOME HEALTHCARE MARKET FOR HIV TEST KITS, BY REGION, 2023–2030 (USD MILLION)

TABLE 57

HOME HEALTHCARE MARKET FOR FETAL MONITORING DEVICES, BY REGION, 2023–2030 (USD MILLION)

TABLE 58

HOME HEALTHCARE MARKET FOR HOLTER & EVENT MONITORS, BY REGION, 2023–2030 (USD MILLION)

TABLE 59

HOME HEALTHCARE MARKET FOR DRUG & ALCOHOL TEST KITS, BY REGION, 2023–2030 (USD MILLION)

TABLE 60

HOME HEALTHCARE MARKET FOR COAGULATION MONITORING PRODUCTS, BY REGION, 2023–2030 (USD MILLION)

TABLE 61

HOME HEALTHCARE MARKET FOR PEAK FLOW METERS, BY REGION, 2023–2030 (USD MILLION)

TABLE 62

HOME HEALTHCARE MARKET FOR COLON CANCER TEST KITS, BY REGION, 2023–2030 (USD MILLION)

TABLE 63

HOME HEALTHCARE MARKET FOR EEG DEVICES, BY REGION, 2023–2030 (USD MILLION)

TABLE 64

HOME HEALTHCARE MARKET FOR HOME SLEEP TESTING DEVICES, BY REGION, 2023–2030 (USD MILLION)

TABLE 65

HOME HEALTHCARE MARKET FOR CHOLESTEROL TESTING PRODUCTS, BY REGION, 2023–2030 (USD MILLION)

TABLE 66

HOME HEALTHCARE MARKET FOR HOME HBA1C TEST KITS, BY REGION, 2023–2030 (USD MILLION)

TABLE 67

KEY MOBILITY CARE PRODUCTS OFFERED BY MAJOR PLAYERS

TABLE 68

HOME HEALTHCARE MARKET FOR MOBILITY CARE PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 69

HOME HEALTHCARE MARKET FOR MOBILITY CARE PRODUCTS, BY REGION, 2023–2030 (USD MILLION)

TABLE 70

HOME HEALTHCARE MARKET FOR WHEELCHAIRS, BY REGION, 2023–2030 (USD MILLION)

TABLE 71

HOME HEALTHCARE MARKET FOR MOBILITY SCOOTERS, BY REGION, 2023–2030 (USD MILLION)

TABLE 72

HOME HEALTHCARE MARKET FOR WALKERS & ROLLATORS, BY REGION, 2023–2030 (USD MILLION)

TABLE 73

HOME HEALTHCARE MARKET FOR CRUTCHES, BY REGION, 2023–2030 (USD MILLION)

TABLE 74

HOME HEALTHCARE MARKET FOR CANES, BY REGION, 2023–2030 (USD MILLION)

TABLE 75

HOME HEALTHCARE SERVICES MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 76

HOME HEALTHCARE SERVICES MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 77

HOME HEALTHCARE MARKET FOR SKILLED NURSING SERVICES, BY REGION, 2023–2030 (USD MILLION)

TABLE 78

HOME HEALTHCARE MARKET FOR REHABILITATION THERAPY SERVICES, BY REGION, 2023–2030 (USD MILLION)

TABLE 79

HOME HEALTHCARE MARKET FOR HOSPICE & PALLIATIVE CARE SERVICES, BY REGION, 2023–2030 (USD MILLION)

TABLE 80

HOME HEALTHCARE MARKET FOR UNSKILLED SERVICES, BY REGION, 2023–2030 (USD MILLION)

TABLE 81

HOME HEALTHCARE MARKET FOR RESPIRATORY THERAPY SERVICES, BY REGION, 2023–2030 (USD MILLION)

TABLE 82

HOME HEALTHCARE MARKET FOR INFUSION THERAPY SERVICES, BY REGION, 2023–2030 (USD MILLION)

TABLE 83

HOME HEALTHCARE MARKET FOR PREGNANCY CARE SERVICES, BY REGION, 2023–2030 (USD MILLION)

TABLE 84

HOME HEALTHCARE INDICATIONS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 85

HOME HEALTHCARE INDICATIONS MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 86

INCIDENCE OF CANCER, BY REGION, 2020 VS. 2030 VS. 2040 (MILLION)

TABLE 87

HOME HEALTHCARE MARKET FOR CANCER, BY REGION, 2023–2030 (USD MILLION)

TABLE 88

HOME HEALTHCARE MARKET FOR RESPIRATORY DISEASES, BY REGION, 2023–2030 (USD MILLION)

TABLE 89

HOME HEALTHCARE MARKET FOR MOBILITY DISORDERS, BY REGION, 2023–2030 (USD MILLION)

TABLE 90

HOME HEALTHCARE MARKET FOR PREGNANCY, BY REGION, 2023–2030 (USD MILLION)

TABLE 91

HOME HEALTHCARE MARKET FOR CARDIOVASCULAR DISEASES & HYPERTENSION, BY REGION, 2023–2030 (USD MILLION)

TABLE 92

HOME HEALTHCARE MARKET FOR WOUND CARE, BY REGION, 2023–2030 (USD MILLION)

TABLE 93

HOME HEALTHCARE MARKET FOR DIABETES, BY REGION, 2023–2030 (USD MILLION)

TABLE 94

HOME HEALTHCARE MARKET FOR HEARING DISORDERS, BY REGION, 2023–2030 (USD MILLION)

TABLE 95

HOME HEALTHCARE MARKET FOR OTHER INDICATIONS, BY REGION, 2023–2030 (USD MILLION)

TABLE 96

HOME HEALTHCARE MARKET, BY REGION, 2023–2030 (USD MILLION)

TABLE 97

NORTH AMERICA: KEY MACROECONOMIC INDICATORS

TABLE 98

NORTH AMERICA: HOME HEALTHCARE MARKET, BY COUNTRY, 2023–2030 (USD MILLION)

TABLE 99

NORTH AMERICA: HOME HEALTHCARE MARKET, BY PRODUCT & SERVICE, 2023–2030 (USD MILLION)

TABLE 100

NORTH AMERICA: HOME HEALTHCARE MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 101

NORTH AMERICA: HOME HEALTHCARE MARKET FOR THERAPEUTIC PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 102

NORTH AMERICA: HOME HEALTHCARE MARKET FOR TESTING, SCREENING, AND MONITORING PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 103

NORTH AMERICA: HOME HEALTHCARE MARKET FOR MOBILITY CARE PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 104

NORTH AMERICA: HOME HEALTHCARE SERVICES MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 105

NORTH AMERICA: HOME HEALTHCARE INDICATIONS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 106

US: HOME HEALTHCARE MARKET, BY PRODUCT & SERVICE, 2023–2030 (USD MILLION)

TABLE 107

US: HOME HEALTHCARE MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 108

US: HOME HEALTHCARE MARKET FOR THERAPEUTIC PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 109

US: HOME HEALTHCARE MARKET FOR TESTING, SCREENING, AND MONITORING PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 110

US: HOME HEALTHCARE MARKET FOR MOBILITY CARE PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 111

US: HOME HEALTHCARE SERVICES MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 112

US: HOME HEALTHCARE INDICATIONS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 113

CANADA: HOME HEALTHCARE MARKET, BY PRODUCT & SERVICE, 2023–2030 (USD MILLION)

TABLE 114

CANADA: HOME HEALTHCARE MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 115

CANADA: HOME HEALTHCARE MARKET FOR THERAPEUTIC PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 116

CANADA: HOME HEALTHCARE MARKET FOR TESTING, SCREENING, AND MONITORING PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 117

CANADA: HOME HEALTHCARE MARKET FOR MOBILITY CARE PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 118

CANADA: HOME HEALTHCARE SERVICES MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 119

CANADA: HOME HEALTHCARE INDICATIONS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 120

EUROPE: KEY MACROECONOMIC INDICATORS

TABLE 121

EUROPE: HOME HEALTHCARE MARKET, BY COUNTRY, 2023–2030 (USD MILLION)

TABLE 122

EUROPE: HOME HEALTHCARE MARKET, BY PRODUCT & SERVICE, 2023–2030 (USD MILLION)

TABLE 123

EUROPE: HOME HEALTHCARE MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 124

EUROPE: HOME HEALTHCARE MARKET FOR THERAPEUTIC PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 125

EUROPE: HOME HEALTHCARE MARKET FOR TESTING, SCREENING, AND MONITORING PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 126

EUROPE: HOME HEALTHCARE MARKET FOR MOBILITY CARE PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 127

EUROPE: HOME HEALTHCARE SERVICES MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 128

EUROPE: HOME HEALTHCARE INDICATIONS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 129

GERMANY: HOME HEALTHCARE MARKET, BY PRODUCT & SERVICE, 2023–2030 (USD MILLION)

TABLE 130

GERMANY: HOME HEALTHCARE MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 131

GERMANY: HOME HEALTHCARE MARKET FOR THERAPEUTIC PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 132

GERMANY: HOME HEALTHCARE MARKET FOR TESTING, SCREENING, AND MONITORING PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 133

GERMANY: HOME HEALTHCARE MARKET FOR MOBILITY CARE PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 134

GERMANY: HOME HEALTHCARE SERVICES MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 135

GERMANY: HOME HEALTHCARE INDICATIONS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 136

UK: HOME HEALTHCARE MARKET, BY PRODUCT & SERVICE, 2023–2030 (USD MILLION)

TABLE 137

UK: HOME HEALTHCARE MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 138

UK: HOME HEALTHCARE MARKET FOR THERAPEUTIC PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 139

UK: HOME HEALTHCARE MARKET FOR TESTING, SCREENING, AND MONITORING PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 140

UK: HOME HEALTHCARE MARKET FOR MOBILITY CARE PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 141

UK: HOME HEALTHCARE SERVICES MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 142

UK: HOME HEALTHCARE INDICATIONS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 143

FRANCE: HOME HEALTHCARE MARKET, BY PRODUCT & SERVICE, 2023–2030 (USD MILLION)

TABLE 144

FRANCE: HOME HEALTHCARE MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 145

FRANCE: HOME HEALTHCARE MARKET FOR THERAPEUTIC PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 146

FRANCE: HOME HEALTHCARE MARKET FOR TESTING, SCREENING, AND MONITORING PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 147

FRANCE: HOME HEALTHCARE MARKET FOR MOBILITY CARE PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 148

FRANCE: HOME HEALTHCARE SERVICES MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 149

FRANCE: HOME HEALTHCARE INDICATIONS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 150

ITALY: HOME HEALTHCARE MARKET, BY PRODUCT & SERVICE, 2023–2030 (USD MILLION)

TABLE 151

ITALY: HOME HEALTHCARE MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 152

ITALY: HOME HEALTHCARE MARKET FOR THERAPEUTIC PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 153

ITALY: HOME HEALTHCARE MARKET FOR TESTING, SCREENING, AND MONITORING PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 154

ITALY: HOME HEALTHCARE MARKET FOR MOBILITY CARE PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 155

ITALY: HOME HEALTHCARE SERVICES MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 156

ITALY: HOME HEALTHCARE INDICATIONS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 157

SPAIN: HOME HEALTHCARE MARKET, BY PRODUCT & SERVICE, 2023–2030 (USD MILLION)

TABLE 158

SPAIN: HOME HEALTHCARE MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 159

SPAIN: HOME HEALTHCARE MARKET FOR THERAPEUTIC PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 160

SPAIN: HOME HEALTHCARE MARKET FOR TESTING, SCREENING, AND MONITORING PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 161

SPAIN: HOME HEALTHCARE MARKET FOR MOBILITY CARE PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 162

SPAIN: HOME HEALTHCARE SERVICES MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 163

SPAIN: HOME HEALTHCARE INDICATIONS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 164

REST OF EUROPE: HOME HEALTHCARE MARKET, BY PRODUCT & SERVICE, 2023–2030 (USD MILLION)

TABLE 165

REST OF EUROPE: HOME HEALTHCARE MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 166

REST OF EUROPE: HOME HEALTHCARE MARKET FOR THERAPEUTIC PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 167

REST OF EUROPE: HOME HEALTHCARE MARKET FOR TESTING, SCREENING, AND MONITORING PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 168

REST OF EUROPE: HOME HEALTHCARE MARKET FOR MOBILITY CARE PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 169

REST OF EUROPE: HOME HEALTHCARE SERVICES MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 170

REST OF EUROPE: HOME HEALTHCARE INDICATIONS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 171

ASIA PACIFIC: KEY MACROECONOMIC INDICATORS

TABLE 172

ASIA PACIFIC: HOME HEALTHCARE MARKET, BY COUNTRY, 2023–2030 (USD MILLION)

TABLE 173

ASIA PACIFIC: HOME HEALTHCARE MARKET, BY PRODUCT & SERVICE, 2023–2030 (USD MILLION)

TABLE 174

ASIA PACIFIC: HOME HEALTHCARE MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 175

ASIA PACIFIC: HOME HEALTHCARE MARKET FOR THERAPEUTIC PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 176

ASIA PACIFIC: HOME HEALTHCARE MARKET FOR TESTING, SCREENING, AND MONITORING PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 177

ASIA PACIFIC: HOME HEALTHCARE MARKET FOR MOBILITY CARE PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 178

ASIA PACIFIC: HOME HEALTHCARE SERVICES MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 179

ASIA PACIFIC: HOME HEALTHCARE INDICATIONS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 180

JAPAN: HOME HEALTHCARE MARKET, BY PRODUCT & SERVICE, 2023–2030 (USD MILLION)

TABLE 181

JAPAN: HOME HEALTHCARE MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 182

JAPAN: HOME HEALTHCARE MARKET FOR THERAPEUTIC PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 183

JAPAN: HOME HEALTHCARE MARKET FOR TESTING, SCREENING, AND MONITORING PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 184

JAPAN: HOME HEALTHCARE MARKET FOR MOBILITY CARE PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 185

JAPAN: HOME HEALTHCARE SERVICES MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 186

JAPAN: HOME HEALTHCARE INDICATIONS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 187

CHINA: HOME HEALTHCARE MARKET, BY PRODUCT & SERVICE, 2023–2030 (USD MILLION)

TABLE 188

CHINA: HOME HEALTHCARE MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 189

CHINA: HOME HEALTHCARE MARKET FOR THERAPEUTIC PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 190

CHINA: HOME HEALTHCARE MARKET FOR TESTING, SCREENING, AND MONITORING PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 191

CHINA: HOME HEALTHCARE MARKET FOR MOBILITY CARE PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 192

CHINA: HOME HEALTHCARE SERVICES MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 193

CHINA: HOME HEALTHCARE INDICATIONS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 194

INDIA: HOME HEALTHCARE MARKET, BY PRODUCT & SERVICE, 2023–2030 (USD BILLION)

TABLE 195

INDIA: HOME HEALTHCARE MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 196

INDIA: HOME HEALTHCARE MARKET FOR THERAPEUTIC PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 197

INDIA: HOME HEALTHCARE MARKET FOR TESTING, SCREENING, AND MONITORING PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 198

INDIA: HOME HEALTHCARE MARKET FOR MOBILITY CARE PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 199

INDIA: HOME HEALTHCARE SERVICES MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 200

INDIA: HOME HEALTHCARE INDICATIONS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 201

REST OF ASIA PACIFIC: HOME HEALTHCARE MARKET, BY PRODUCT & SERVICE, 2023–2030 (USD BILLION)

TABLE 202

REST OF ASIA PACIFIC: HOME HEALTHCARE MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 203

REST OF ASIA PACIFIC: HOME HEALTHCARE MARKET FOR THERAPEUTIC PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 204

REST OF ASIA PACIFIC: HOME HEALTHCARE MARKET FOR TESTING, SCREENING, AND MONITORING PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 205

REST OF ASIA PACIFIC: HOME HEALTHCARE MARKET FOR MOBILITY CARE PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 206

REST OF ASIA PACIFIC: HOME HEALTHCARE SERVICES MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 207

REST OF ASIA PACIFIC: HOME HEALTHCARE INDICATIONS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 208

LATIN AMERICA: KEY MACROECONOMIC INDICATORS

TABLE 209

LATIN AMERICA: HOME HEALTHCARE MARKET, BY PRODUCT & SERVICE, 2023–2030 (USD BILLION)

TABLE 210

LATIN AMERICA: HOME HEALTHCARE MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 211

LATIN AMERICA: HOME HEALTHCARE MARKET FOR THERAPEUTIC PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 212

LATIN AMERICA: HOME HEALTHCARE MARKET FOR TESTING, SCREENING, AND MONITORING PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 213

LATIN AMERICA: HOME HEALTHCARE MARKET FOR MOBILITY CARE PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 214

LATIN AMERICA: HOME HEALTHCARE SERVICES MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 215

LATIN AMERICA: HOME HEALTHCARE INDICATIONS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 216

MIDDLE EAST & AFRICA: KEY MACROECONOMIC INDICATORS

TABLE 217

MIDDLE EAST & AFRICA: HOME HEALTHCARE MARKET, BY PRODUCT & SERVICE, 2023–2030 (USD BILLION)

TABLE 218

MIDDLE EAST & AFRICA: HOME HEALTHCARE MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 219

MIDDLE EAST & AFRICA: HOME HEALTHCARE MARKET FOR THERAPEUTIC PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 220

MIDDLE EAST & AFRICA: HOME HEALTHCARE MARKET FOR TESTING, SCREENING, AND MONITORING PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 221

MIDDLE EAST & AFRICA: HOME HEALTHCARE MARKET FOR MOBILITY CARE PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 222

MIDDLE EAST & AFRICA: HOME HEALTHCARE SERVICES MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 223

MIDDLE EAST & AFRICA: HOME HEALTHCARE INDICATIONS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 224

GCC COUNTRIES: KEY MACROECONOMIC INDICATORS

TABLE 225

GCC COUNTRIES: HOME HEALTHCARE MARKET, BY PRODUCT & SERVICE, 2023–2030 (USD BILLION)

TABLE 226

GCC COUNTRIES: HOME HEALTHCARE MARKET, BY PRODUCT, 2023–2030 (USD MILLION)

TABLE 227

GCC COUNTRIES: HOME HEALTHCARE MARKET FOR THERAPEUTIC PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 228

GCC COUNTRIES: HOME HEALTHCARE MARKET FOR TESTING, SCREENING, AND MONITORING PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 229

GCC COUNTRIES: HOME HEALTHCARE MARKET FOR MOBILITY CARE PRODUCTS, BY TYPE, 2023–2030 (USD MILLION)

TABLE 230

GCC COUNTRIES: HOME HEALTHCARE SERVICES MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 231

GCC COUNTRIES: HOME HEALTHCARE INDICATIONS MARKET, BY TYPE, 2023–2030 (USD MILLION)

TABLE 232

HOME HEALTHCARE MARKET: OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS, JANUARY 2022–JUNE 2025

TABLE 233

HOME HEALTHCARE MARKET: DEGREE OF COMPETITION, 2024 (%)

TABLE 234

HOME HEALTHCARE MARKET: REGION FOOTPRINT

TABLE 235

HOME HEALTHCARE MARKET: PRODUCT & SERVICE FOOTPRINT

TABLE 236

HOME HEALTHCARE MARKET: PRODUCT FOOTPRINT

TABLE 237

HOME HEALTHCARE MARKET: END-USER FOOTPRINT

TABLE 238

HOME HEALTHCARE MARKET: DETAILED LIST OF KEY STARTUPS/SMES

TABLE 239

HOME HEALTHCARE MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES, 2024

TABLE 240

HOME HEALTHCARE MARKET: PRODUCT LAUNCHES AND APPROVALS, JANUARY 2022–JUNE 2025

TABLE 241

HOME HEALTHCARE MARKET: DEALS, JANUARY 2022–JUNE 2025

TABLE 242

HOME HEALTHCARE MARKET: EXPANSIONS, JANUARY 2022–JUNE 2025

TABLE 243

FRESENIUS MEDICAL CARE AG: COMPANY OVERVIEW

TABLE 244

FRESENIUS MEDICAL CARE AG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 245

FRESENIUS MEDICAL CARE AG: PRODUCT LAUNCHES AND APPROVALS, JANUARY 2022–JUNE 2025

TABLE 246

FRESENIUS MEDICAL CARE AG: DEALS, JANUARY 2022–JUNE 2025

TABLE 247

FRESENIUS MEDICAL CARE AG: EXPANSIONS, JANUARY 2022–JUNE 2025

TABLE 248

ABBOTT: COMPANY OVERVIEW

TABLE 249

ABBOTT: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 250

ABBOTT: PRODUCT LAUNCHES AND APPROVALS, JANUARY 2022–JUNE 2025

TABLE 251

ABBOTT: DEALS, JANUARY 2022–JUNE 2025

TABLE 252

ABBOTT: EXPANSIONS, JANUARY 2022–JUNE 2025

TABLE 253

LINDE PLC: COMPANY OVERVIEW

TABLE 254

LINDE PLC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 255

F. HOFFMANN-LA ROCHE LTD: COMPANY OVERVIEW

TABLE 256

F. HOFFMAN-LA ROCHE LTD: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 257

F. HOFFMAN-LA ROCHE LTD: PRODUCT LAUNCHES AND APPROVALS, JANUARY 2022–JUNE 2025

TABLE 258

RESMED: COMPANY OVERVIEW

TABLE 259

RESMED: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 260

RESMED: PRODUCT LAUNCHES AND APPROVALS, JANUARY 2022–JUNE 2025

TABLE 261

RESMED: DEALS, JANUARY 2022–JUNE 2025

TABLE 262

KONINKLIJKE PHILIPS N.V.: COMPANY OVERVIEW

TABLE 263

KONINKLIJKE PHILIPS N.V.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 264

KONINKLIJKE PHILIPS N.V.: PRODUCT LAUNCHES AND APPROVALS, JANUARY 2022–JUNE 2025

TABLE 265

KONINKLIJKE PHILIPS N.V.: DEALS, JANUARY 2022–JUNE 2025

TABLE 266

GE HEALTHCARE: COMPANY OVERVIEW

TABLE 267

GE HEALTHCARE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 268

GE HEALTHCARE: DEALS, JANUARY 2022–JUNE 2025

TABLE 269

A&D HOLON HOLDINGS COMPANY, LIMITED: COMPANY OVERVIEW

TABLE 270

A&D HOLON HOLDINGS COMPANY, LIMITED: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 271

CONVATEC GROUP PLC: COMPANY OVERVIEW

TABLE 272

CONVATEC GROUP PLC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 273

CONVATEC GROUP PLC: PRODUCT LAUNCHES AND APPROVALS, JANUARY 2022–JUNE 2025

TABLE 274

CONVATEC GROUP PLC: DEALS, JANUARY 2022–JUNE 2025

TABLE 275

CONVATEC GROUP PLC: EXPANSIONS, JANUARY 2022–JUNE 2025

TABLE 276

AMEDISYS: COMPANY OVERVIEW

TABLE 277

AMEDISYS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 278

AMEDISYS: DEALS, JANUARY 2022–JUNE 2025

TABLE 279

OMRON HEALTHCARE CO., LTD.: COMPANY OVERVIEW

TABLE 280

OMRON HEALTHCARE CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 281

OMRON HEALTHCARE CO., LTD.: DEALS, JANUARY 2022–JUNE 2025

TABLE 282

INVACARE CORPORATION: COMPANY OVERVIEW

TABLE 283

BAYADA HOME HEALTH CARE: COMPANY OVERVIEW

TABLE 284

DRIVE DEVILBISS HEALTHCARE: COMPANY OVERVIEW

TABLE 285

SUNRISE MEDICAL: COMPANY OVERVIEW

TABLE 286

ROMA MEDICAL: COMPANY OVERVIEW

TABLE 287

CAREMAX REHABILITATION EQUIPMENT CO., LTD.: COMPANY OVERVIEW

TABLE 288

VITALOGRAPH: COMPANY OVERVIEW

TABLE 289

ADVITA PFLEGEDIENST GMBH: COMPANY OVERVIEW

TABLE 290

THE RENAFAN GROUP: COMPANY OVERVIEW

TABLE 291

CONTEC MEDICAL SYSTEMS CO., LTD.: COMPANY OVERVIEW

TABLE 292

B. BRAUN SE: COMPANY OVERVIEW

TABLE 293

BAXTER: COMPANY OVERVIEW

TABLE 294

MEDLINE INDUSTRIES: COMPANY OVERVIEW

TABLE 295

ADVIN HEALTH CARE: COMPANY OVERVIEW

LIST OF FIGURES

FIGURE 1

HOME HEALTHCARE MARKET SEGMENTATION AND REGIONAL SCOPE

FIGURE 2

HOME HEALTHCARE MARKET: RESEARCH DESIGN

FIGURE 3

BREAKDOWN OF PRIMARY INTERVIEWS: BY COMPANY TYPE, DESIGNATION, AND REGION

FIGURE 4

BOTTOM-UP APPROACH: COMPANY REVENUE ESTIMATION APPROACH

FIGURE 5

CAGR PROJECTIONS: SUPPLY-SIDE ANALYSIS

FIGURE 6

HOME HEALTHCARE MARKET: TOP-DOWN APPROACH

FIGURE 7

DATA TRIANGULATION METHODOLOGY

FIGURE 8

HOME HEALTHCARE MARKET: PARAMETRIC ASSUMPTIONS

FIGURE 9

HOME HEALTHCARE MARKET, BY PRODUCT & SERVICE, 2025 VS. 2030 (USD BILLION)

FIGURE 10

HOME HEALTHCARE MARKET, BY PRODUCT, 2025 VS. 2030 (USD BILLION)

FIGURE 11

HOME HEALTHCARE MARKET, BY SERVICE, 2025 VS. 2030 (USD BILLION)

FIGURE 12

HOME HEALTHCARE MARKET, BY INDICATION, 2025 VS. 2030 (USD BILLION)

FIGURE 13

HOME HEALTHCARE MARKET: GEOGRAPHICAL SNAPSHOT

FIGURE 14

GROWING ELDERLY POPULATION AND HIGH INCIDENCE OF CHRONIC DISEASES TO DRIVE MARKET

FIGURE 15

JAPAN TO REGISTER HIGHEST GROWTH DURING FORECAST PERIOD

FIGURE 16

ASIA PACIFIC TO LEAD MARKET DURING FORECAST PERIOD

FIGURE 17

DEVELOPED MARKETS TO HAVE LARGER SHARE DURING FORECAST PERIOD

FIGURE 18

HOME HEALTHCARE MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

FIGURE 19

HOME HEALTHCARE MARKET: TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

FIGURE 20

HOME HEALTHCARE MARKET: VALUE CHAIN ANALYSIS

FIGURE 21

HOME HEALTHCARE MARKET: SUPPLY CHAIN ANALYSIS

FIGURE 22

HOME HEALTHCARE MARKET: ECOSYSTEM ANALYSIS

FIGURE 23

HOME HEALTHCARE MARKET: INVESTMENT AND FUNDING SCENARIO, 2020–2024

FIGURE 24

HOME HEALTHCARE MARKET: PATENT ANALYSIS, JANUARY 2015–DECEMBER 2024

FIGURE 25

CANADA: APPROVAL PROCESS FOR MEDICAL DEVICES

FIGURE 26

EUROPE: CE APPROVAL PROCESS FOR MEDICAL DEVICES

FIGURE 27

HOME HEALTHCARE MARKET: PORTER’S FIVE FORCES ANALYSIS

FIGURE 28

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS OF HOME HEALTHCARE PRODUCTS

FIGURE 29

KEY BUYING CRITERIA FOR HOME HEALTHCARE PRODUCTS

FIGURE 30

AI USE CASES

FIGURE 31

ADJACENT MARKETS FOR HOME HEALTHCARE MARKET

FIGURE 32

NORTH AMERICA: HOME HEALTHCARE MARKET SNAPSHOT

FIGURE 33

ASIA PACIFIC: HOME HEALTHCARE MARKET SNAPSHOT

FIGURE 34

HOME HEALTHCARE MARKET: REVENUE SHARE ANALYSIS OF TOP FIVE PLAYERS, 2022–2024 (USD MILLION)

FIGURE 35

HOME HEALTHCARE MARKET SHARE ANALYSIS, 2024 (%)

FIGURE 36

EV/EBITDA OF KEY VENDORS, 2025

FIGURE 37

YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND 5-YEAR STOCK BETA OF KEY VENDORS

FIGURE 38

HOME HEALTHCARE MARKET: BRAND/PRODUCT COMPARISON

FIGURE 39

HOME HEALTHCARE MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

FIGURE 40

HOME HEALTHCARE MARKET: COMPANY FOOTPRINT

FIGURE 41

HOME HEALTHCARE MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

FIGURE 42

FRESENIUS MEDICAL CARE AG: COMPANY SNAPSHOT (2024)

FIGURE 43

ABBOTT: COMPANY SNAPSHOT (2024)

FIGURE 44

LINDE PLC: COMPANY SNAPSHOT (2024)

FIGURE 45

F. HOFFMANN-LA ROCHE LTD: COMPANY SNAPSHOT (2024)

FIGURE 46

RESMED: COMPANY SNAPSHOT (2024)

FIGURE 47

KONINKLIJKE PHILIPS N.V.: COMPANY SNAPSHOT (2024)

FIGURE 48

GE HEALTHCARE: COMPANY SNAPSHOT (2024)

FIGURE 49

A&D HOLON HOLDINGS COMPANY, LIMITED: COMPANY SNAPSHOT (2024)

FIGURE 50

CONVATEC GROUP PLC: COMPANY SNAPSHOT (2024)

FIGURE 51

AMEDISYS: COMPANY SNAPSHOT (2024)

FIGURE 52

OMRON HEALTHCARE CO., LTD.: COMPANY SNAPSHOT (2024)

Methodology

This study involved the extensive use of both primary and secondary sources. The research process involved the study of various factors affecting the industry to identify the segmentation types, industry trends, key players, competitive landscape, fundamental market dynamics, and key player strategies.

Secondary Research

The secondary research process involves the widespread use of secondary sources, directories, databases (such as Bloomberg Businessweek, Factiva, and D&B Hoovers), white papers, annual reports, investor presentations, SEC filings of companies and publications from government sources [such as National Institutes of Health (NIH), US FDA, US Census Bureau, World Health Organization (WHO), , Global Burden of Disease Study, and Centers for Medicare and Medicaid Services (CMS) were referred to identify and collect information for the global home healthcare market study. It was also used to obtain important information about the key players and market classification & segmentation according to industry trends to the bottom-most level, and key developments related to market and technology perspectives. A database of the key industry leaders was also prepared using secondary research.

Primary Research

In the primary research process, various sources from both the supply and demand sides were interviewed to obtain qualitative and quantitative information for this report. The primary sources from the supply side include industry experts such as CEOs, vice presidents, marketing and sales directors, technology & innovation directors, and related key executives from various key companies and organizations in the home healthcare market. The primary sources from the demand side include home healthcare service providers and home users. Primary research was conducted to validate the market segmentation, identify key players in the market, and gather insights on key industry trends & key market dynamics.

A breakdown of the primary respondents is provided below:

*C-level primaries include CEOs, CFOs, COOs, and VPs.

*Other designations include sales managers, marketing managers, business development managers, product managers, distributors, and suppliers.

Note: Companies are classified into tiers based on their total revenue. As of 2023, Tier 1 = >USD 10.00 billion, Tier 2 = USD 1.00 billion to USD 10.00 billion, and Tier 3 = < USD 1.00 billion.

Source: MarketsandMarkets Analysis

To know about the assumptions considered for the study, download the pdf brochure

Market Size Estimation

For the global market value, annual revenues were calculated based on the revenue mapping of major product manufacturers and OEMs active in the global home healthcare market. All the major service providers were identified at the global and/or country/regional level. Revenue mapping for the respective business segments/subsegments was done for the major players. Also, the global home healthcare market was split into various segments and sub-segments based on:

- List of major players operating in the product market at the regional and/or country level

- Product mapping of home healthcare providers at the regional and/or country level

- Mapping of annual revenue generated by listed major players from home healthcare (or the nearest reported business unit/product category)

- Extrapolation of the revenue mapping of the listed major players to derive the global market value of the respective segments/subsegments

- Summation of the market value of all segments/subsegments to arrive at the global home healthcare market

The above-mentioned data was consolidated and added with detailed inputs and analysis from MarketsandMarkets and presented in this report.

Market Size Estimation (Bottom-up Approach & Top-down Approach)

Data Triangulation

After arriving at the overall size of the global home healthcare market through the above-mentioned methodology, this market was split into several segments and subsegments. The data triangulation and market breakdown procedures were employed, wherever applicable, to complete the overall market engineering process and arrive at the exact market value data for the key segments and subsegments. The extrapolated market data was triangulated by studying various macro indicators and regional trends from both demand- and supply-side participants.

Market Definition

Home healthcare refers to the medical attention, care, and support provided to patients at their residences by licensed healthcare workers, such as nurses, home health aides, and personal care aides. The home healthcare market includes products and services that can be set up remotely at a patient’s home.

Stakeholders

- Home Healthcare Equipment Manufacturers

- Home Healthcare Service Providers

- Home Health Software Vendors

- Nursing Service Providers

- Wound Care Product Manufacturers

- Pregnancy Care Product Manufacturers and Service Providers

- Supportive Care Product Manufacturers and Service Providers

- Diagnostic Companies

- Research & Development (R&D) Companies

- Business Research and Consulting Service Providers

- Medical Research Laboratories

- Venture Capitalists

Report Objectives

- To define, describe, segment, and forecast the global home healthcare market by product, service, indication, and region

- To provide detailed information regarding the major factors influencing the market growth (such as drivers, restraints, opportunities, and challenges)

- To analyze the micromarkets with respect to individual growth trends, prospects, and contributions to the overall home healthcare market

- To analyze market opportunities for stakeholders and provide details of the competitive landscape for key players

- To forecast the size of the market segments with respect to five regions: North America, Europe, the Asia Pacific, Latin America, Middle East & Africa, and GCC Countries

- To profile the key players and comprehensively analyze their product portfolios, market positions, and core competencies

- To track and analyze company developments such as acquisitions, product launches & approvals, and expansions

- To benchmark players within the market using the proprietary “Competitive Leadership Mapping” framework, which analyzes market players on various parameters within the broad categories of business and product strategy

Key Questions Addressed by the Report

Which are the top industry players in the home healthcare market?

The key players in this market are Fresenius Medical Care AG (Germany), Abbott (US), Linde plc (Ireland), F. Hoffmann-La Roche, Ltd. (Switzerland), ResMed (US), Koninklijke Philips N.V. (Netherlands), GE Healthcare (US), A&D HOLON Holdings Company, Limited, Convatec Group PLC (UK), Amedisys (US), OMRON Healthcare Co., Ltd. (Japan).

What are some of the major drivers for this market?

Recent trends significantly shaping the home healthcare market include the rapid growth of the aging population, the increasing prevalence of chronic diseases, and the rising demand for affordable and accessible healthcare solutions. As the global elderly population expands, there is a greater need for continuous medical support to manage age-related health conditions such as heart disease, arthritis, diabetes, and respiratory disorders. At the same time, healthcare systems worldwide are under pressure to reduce costs without compromising the quality of care. Home healthcare has emerged as a practical solution, offering personalized medical services in the comfort of patients' homes, helping reduce hospital visits, lower treatment costs, and improve patient outcomes. These trends are collectively driving the demand for home-based medical care, technologies, and professional support services.

What are the major products used in home healthcare?

The home healthcare market is segmented into testing, screening, and monitoring products; therapeutic products; and mobility care products. The therapeutic products accounted for the largest share of the home healthcare market in 2024.

What are the major indications of the home healthcare market?

This report contains the following indication segments: cancer, respiratory diseases, mobility disorders, cardiovascular diseases and hypertension, pregnancy, wound care, diabetes, hearing disorders, and other indications.

Which region is lucrative for the global home healthcare market?

The Asia Pacific region is anticipated to experience the fastest growth in the home healthcare market during the forecast period. The growing demand for high-quality, patient-centered healthcare services is encouraging the adoption of home-based care solutions. In addition, increasing healthcare expenditures, favorable government policies, and greater public awareness about the benefits of home monitoring and early intervention are further accelerating market expansion. These factors are collectively boosting the demand for a wide range of home healthcare products and services across the region.

Fact checked

Personalize This Research

- Triangulate with your Own Data

- Get Data as per your Format and Definition

- Gain a Deeper Dive on a Specific Application, Geography, Customer or Competitor

- Any level of Personalization

Let Us Help You

- What are the Known and Unknown Adjacencies Impacting the Home Healthcare Market

- What will your New Revenue Sources be?

- Who will be your Top Customer; what will make them switch?

- Defend your Market Share or Win Competitors

- Get a Scorecard for Target Partners

Custom Market Research Services

We Will Customise The Research For You, In Case The Report Listed Above Does Not Meet With Your Requirements

Get 10% Free CustomisationTESTIMONIALS

JAYANT RAJPUROHIT

Director of Market Insights, Data and Analytics

SFI Health,

Leading Pharmaceutical Companywww.sfihealth.com/

We at SFI Health approached MarketsandMarkets for an Opportunity Assessment on "Incidence and Prevalence of Focus Indications" as we wanted to know the most attractive HCPs like Physician, Functional MD, Naturopath and Pharmacist. The project was critical for us to ensure our focus on the right target which would enable sustainable growth and profitability for SFI Health. The business insights provided exceeded our expectations and we were extremely impressed. The team at MarketsandMarkets is highly professional and detail oriented and very well understood our business needs. MarketsandMarkets offers a unique combination of expertise and dedicated engagement model. We identified 2 new products to be launched in coming months, based on the research findings provided by MarketsandMarkets. We are happy with the services and would strongly recommend MarketsandMarkets to my peers in the industry.

BEATRIZ DE LA CALLE

Head of Commercial Analytics

Qualicaps,

Leading Pharmaceutical Companywww.qualicaps.com/

We partnered with MarketsandMarkets for an assessment study on hard empty capsules. The team was extremely professional in understanding our business requirements and we received timely responses to all our queries. The market intelligence and the recommendations has met our business requirements. We were extremely impressed to see the final study results; it really exceeded our expectations. The market intelligence offered by MarketsandMarkets, and clarity on next steps will help us achieve our business objective for the Year 2021. We are happy with the services and would strongly recommend MarketsandMarkets to my peers in the industry.

Bob Williams,

Senior Director Business Development & Innovation

Bracco Diagnostics Inc.,

Italian Multinational in life sciences sector and a World Leader in imaging diagnosticsimaging.bracco.com/us-en

We were pleased with targeted insights that MarketsandMarkets identified from a custom study on the 'Radiation Dose Management Solutions Market'. Your team identified and characterized the market participants as well as underlying trends accurately. This study was useful to Bracco in formulating business strategies for our dose monitoring product lines and we thank MarketsandMarkets for the job well done.

Cody Coonradt,

Market Development and Strategy Manager

3M Health Information Systems,

Leader in Health care Coding, Payment & Analytics Solutions.www.3m.com/3M/en_US/health-information-systems-us

The value for our organization comes from three things: depth of research, specificity of segments and being easy to work with. As important as the first two are, the third can't be underestimated. MarketsandMarkets, maybe more than any other research vendor, wants to know what is top of mind for our team and what big questions we are grappling to answer.

Their customer first approach and high value engagement model, have given us great analysis and excellent value for money

- US Home Healthcare Market

- Canada Home Healthcare Market

- UK Home Healthcare Market

- Germany Home Healthcare Market

- France Home Healthcare Market

- Italy Home Healthcare Market

- Spain Home Healthcare Market

- China Home Healthcare Market

- Japan Home Healthcare Market

- India Home Healthcare Market

- GCC Countries Home Healthcare Market

Growth opportunities and latent adjacency in Home Healthcare Market

Olivia

Jun, 2026

After reviewing the Home Healthcare Market insights, I see a strong business case for providers to expand decentralized care models as aging populations and cost pressures continue to shift demand away from traditional hospital settings..

Ethan

Jun, 2026

From a strategic standpoint, the Home Healthcare Market highlights how technology integration, especially remote monitoring and digital health platforms, is becoming essential for improving patient outcomes while maintaining operational efficiency..

Sophia

Jun, 2026

Looking at the broader landscape, my takeaway from the Home Healthcare Market is that reimbursement frameworks and regional policy variations will play a decisive role in how quickly service providers can scale sustainably..

Matthew

Mar, 2022

Which is the fastest growing market of Home Healthcare Market?.

Mark

Mar, 2022

Can you enlighten us with your market intelligence to grow and sustain in Home Healthcare Market?.

Donald

Mar, 2022

What are the growth estimates for Home Healthcare Market till 2026?.