Download PDF

Download PDF Request Customisation

Request Customisation

Machine Vision Market Size, Share & Trends

Report Code

SE 5835

Published in

May, 2025, By MarketsandMarkets™

Machine Vision Market Size, Share & Trends by Component (Camera, Frame Grabbers, Optics, LED Lighting, Processors, AI-based Machine Vision Software), Type (PC based, Smart Camera-based), Deployment (General, Robotic Cell), Vision Type (1D, 2D, 3D) - Global Forecast to 2030

USD 23.63

MARKET SIZE, 2030

CAGR 8.3%

(2025-2030)

310

REPORT PAGES

232

MARKET TABLES

MACHINE VISION MARKET SIZE, SHARE & TRENDS

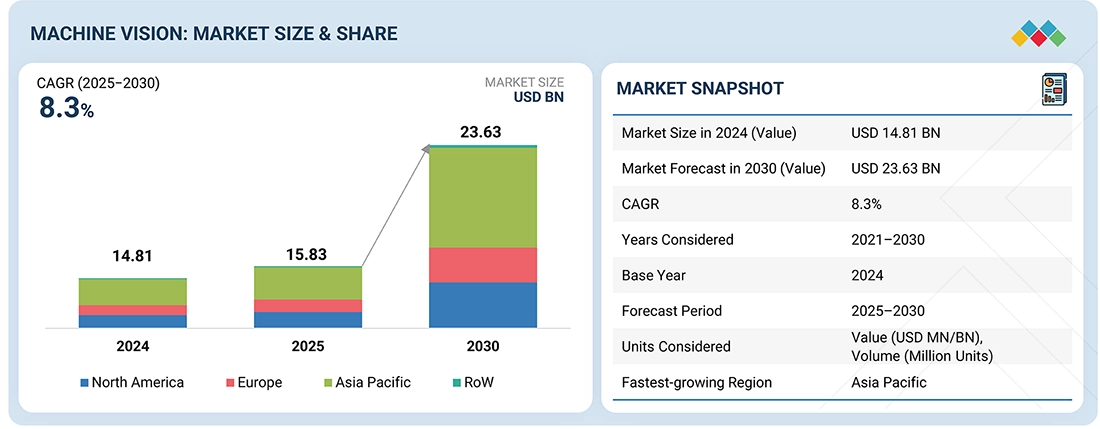

The global machine vision market size was valued at USD 15.83 billion in 2025 and is projected to reach USD 23.63 billion by 2030, growing at a CAGR of 8.3% from 2025 to 2030. Advancements in automation and Industry 4.0, particularly in markets such as automotive, electronics, and pharmaceuticals, are driving the demand for machine vision systems industry to enhance quality control and operational optimization. The integration of AI and deep learning technologies significantly enhances the ability of these systems in terms of defect detection and predictive maintenance, particularly in high-growth industries such as electronics & semiconductors.

MARKET SNAPSHOT TABLE

| REPORT METRIC | DETAILS |

|---|---|

| Market Size in 2025 (Value) | USD 15.83 Billion |

| Market Forecast in 2030 (Value) | USD 23.63 Billion |

| Growth Rate | CAGR of 8.3% from 2025-2030 |

| Years Considered | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million/Billion), Volume (Million Unit) |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Top Companies |

|

| Growth Drivers |

|

| Segments Covered |

|

| Regional Scope | North America, Europe, Asia Pacific, Latin America, Middle East, and RoW |

Market Size & Forecast

• 2025 Market Size: USD 15.83 Billion

• 2030 Projected Market Size: USD 23.63 Billion

• CAGR (2025-2030): 8.3%

• AI-based machine vision software: Fastest-growing component

• Asia Pacific : Fastest growing market

MACHINE VISION MARKET KEY TAKEAWAYS

-

BY COMPONENTThe machine vision market share is segmented into cameras, optics, frame grabbers, processors, LED lighting, other hardware components, and software. The software segment, particularly AI-based machine vision software, is the fastest-growing component because it represents the intelligence layer that unlocks the true potential of the system. Advances in deep learning enable software to handle complex, unstructured inspection tasks with greater accuracy and flexibility than traditional rule-based systems, thereby increasing the value derived from fixed hardware components.

-

BY SYSTEM TYPEThe market is bifurcated into PC-based and Smart Camera-based. PC-based systems have historically held the largest market share due to their superior processing power and memory, which are necessary for complex, high-resolution 3D and multi-camera inspection tasks. These systems offer greater flexibility for customized applications and software integration, making them the preferred choice for demanding manufacturing environments in sectors like automotive and electronics.

-

BY INDUSTRYThe market serves a wide range of industries, including automotive, consumer products, electronics & semiconductors, printing, logistics, metals, rubber & plastics, food & beverages, healthcare, machinery, solar panel manufacturing, and other robotic vision industries. The food & beverage sector holds the largest market share, primarily due to stringent quality and safety regulations that mandate comprehensive inspection systems for sorting, grading, and detecting foreign objects. The consistency provided by machine vision is essential in high-speed processing lines to prevent contamination and maintain brand reputation, driving high adoption across packaging and quality control applications.

-

BY REGIONThe Asia Pacific is projected to record the fastest growth, with a CAGR of 9.2%, due to massive ongoing industrial automation efforts across major economies, including China, India, and South Korea. This growth is fueled by large-scale expansion in high-tech manufacturing, especially in electronics and automotive production, which requires high-volume, precision inspection and quality control offered by machine vision systems.

-

COMPETITIVE LANDSCAPEThe leading players in the market are Cognex Corporation, Teledyne Technologies Inc., KEYENCE CORPORATION, Omron Corporation, and Basler AG. Companies are pursuing strategic acquisitions and partnerships to expand their product portfolios and provide machine vision solutions, thereby strengthening their market position.

The machine vision market growth is growing rapidly as manufacturers increasingly demand higher precision, quality, and speed, particularly in sectors such as electronics, automotive, and pharmaceuticals. Technological advancements, including improved sensors, AI/ML, embedded processing, and smart cameras, are making vision systems more reliable and cost-effective. Additionally, labor shortages, rising automation in logistics and e-commerce, and stricter quality/regulatory standards are accelerating adoption.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

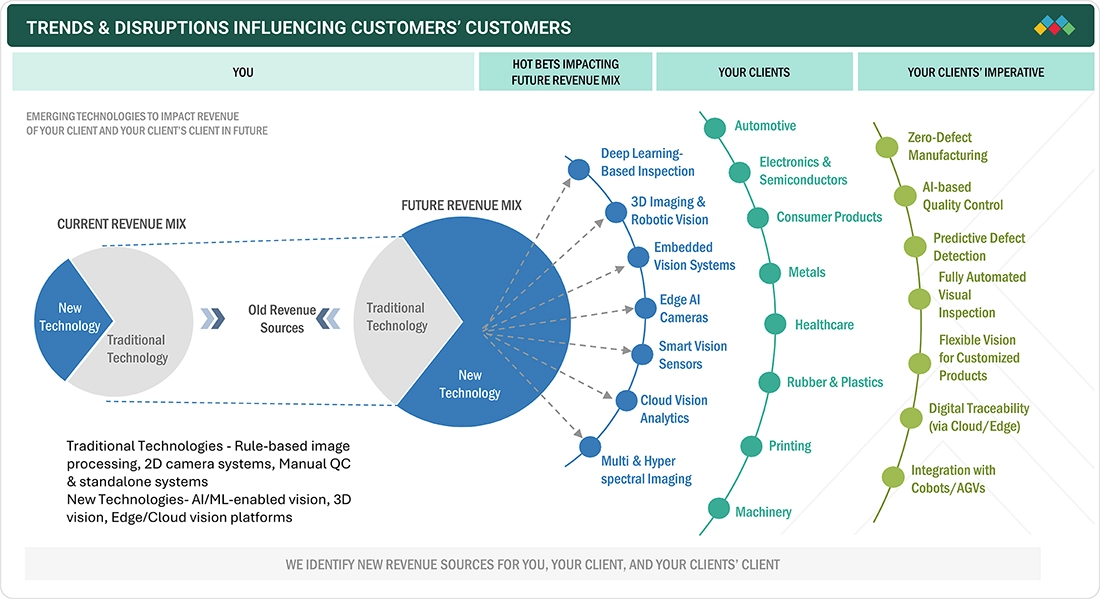

TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' CUSTOMERS

The demand for machine vision systems is expected to increase over the next few years due to the growing need for automation in inspection processes across various industries. Key trends in the machine vision market trends include AI-driven advancements, integration with Industry 4.0 and smart manufacturing, rapid technological innovations, the emergence of embedded vision systems, edge computing, collaborative robots with vision capabilities, customization, a focus on sustainability, and data security. These trends impact customer businesses by enhancing efficiency, enabling real-time decision-making, supporting sustainability goals, and ensuring secure data handling in machine vision applications.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

MACHINE VISION MARKET DYNAMICS

Drivers

Impact

Level

Level

-

Increasing demand for quality assurance and automated inspection in manufacturing industry

-

Rising adoption of vision-guided robotic systems across multiple industries

RESTRAINTS

Impact

Level

Level

-

Lack of awareness and high cost associated with machine vision systems

OPPORTUNITIES

Impact

Level

Level

-

Rising adoption in food & beverage industry

-

Government-backed initiatives to support industrial automation

CHALLENGES

Impact

Level

Level

-

Complexities in integrating diverse machine vision components with traditional systems

-

Cyber vulnerabilities in industrial robotic systems

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Driver: Increasing demand for quality assurance and automated inspection in manufacturing industry

Manufacturing companies worldwide are increasingly investing in automation. Also, the need for automated quality assurance has increased as industries have realized its importance in manufacturing processes. Quality assurance helps minimize defects, improve production efficiency, and ensure consistent product quality in manufacturing processes. This has led to the widespread adoption of machine vision as an integral part of long-term automation development processes.

Restraint: Lack of awareness and high cost associated with machine vision systems

A key challenge to the wider adoption of machine vision, despite its role in automation, is the lack of user awareness regarding advanced systems. While 3D stereo vision provides vital capabilities—such as precise distance measurement and complex defect identification (e.g., bent pins or irregular bottle shapes)—its sophistication creates barriers. The increasing complexity of 3D technology demands frequent training and workshops, which are costly and time-intensive. Consequently, operators often struggle to utilize these systems effectively, resulting in poor programming, inaccurate results, and unnecessary expenses.

Opportunity: Rising adoption in food & beverage industry

There has been a surge in demand for packaged food products, including biscuits, processed foods, frozen desserts, meat, and noodles. There is increasing adoption of machine vision technologies due to the growing demand for packaged food products. The major applications of AI machine vision systems in the food & beverage industry fall into three broad categories: production and processing, packaging and distribution, and tracking and tracing products through complex supply chains.

Challenge: Complexities in integrating diverse machine vision components with traditional systems

Whether it is a camera, optics, software, lighting, or a frame grabber, versatile solutions can be quickly developed to tackle a wide range of tasks by using multipurpose components. However, there is an urgent need to simplify the integration process of various components in machine vision systems and production lines at application sites. With the increasing need for convenient installation and handling of all technical systems, players in the machine vision industry must develop plug-and-play solutions to meet the demand for easier integration and installation.

Machine Vision Market: COMMERCIAL USE CASES ACROSS INDUSTRIES

| COMPANY | USE CASE DESCRIPTION | BENEFITS |

|---|---|---|

|

Advanced cameras (2D, 3D, SWIR, line scan, embedded) and AI-enabled vision software for industrial inspection, robotics, logistics, pharma, automotive, and smart infrastructure | High image accuracy, rapid defect detection, modular systems, reliable AI analysis, broad application coverage, easy integration |

|

Smart cameras/vision sensors for automated assembly, high-speed quality inspection, and robot guidance, widespread in automotive, electronics, and food industries | Consistent accuracy, quick deployment, flexible setups, robust programming, reduced manual oversight, scalable to diverse industries |

|

Embedded and AI-powered vision platforms for real-time analytics, defect detection, lab automation, packaging, and automotive components | Reliable imaging for demanding environments, multi-format analytics, easy integration, robust data capture, customizable workflows |

|

Vision systems (2D/3D/AI) for bin picking, object recognition, production quality control, dynamic factory inspection and automation | Flexible calibration, wide industry support, rapid error-proofing, fast deployment, versatile inspection modes, enhanced productivity |

|

Vision-guided and deep learning systems for defect detection, traceability, barcode reading, robotic guidance, and yield optimization in manufacturing and logistics | Superior speed, robust accuracy, automated learning, minimal manual configuration, seamless traceability, high operational ROI |

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

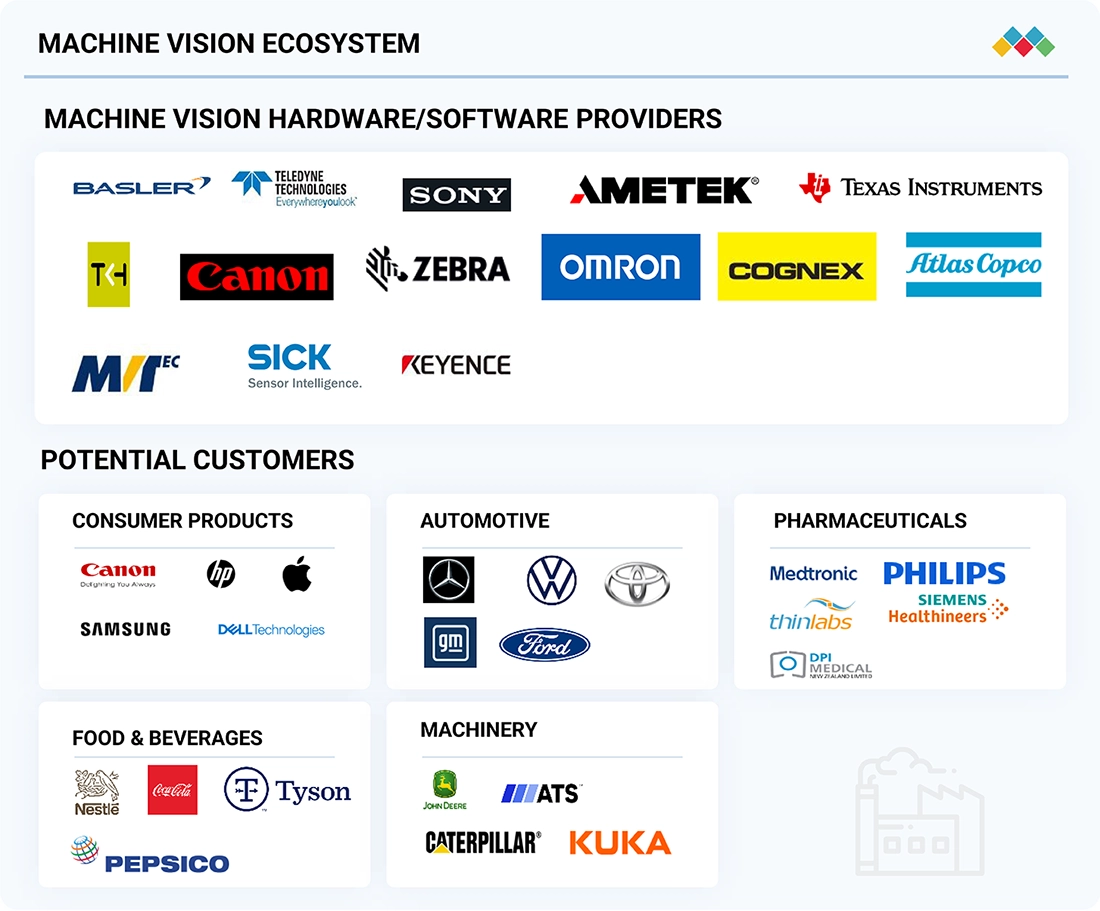

MACHINE VISION MARKET ECOSYSTEM

A robust ecosystem of established hardware and software providers supports the machine vision market, which includes key players like Cognex Corporation (US), Basler AG (Germany), KEYENCE CORPORATION (Japan), Teledyne Technologies Inc. (US), and Omron Corporation (Japan). These companies offer advanced imaging technologies tailored to the needs of diverse industries. The market serves a wide range of potential customers across various sectors, including consumer products, automotive, pharmaceuticals, food & beverages, and machinery, highlighting its cross-sectoral relevance. The strong presence of industrial giants reflects the growing demand for automation, quality control, and intelligent inspection solutions.

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

MACHINE VISION MARKET SEGMENTS

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Machine Vision Market, By Component

The cameras segment held the largest market share in 2024, primarily because they are the fundamental, indispensable hardware component at the very start of any machine vision process. The camera is responsible for the crucial initial step of image capture, and its cost forms a substantial portion of the system's total bill of materials. Furthermore, the increasing demand for specialized, high-resolution smart cameras drives up the overall value of this segment.

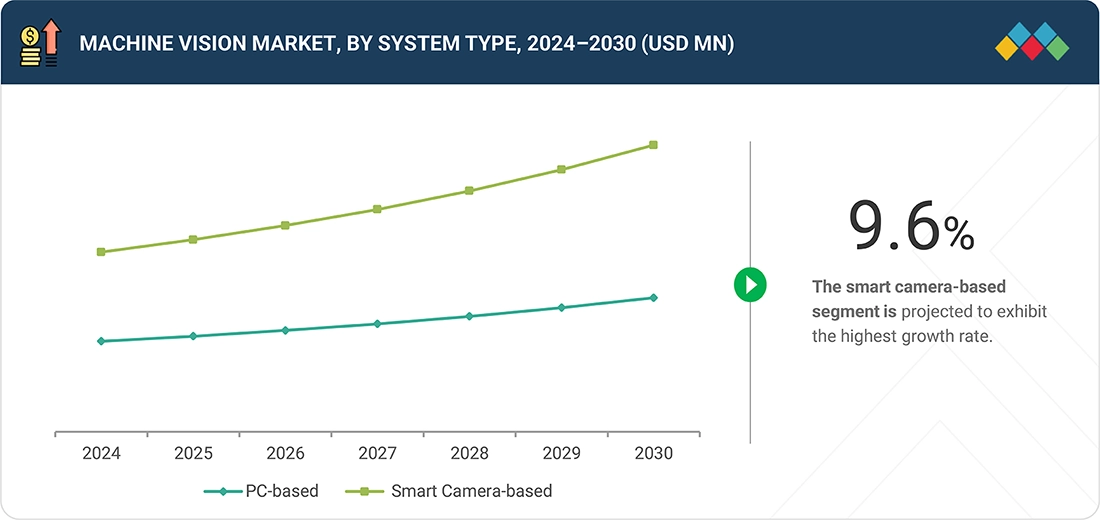

Machine Vision Market, By System Type

The smart camera-based segment is experiencing the fastest growth because these systems integrate the camera, processor, and software into a single, compact unit. This results in easier installation, reduced integration complexity, and lower overall system costs for simpler inspection tasks, making them highly attractive for small- to medium-scale automation.

Machine Vision Market, By Industry

The Food & Beverage segment is forecast to be the fastest-growing in the machine vision market, primarily due to the increasing focus on strict quality control and traceability across the industry supply chain. Machine vision systems are being rapidly adopted for critical tasks such as high-speed packaging inspection, ensuring product integrity, and complying with complex regulatory standards.

MACHINE VISION MARKET REGION

Asia Pacific is expected to register the highest CAGR in the global machine vision market during the forecast period.

The Asia Pacific is projected to be the fastest-growing market for the machine vision market. The growth can be attributed to the large presence of major players through their subsidiaries, distributors, and resellers. China has a strong export industry. It is a major manufacturing hub for various industries, including electronics, semiconductors, automotive, and other consumer goods. The country has experienced tremendous industrial growth over the past two decades and has surpassed the US to become the world's largest producer of manufactured goods.

The North America machine vision market is projected to reach USD 6.66 billion by 2030 from USD 4.13 billion in 2024, growing at a CAGR of 8.5% from 2025 to 2030. Market growth is driven by the increasing adoption of automation in manufacturing, rising demand for quality inspection, rapid advancements in AI-based vision, and strong investments in smart factories and industrial digitization initiatives across the region.

The machine vision market in Europe is projected to reach USD 5.43 billion by 2030, up from USD 3.61 billion in 2024, with a CAGR of 7.3% from 2025 to 2030. Market growth is driven by the rising adoption of automation across European manufacturing, increasing demand for high-precision inspection, rapid advancements in AI-enabled vision technologies, and strong momentum toward smart factories supported by EU digitalization initiatives.

The Asia Pacific machine vision market is projected to reach USD 9.81 billion by 2030, up from USD 5.85 billion in 2024, growing at a CAGR of 9.2% from 2025 to 2030. Growth is supported by the region’s expanding electronics and semiconductor manufacturing base, accelerating automation in automotive and EV production, rising adoption of AI-driven inspection systems, and increasing investments in smart factory and industrial digitalization initiatives across the Asia Pacific.

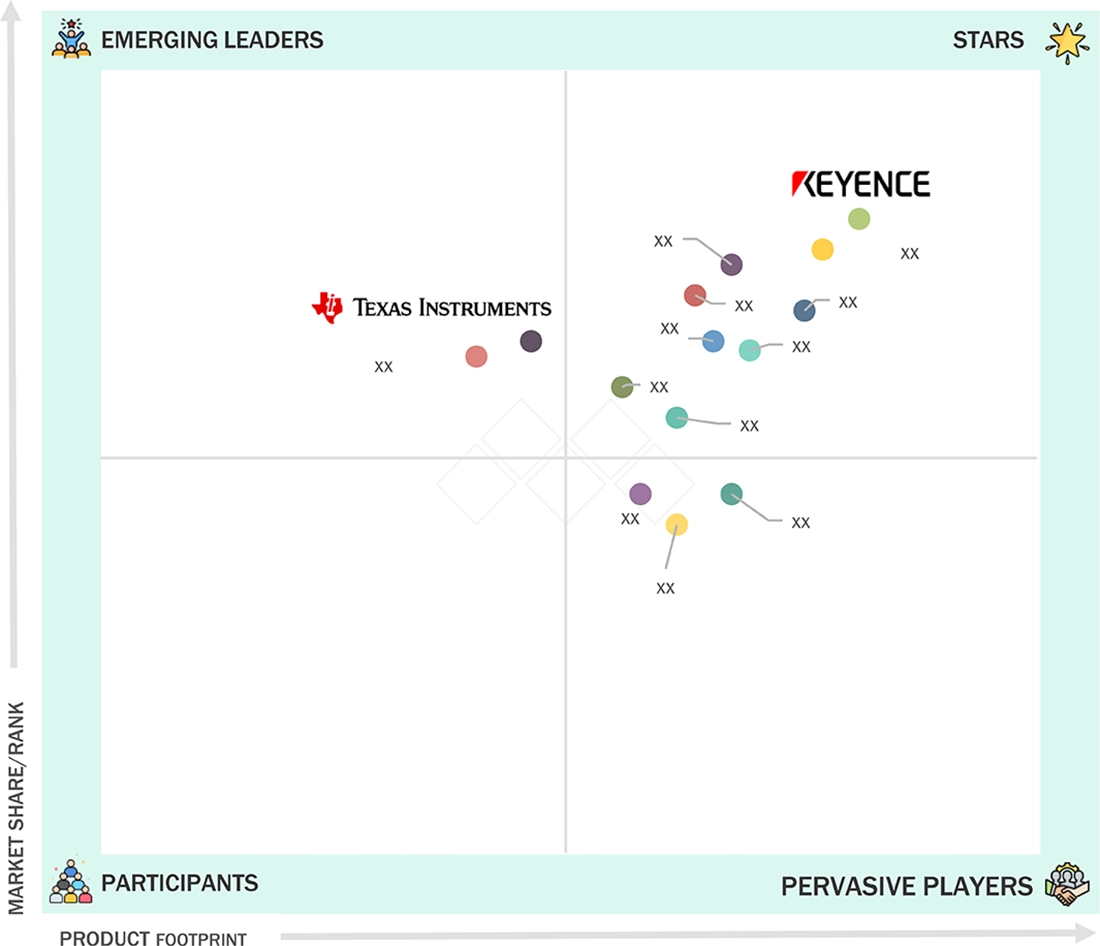

Machine Vision Market: COMPANY EVALUATION MATRIX

In the machine vision market matrix, KEYENCE CORPORATION (Star) and Texas Instruments Incorporated (Emerging Leader) hold strong positions with their broad product portfolios, global presence, and robust financial capabilities. Their continuous innovation and brand equity enable them to lead large-scale adoption of machine vision solutions worldwide.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

MACHINE VISION MARKET KEY PLAYERS

WHAT IS IN IT FOR YOU: Machine Vision Market REPORT CONTENT GUIDE

DELIVERED CUSTOMIZATIONS

We have successfully delivered the following deep-dive customizations:

| CLIENT REQUEST | CUSTOMIZATION DELIVERED | VALUE ADDS |

|---|---|---|

| European Automotive OEM |

|

|

| North American Electronics Manufacturer |

|

|

| Asia Pacific Pharmaceutical Packaging Company |

|

|

RECENT DEVELOPMENTS

- March 2025 : Keyence Corporation (Japan) launched vision sensor with built-in AI automates part detection, position verification, and counting under challenging conditions, surpassing traditional vision sensors. It ensures stability against environmental factors and simplify complex applications.

- September 2024 : Teledyne DALSA (Canada), a subsidiary of Teledyne Technologies Inc. (US), introduced the Linea HS2 TDI line scan camera family. It offers ultra-high-speed imaging with 16k resolution and 1 MHz line rates, excelling in light-starved environments. This next-generation TDI technology achieves 16 Gigapixels per second data throughput, representing a significant advancement in line scan imaging.

- August 2024 : Cognex Corporation (US) enhanced its In-Sight SnAPP vision sensor with a new AI-powered counting tool. This tool helps in automating assembly verification and quantity checks for manufacturers. It simplifies counting complex parts, including reflective, distorted, and varying contrast objects.

Table of Contents

![]() Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

TITLE

PAGE NO

1

INTRODUCTION

27

2

RESEARCH METHODOLOGY

32

3

EXECUTIVE SUMMARY

44

4

PREMIUM INSIGHTS

49

5

MARKET OVERVIEW

Surging demand for AI-powered vision systems reshapes manufacturing with enhanced quality and safety.

53

5.1

INTRODUCTION

5.2

MARKET DYNAMICS

5.2.1

DRIVERS

5.2.1.1

INCREASING DEMAND FOR QUALITY ASSURANCE AND AUTOMATED INSPECTION IN MANUFACTURING INDUSTRY

5.2.1.2

RISING ADOPTION OF VISION-GUIDED ROBOTIC SYSTEMS ACROSS MULTIPLE INDUSTRIES

5.2.1.3

GROWING EMPHASIS ON SAFETY AND IMPROVED PRODUCT QUALITY

5.2.1.4

GROWING ADOPTION OF AI-POWERED SYSTEMS ACROSS INDUSTRIES

5.2.2

RESTRAINTS

5.2.2.1

LACK OF AWARENESS AND HIGH COST ASSOCIATED WITH MACHINE VISION SYSTEMS

5.2.3

OPPORTUNITIES

5.2.3.1

RISING ADOPTION IN FOOD & BEVERAGE INDUSTRY

5.2.3.2

GOVERNMENT-BACKED INITIATIVES TO SUPPORT INDUSTRIAL AUTOMATION

5.2.3.3

EMERGENCE OF COMPACT SMART CAMERAS AND PROCESSORS

5.2.3.4

SURGING DEMAND FOR HYBRID AND EVS

5.2.4

CHALLENGES

5.2.4.1

COMPLEXITIES IN INTEGRATING DIVERSE MACHINE VISION COMPONENTS WITH TRADITIONAL SYSTEMS

5.2.4.2

CYBER VULNERABILITIES IN INDUSTRIAL ROBOTIC SYSTEMS

5.2.4.3

LACK OF SKILLED WORKFORCE TO OPERATE MACHINE VISION SYSTEMS

5.3

TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4

PRICING ANALYSIS

5.4.1

INDICATIVE PRICING OF MACHINE VISION KEY COMPONENT (CAMERA), BY KEY PLAYERS, 2024

5.4.2

AVERAGE SELLING PRICE TREND OF MACHINE VISION HARDWARE COMPONENT, 2021–2024

5.4.3

AVERAGE SELLING PRICE TREND OF MACHINE VISION HARDWARE COMPONENT, BY REGION, 2021–2024

5.5

VALUE CHAIN ANALYSIS

5.6

ECOSYSTEM ANALYSIS

5.7

INVESTMENT AND FUNDING SCENARIO

5.8

TECHNOLOGY ANALYSIS

5.8.1

KEY TECHNOLOGIES

5.8.1.1

ROBOTIC VISION

5.8.1.2

AI IN MACHINE VISION

5.8.2

COMPLEMENTARY TECHNOLOGIES

5.8.2.1

5G

5.8.2.2

EDGE COMPUTING

5.8.3

ADJACENT TECHNOLOGIES

5.8.3.1

CLOUD COMPUTING

5.9

PATENT ANALYSIS

5.10

TRADE ANALYSIS

5.10.1

IMPORT SCENARIO (HS CODE 852580)

5.10.2

EXPORT SCENARIO (HS CODE 852580)

5.11

KEY CONFERENCES AND EVENTS, 2025–2026

5.12

CASE STUDY

5.12.1

PANPASS TECHNOLOGY CO., LTD. AND COGNEX CORPORATION TRANSFORM YUNMEN WINE GROUP'S TRACEABILITY THROUGH MACHINE VISION AND AI-BASED OCR

5.12.2

PRESCRIPTIVE DATA USES TELEDYNE FLIR'S MACHINE VISION SENSORS TO DELIVER ACCURATE OCCUPANCY DATA FOR SMART BUILDINGS

5.12.3

LEADING AUTOMOTIVE SUPPLIER IMPROVES INSPECTION EFFICIENCY WITH FUJIFILM'S 4D HIGH RESOLUTION MACHINE VISION LENSES

5.12.4

ADVANCED DIMENSIONAL AND QUALITY CONTROL WITH 3D MACHINE VISION AT SIDENOR STEEL MILL

5.13

REGULATORY LANDSCAPE

5.13.1

REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.13.2

STANDARDS

5.14

PORTER'S FIVE FORCES ANALYSIS

5.14.1

THREAT OF NEW ENTRANTS

5.14.2

THREAT OF SUBSTITUTES

5.14.3

BARGAINING POWER OF SUPPLIERS

5.14.4

BARGAINING POWER OF BUYERS

5.14.5

INTENSITY OF COMPETITIVE RIVALRY

5.15

KEY STAKEHOLDERS AND BUYING CRITERIA

5.15.1

KEY STAKEHOLDERS IN BUYING PROCESS

5.15.2

BUYING CRITERIA

5.16

IMPACT OF AI/GEN AI ON MACHINE VISION MARKET

5.16.1

INTRODUCTION

5.16.2

IMPACT OF AI/GEN AI ON KEY END-USE INDUSTRIES

5.16.2.1

ELECTRONICS & SEMICONDUCTORS

5.16.2.2

FOOD & BEVERAGES

5.16.3

AI USE CASES

5.16.4

FUTURE OF AI/GEN AI IN MACHINE VISION ECOSYSTEM

5.17

IMPACT OF 2025 US TARIFF ON MACHINE VISION MARKET

5.17.1

INTRODUCTION

5.17.2

KEY TARIFF RATES

5.17.3

PRICE IMPACT ANALYSIS

5.17.4

IMPACT ON COUNTRIES/REGIONS

5.17.4.1

US

5.17.4.2

EUROPE

5.17.4.3

ASIA PACIFIC

5.17.5

IMPACT ON END-USE INDUSTRIES

6

APPLICATIONS OF MACHINE VISION

Revolutionize efficiency and precision with machine vision's diverse, industry-transforming applications.

97

6.1

INTRODUCTION

6.2

QUALITY ASSURANCE AND INSPECTION

6.3

POSITIONING AND GUIDANCE

6.4

MEASUREMENT

6.5

IDENTIFICATION

6.6

PREDICTIVE MAINTENANCE

7

MACHINE VISION MARKET, BY COMPONENT

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million and Units | 24 Data Tables

101

7.1

INTRODUCTION

7.2

CAMERAS

7.2.1

EMERGENCE OF 3D CAMERAS WITH HIGH-PRECISION VISION TO DRIVE MARKET

7.2.2

INTERFACE STANDARDS

7.2.2.1

USB 2.0

7.2.2.2

USB 3.0

7.2.2.3

CAMERA LINK

7.2.2.4

CAMERA LINK HS

7.2.2.5

GIGE

7.2.2.6

10 GIGE & 25 GIGE BANDWIDTH OVER GIGE VISION

7.2.2.7

OTHERS

7.2.3

IMAGING SPECTRUM

7.2.3.1

VISIBLE LIGHT

7.2.3.2

VISIBLE + IR/IR

7.2.4

FRAME RATE

7.2.4.1

LESS THAN 25 FRAMES PER SECOND

7.2.4.2

25–125 FRAMES PER SECOND

7.2.4.3

MORE THAN 125 FRAMES PER SECOND

7.2.5

FORMAT

7.2.5.1

LINE SCAN

7.2.5.2

AREA SCAN

7.2.6

SENSOR

7.2.6.1

COMPLEMENTARY METAL OXIDE SEMICONDUCTOR (CMOS)

7.2.6.2

CHARGED-COUPLED DEVICE (CCD)

7.3

FRAME GRABBERS

7.3.1

INCREASING ADOPTION IN HIGH-SPEED AND LARGE-SCALE MACHINE VISION SYSTEMS TO DRIVE MARKET

7.4

LED LIGHTING

7.4.1

INCREASING ADOPTION OF STRUCTURED LIGHTING SOLUTIONS TO FUEL DEMAND

7.5

OPTICS

7.5.1

GROWING INTEGRATION WITH CAMERA BODIES FOR OBJECT IMAGE CAPTURE TO FUEL DEMAND

7.6

PROCESSORS

7.6.1

ADOPTION OF ADVANCED VISION SYSTEMS FUELING DEMAND FOR HIGH-PERFORMANCE PROCESSORS

7.6.2

FIELD-PROGRAMMABLE GATE ARRAY (FPGA)

7.6.3

DIGITAL SIGNAL PROCESSOR (DSP)

7.6.4

MICROCONTROLLER AND MICROPROCESSOR

7.6.5

VISION PROCESSING UNIT

7.7

OTHER HARDWARE COMPONENTS

7.7.1

NEED TO ENHANCE SYSTEM RELIABILITY AND PERFORMANCE TO FUEL SEGMENTAL GROWTH

7.8

SOFTWARE

7.8.1

AI-BASED MACHINE VISION SOFTWARE

8

MACHINE VISION MARKET, BY VISION TYPE

Market Size & Growth Rate Forecast Analysis

120

8.1

INTRODUCTION

8.2

1D VISION SYSTEMS

8.2.1

APPLICATION IN PRECISE LINEAR INSPECTION IN MANUFACTURING TO DRIVE DEMAND

8.3

2D VISION SYSTEMS

8.3.1

ADVANCEMENTS IN EMBEDDED VISION AND SMART CAMERA TECHNOLOGIES TO SUPPORT MARKET GROWTH

8.4

3D VISION SYSTEMS

8.4.1

RISING ADOPTION IN DEPTH ANALYSIS AND SURFACE INSPECTION TO FUEL DEMAND

9

MACHINE VISION MARKET, BY DEPLOYMENT

Market Size & Growth Rate Forecast Analysis

122

9.1

INTRODUCTION

9.2

GENERAL

9.2.1

RISING DEMAND FOR AUTOMATED INSPECTIONS TO DRIVE MARKET GROWTH

9.3

ROBOTIC CELL

9.3.1

RISING AUTOMATION AND TECHNOLOGICAL ADVANCEMENTS TO PROPEL MACHINE VISION ADOPTION

10

MACHINE VISION MARKET, BY SYSTEM TYPE

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 6 Data Tables

124

10.1

INTRODUCTION

10.2

PC-BASED

10.2.1

ADVANCED PROCESSING WITH MULTI-CAMERA SUPPORT TO DRIVE ADOPTION OF PC-BASED VISION SYSTEMS

10.3

SMART CAMERA-BASED

10.3.1

RISING ADOPTION OF SMART CAMERA IN IMAGING AND SECURITY APPLICATIONS TO DRIVE MARKET

11

MACHINE VISION MARKET, BY INDUSTRY

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 50 Data Tables

130

11.1

INTRODUCTION

11.2

AUTOMOTIVE

11.2.1

NEED FOR ENHANCING ACCURACY AND PRODUCTIVITY TO INCREASE ADOPTION

11.3

ELECTRONICS & SEMICONDUCTORS

11.3.1

RISING NEED TO IMPROVE ELECTRONIC MANUFACTURING BY IDENTIFYING DEFECTS AND ENHANCING SEMICONDUCTOR PRODUCTION

11.4

CONSUMER PRODUCTS

11.4.1

GROWING DEMAND FOR AUTOMATED INSPECTION TO IMPROVE ELECTRONIC ASSEMBLY TO DRIVE MARKET

11.5

METALS

11.5.1

SHORTAGE OF SKILLED LABOR FUELING ADOPTION OF MACHINE VISION SYSTEMS TO BOOST PRODUCT QUALITY

11.6

HEALTHCARE

11.6.1

STRINGENT GOVERNMENT REGULATION AND GROWING NEED TO COMBAT COUNTERFEIT PRODUCTS TO DRIVE MARKET

11.7

FOOD & BEVERAGES

11.7.1

FOOD

11.7.1.1

NEED TO REDUCE LABOR COST AND ENHANCE FOOD PROCESSING FUELING ADOPTION

11.7.2

BEVERAGES

11.7.2.1

NEED TO ENSURE QUALITY AND HYGIENE IN BEVERAGE PRODUCTION TO FUEL MARKET GROWTH

11.8

RUBBER & PLASTICS

11.8.1

INCREASING CONSUMPTION OF PLASTICS IN VARIOUS INDUSTRIAL SECTORS TO SUPPORT MARKET GROWTH

11.9

PRINTING

11.9.1

MACHINE VISION SYSTEMS INCREASINGLY USED TO MAINTAIN QUALITY IN PRINTING OPERATIONS

11.10

MACHINERY

11.10.1

GROWING NEED TO ENHANCE MACHINERY PERFORMANCE AND SAFETY TO FUEL DEMAND

11.11

SOLAR PANEL MANUFACTURING

11.11.1

NEED FOR INCREASED PRODUCTION AND QUALITY OF SOLAR PANELS TO BOOST MARKET GROWTH

11.12

LOGISTICS

11.12.1

GROWING DEMAND FOR AUTOMATED SORTING AND TRACKING TO DRIVE MARKET

11.13

OTHER INDUSTRIES

11.13.1

INCREASING ADOPTION OF MACHINE VISION FOR DEFECT DETECTION AND QUALITY CONTROL TO SUPPORT MARKET GROWTH

12

MACHINE VISION MARKET, BY REGION

Comprehensive coverage of 8 Regions with country-level deep-dive of 22 Countries | 78 Data Tables.

153

12.1

INTRODUCTION

12.2

NORTH AMERICA

12.2.1

MACROECONOMIC OUTLOOK FOR NORTH AMERICA

12.2.2

US

12.2.2.1

EXPANDING ROLE OF MACHINE VISION IN HEALTHCARE AND AUTOMOTIVE APPLICATIONS TO DRIVE MARKET

12.2.3

CANADA

12.2.3.1

INCREASING ADOPTION IN AUTOMOTIVE, ELECTRONICS, AND HEALTHCARE INDUSTRIES TO BOOST DEMAND

12.2.4

MEXICO

12.2.4.1

GROWING EMPHASIS ON HIGH-QUALITY STANDARDS AND OPERATIONAL EFFICIENCY TO FUEL ADOPTION

12.3

EUROPE

12.3.1

MACROECONOMIC OUTLOOK FOR EUROPE

12.3.2

GERMANY

12.3.2.1

INCREASING ADOPTION TO ENHANCE OPERATIONAL EFFICIENCY AND PRECISION IN INDUSTRIAL APPLICATIONS TO DRIVE MARKET

12.3.3

UK

12.3.3.1

RISING ADOPTION IN AUTOMOTIVE AND MANUFACTURING SECTORS TO FUEL MARKET GROWTH

12.3.4

FRANCE

12.3.4.1

GROWTH IN ELECTRIC VEHICLE MARKET AND PORTABLE ELECTRONICS DRIVING MACHINE VISION ADOPTION

12.3.5

ITALY

12.3.5.1

GOVERNMENT INITIATIVES DRIVING ADOPTION OF ADVANCED MANUFACTURING TECHNOLOGIES

12.3.6

SPAIN

12.3.6.1

GROWTH OF CONSUMER ELECTRONICS AND PHARMACEUTICAL INDUSTRIES FUELING MACHINE VISION ADOPTION

12.3.7

NETHERLANDS

12.3.7.1

RISING ADOPTION IN LOGISTICS, FOOD PROCESSING, AND ELECTRONICS SECTORS TO DRIVE MARKET

12.3.8

SWITZERLAND

12.3.8.1

INCREASED INTEGRATION OF MACHINE VISION IN PRECISION MANUFACTURING AND PHARMACEUTICAL AUTOMATION TO BOOST MARKET

12.3.9

NORDICS

12.3.9.1

STRONG PUSH FOR INDUSTRIAL AUTOMATION FUELING DEMAND ACROSS MANUFACTURING AND ENERGY SECTORS

12.3.10

REST OF EUROPE

12.4

ASIA PACIFIC

12.4.1

MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

12.4.2

CHINA

12.4.2.1

EXPANDING DEPLOYMENT OF MACHINE VISION SYSTEMS FOR HIGHER PRODUCTIVITY AND QUALITY ENHANCEMENT

12.4.3

JAPAN

12.4.3.1

INCREASING ADOPTION IN CONSUMER ELECTRONICS SECTOR TO BOOST MARKET GROWTH

12.4.4

SOUTH KOREA

12.4.4.1

ADOPTION OF MACHINE VISION SYSTEMS EXPANDING IN KEY SECTORS TO ENSURE QUALITY COMPLIANCE

12.4.5

INDIA

12.4.5.1

GOVERNMENT INITIATIVES DRIVING FACTORY AUTOMATION GROWTH

12.4.6

INDONESIA

12.4.6.1

EMERGING INDUSTRIAL BASE AND RISING AUTOMATION NEEDS DRIVING MACHINE VISION ADOPTION

12.4.7

SINGAPORE

12.4.7.1

TECHNOLOGICAL LEADERSHIP AND ADVANCED INFRASTRUCTURE SUPPORTING MARKET GROWTH

12.4.8

AUSTRALIA

12.4.8.1

EXPANDING APPLICATIONS IN FOOD & BEVERAGES AND ELECTRONICS INDUSTRIES TO DRIVE DEMAND

12.4.9

REST OF ASIA PACIFIC

12.5

ROW

12.5.1

MACROECONOMIC OUTLOOK FOR ROW

12.5.2

MIDDLE EAST

12.5.2.1

SAUDI ARABIA

12.5.2.2

UAE

12.5.2.3

BAHRAIN

12.5.2.4

KUWAIT

12.5.2.5

OMAN

12.5.2.6

QATAR

12.5.2.7

REST OF MIDDLE EAST

12.5.3

SOUTH AMERICA

12.5.3.1

BRAZIL

12.5.3.2

ARGENTINA

12.5.3.3

OTHER SOUTH AMERICAN COUNTRIES

12.5.4

AFRICA

12.5.4.1

SOUTH AFRICA

12.5.4.2

OTHER AFRICAN COUNTRIES

13

COMPETITIVE LANDSCAPE

Uncover top players' strategies and market share dynamics shaping the competitive landscape.

218

13.1

INTRODUCTION

13.2

KEY PLAYER STRATEGIES/RIGHT TO WIN, JANUARY 2021–MARCH 2025

13.3

REVENUE ANALYSIS, 2020–2024

13.4

MARKET SHARE ANALYSIS OF TOP FIVE PLAYERS, 2024

13.5

PRODUCT COMPARISON

13.6

COMPANY VALUATION AND FINANCIAL METRICS

13.7

COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

13.7.1

STARS

13.7.2

EMERGING LEADERS

13.7.3

PERVASIVE PLAYERS

13.7.4

PARTICIPANTS

13.7.5

COMPANY FOOTPRINT: KEY PLAYERS, 2024

13.7.5.1

COMPANY FOOTPRINT

13.7.5.2

REGION FOOTPRINT

13.7.5.3

SYSTEM TYPE FOOTPRINT

13.7.5.4

COMPONENT FOOTPRINT

13.7.5.5

INDUSTRY FOOTPRINT

13.8

COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

13.8.1

PROGRESSIVE COMPANIES

13.8.2

RESPONSIVE COMPANIES

13.8.3

DYNAMIC COMPANIES

13.8.4

STARTING BLOCKS

13.8.5

COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

13.8.5.1

DETAILED LIST OF KEY STARTUPS/SMES

13.8.5.2

COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

13.9

COMPETITIVE SCENARIO

13.9.1

PRODUCT LAUNCHES

13.9.2

DEALS

14

COMPANY PROFILES

In-depth Company Profiles of Leading Market Players with detailed Business Overview, Product and Service Portfolio, Recent Developments, and Unique Analyst Perspective (MnM View)

241

14.1

KEY PLAYERS

14.1.1

COGNEX CORPORATION

14.1.1.1

BUSINESS OVERVIEW

14.1.1.2

PRODUCTS/SOLUTIONS/SERVICES OFFERED

14.1.1.3

RECENT DEVELOPMENTS

14.1.1.4

MNM VIEW

14.1.2

BASLER AG

14.1.3

KEYENCE CORPORATION

14.1.4

TELEDYNE TECHNOLOGIES INC.

14.1.5

OMRON CORPORATION

14.1.6

TKH

14.1.7

SICK AG

14.1.8

SONY GROUP CORPORATION

14.1.9

TEXAS INSTRUMENTS INCORPORATED

14.1.10

ATLAS COPCO AB

14.1.11

AMETEK.INC.

14.1.12

EMERSON ELECTRIC CO.

14.1.13

CANON INC.

14.1.14

ZEBRA TECHNOLOGIES CORP.

14.2

OTHER PLAYERS

14.2.1

QUALITAS TECHNOLOGIES

14.2.2

BAUMER

14.2.3

TORDIVEL AS

14.2.4

MVTEC SOFTWARE GMBH

14.2.5

JAI A/S

14.2.6

INDUSTRIAL VISION SYSTEMS

14.2.7

IVISYS

14.2.8

USS VISION LLC

14.2.9

OPTOTUNE

14.2.10

IDS IMAGING DEVELOPMENT SYSTEMS GMBH

14.2.11

INTELGIC INC.

15

APPENDIX

302

15.1

INSIGHTS FROM INDUSTRY EXPERTS

15.2

DISCUSSION GUIDE

15.3

KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

15.4

CUSTOMIZATION OPTIONS

15.5

RELATED REPORTS

15.6

AUTHOR DETAILS

LIST OF TABLES

TABLE 1

MACHINE VISION MARKET: RESEARCH ASSUMPTIONS

TABLE 2

MACHINE VISION MARKET: RISK ANALYSIS

TABLE 3

INDICATING PRICING OF MACHINE VISION KEY COMPONENT (CAMERA), BY KEY PLAYERS, 2024

TABLE 4

AVERAGE SELLING PRICE TREND OF MACHINE VISION HARDWARE COMPONENT, 2021–2024 (USD)

TABLE 5

AVERAGE SELLING PRICE TREND OF MACHINE VISION HARDWARE COMPONENT, BY REGION, 2021–2024 (USD)

TABLE 6

MACHINE VISION MARKET: ROLE OF COMPANIES IN ECOSYSTEM

TABLE 7

LIST OF MAJOR PATENTS, 2021–2024

TABLE 8

IMPORT DATA FOR HS CODE 852580-COMPLIANT PRODUCTS, BY COUNTRY, 2019–2023 (USD MILLION)

TABLE 9

EXPORT DATA FOR HS CODE 852580-COMPLIANT PRODUCTS, BY COUNTRY, 2019–2023 (USD MILLION)

TABLE 10

LIST OF KEY CONFERENCES AND EVENTS, 2025–2026

TABLE 11

NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 12

EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 13

ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 14

ROW: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 15

STANDARDS

TABLE 16

MACHINE VISION MARKET: IMPACT OF PORTER'S FIVE FORCES

TABLE 17

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE INDUSTRIES (%)

TABLE 18

KEY BUYING CRITERIA FOR TOP THREE INDUSTRIES

TABLE 19

US-ADJUSTED RECIPROCAL TARIFF RATES

TABLE 20

KEY PRODUCT-RELATED TARIFF EFFECTIVE FOR MACHINE VISION

TABLE 21

MACHINE VISION MARKET, BY COMPONENT, 2021–2024 (USD MILLION)

TABLE 22

MACHINE VISION MARKET, BY COMPONENT, 2025–2030 (USD MILLION)

TABLE 23

MACHINE VISION MARKET, BY HARDWARE COMPONENT, 2021–2024 (MILLION UNITS)

TABLE 24

MACHINE VISION MARKET, BY HARDWARE COMPONENT, 2025–2030 (MILLION UNITS)

TABLE 25

CAMERAS: MACHINE VISION MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 26

CAMERAS: MACHINE VISION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 27

CAMERAS: MACHINE VISION HARDWARE MARKET, BY IMAGING SPECTRUM, 2021–2024 (USD MILLION)

TABLE 28

CAMERAS: MACHINE VISION HARDWARE MARKET, BY IMAGING SPECTRUM, 2025–2030 (USD MILLION)

TABLE 29

CAMERAS: MACHINE VISION HARDWARE MARKET, BY FRAME RATE, 2021–2024 (USD MILLION)

TABLE 30

CAMERAS: MACHINE VISION HARDWARE MARKET, BY FRAME RATE, 2025–2030 (USD MILLION)

TABLE 31

CAMERAS: MACHINE VISION HARDWARE MARKET, BY FORMAT, 2021–2024 (USD MILLION)

TABLE 32

CAMERAS: MACHINE VISION HARDWARE MARKET, BY FORMAT, 2025–2030 (USD MILLION)

TABLE 33

FRAME GRABBERS: MACHINE VISION MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 34

FRAME GRABBERS: MACHINE VISION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 35

LED LIGHTING: MACHINE VISION MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 36

LED LIGHTING: MACHINE VISION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 37

OPTICS: MACHINE VISION MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 38

OPTICS: MACHINE VISION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 39

PROCESSORS: MACHINE VISION MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 40

PROCESSORS: MACHINE VISION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 41

OTHER HARDWARE COMPONENTS: MACHINE VISION MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 42

OTHER HARDWARE COMPONENTS: MACHINE VISION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 43

SOFTWARE: MACHINE VISION MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 44

SOFTWARE: MACHINE VISION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 45

MACHINE VISION MARKET, BY SYSTEM TYPE, 2021–2024 (USD MILLION)

TABLE 46

MACHINE VISION MARKET, BY SYSTEM TYPE, 2025–2030 (USD MILLION)

TABLE 47

PC-BASED: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 48

PC-BASED: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 49

SMART CAMERA-BASED: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 50

SMART CAMERA-BASED: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 51

MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 52

MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 53

AUTOMOTIVE: MACHINE VISION MARKET, BY SYSTEM TYPE, 2021–2024 (USD MILLION)

TABLE 54

AUTOMOTIVE: MACHINE VISION MARKET, BY SYSTEM TYPE, 2025–2030 (USD MILLION)

TABLE 55

AUTOMOTIVE: MACHINE VISION MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 56

AUTOMOTIVE: MACHINE VISION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 57

ELECTRONICS & SEMICONDUCTORS: MACHINE VISION MARKET, BY SYSTEM TYPE, 2021–2024 (USD MILLION)

TABLE 58

ELECTRONICS & SEMICONDUCTORS: MACHINE VISION MARKET, BY SYSTEM TYPE, 2025–2030 (USD MILLION)

TABLE 59

ELECTRONICS & SEMICONDUCTORS: MACHINE VISION MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 60

ELECTRONICS & SEMICONDUCTORS: MACHINE VISION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 61

CONSUMER PRODUCTS: MACHINE VISION MARKET, BY SYSTEM TYPE, 2021–2024 (USD MILLION)

TABLE 62

CONSUMER PRODUCTS: MACHINE VISION MARKET, BY SYSTEM TYPE, 2025–2030 (USD MILLION)

TABLE 63

CONSUMER PRODUCTS: MACHINE VISION MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 64

CONSUMER PRODUCTS: MACHINE VISION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 65

METALS: MACHINE VISION MARKET, BY SYSTEM TYPE, 2021–2024 (USD MILLION)

TABLE 66

METALS: MACHINE VISION MARKET, BY SYSTEM TYPE, 2025–2030 (USD MILLION)

TABLE 67

METALS: MACHINE VISION MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 68

METALS: MACHINE VISION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 69

HEALTHCARE: MACHINE VISION MARKET, BY SYSTEM TYPE, 2021–2024 (USD MILLION)

TABLE 70

HEALTHCARE: MACHINE VISION MARKET, BY SYSTEM TYPE, 2025–2030 (USD MILLION)

TABLE 71

HEALTHCARE: MACHINE VISION MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 72

HEALTHCARE: MACHINE VISION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 73

FOOD & BEVERAGE: MACHINE VISION MARKET, BY SYSTEM TYPE, 2021–2024 (USD MILLION)

TABLE 74

FOOD & BEVERAGE: MACHINE VISION MARKET, BY SYSTEM TYPE, 2025–2030 (USD MILLION)

TABLE 75

FOOD & BEVERAGE: MACHINE VISION MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 76

FOOD & BEVERAGE: MACHINE VISION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 77

RUBBER & PLASTICS: MACHINE VISION MARKET, BY SYSTEM TYPE, 2021–2024 (USD MILLION)

TABLE 78

RUBBER & PLASTICS: MACHINE VISION MARKET, BY SYSTEM TYPE, 2025–2030 (USD MILLION)

TABLE 79

RUBBER & PLASTICS: MACHINE VISION MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 80

RUBBER & PLASTICS: MACHINE VISION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 81

PRINTING: MACHINE VISION MARKET, BY SYSTEM TYPE, 2021–2024 (USD MILLION)

TABLE 82

PRINTING: MACHINE VISION MARKET, BY SYSTEM TYPE, 2025–2030 (USD MILLION)

TABLE 83

PRINTING: MACHINE VISION MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 84

PRINTING: MACHINE VISION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 85

MACHINERY: MACHINE VISION MARKET, BY SYSTEM TYPE, 2021–2024 (USD MILLION)

TABLE 86

MACHINERY: MACHINE VISION MARKET, BY SYSTEM TYPE, 2025–2030 (USD MILLION)

TABLE 87

MACHINERY: MACHINE VISION MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 88

MACHINERY: MACHINE VISION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 89

SOLAR PANEL MANUFACTURING: MACHINE VISION MARKET, BY SYSTEM TYPE, 2021–2024 (USD MILLION)

TABLE 90

SOLAR PANEL MANUFACTURING: MACHINE VISION MARKET, BY SYSTEM TYPE, 2025–2030 (USD MILLION)

TABLE 91

SOLAR PANEL MANUFACTURING: MACHINE VISION MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 92

SOLAR PANEL MANUFACTURING: MACHINE VISION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 93

LOGISTICS: MACHINE VISION MARKET, BY SYSTEM TYPE, 2021–2024 (USD MILLION)

TABLE 94

LOGISTICS: MACHINE VISION MARKET, BY SYSTEM TYPE, 2025–2030 (USD MILLION)

TABLE 95

LOGISTICS: MACHINE VISION MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 96

LOGISTICS: MACHINE VISION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 97

OTHER INDUSTRIES: MACHINE VISION MARKET, BY SYSTEM TYPE, 2021–2024 (USD MILLION)

TABLE 98

OTHER INDUSTRIES: MACHINE VISION MARKET, BY SYSTEM TYPE, 2025–2030 (USD MILLION)

TABLE 99

OTHER INDUSTRIES: MACHINE VISION MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 100

OTHER INDUSTRIES: MACHINE VISION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 101

MACHINE VISION MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 102

MACHINE VISION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 103

NORTH AMERICA: MACHINE VISION MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 104

NORTH AMERICA: MACHINE VISION MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 105

NORTH AMERICA: MACHINE VISION MARKET, BY COMPONENT, 2021–2024 (USD MILLION)

TABLE 106

NORTH AMERICA: MACHINE VISION MARKET, BY COMPONENT, 2025–2030 (USD MILLION)

TABLE 107

NORTH AMERICA: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 108

NORTH AMERICA: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 109

US: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 110

US: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 111

CANADA: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 112

CANADA: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 113

MEXICO: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 114

MEXICO: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 115

EUROPE: MACHINE VISION MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 116

EUROPE: MACHINE VISION MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 117

EUROPE: MACHINE VISION MARKET, BY COMPONENT, 2021–2024 (USD MILLION)

TABLE 118

EUROPE: MACHINE VISION MARKET, BY COMPONENT, 2025–2030 (USD MILLION)

TABLE 119

EUROPE: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 120

EUROPE: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 121

GERMANY: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 122

GERMANY: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 123

UK: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 124

UK: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 125

FRANCE: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 126

FRANCE: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 127

ITALY: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 128

ITALY: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 129

SPAIN: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 130

SPAIN: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 131

NETHERLANDS: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 132

NETHERLANDS: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 133

SWITZERLAND: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 134

SWITZERLAND: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 135

NORDICS: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 136

NORDICS: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 137

REST OF EUROPE: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 138

REST OF EUROPE: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 139

ASIA PACIFIC: MACHINE VISION MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 140

ASIA PACIFIC: MACHINE VISION MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 141

ASIA PACIFIC: MACHINE VISION MARKET, BY COMPONENT, 2021–2024 (USD MILLION)

TABLE 142

ASIA PACIFIC: MACHINE VISION MARKET, BY COMPONENT, 2025–2030 (USD MILLION)

TABLE 143

ASIA PACIFIC: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 144

ASIA PACIFIC: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 145

CHINA: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 146

CHINA: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 147

JAPAN: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 148

JAPAN: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 149

SOUTH KOREA: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 150

SOUTH KOREA: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 151

INDIA: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 152

INDIA: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 153

INDONESIA: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 154

INDONESIA: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 155

SINGAPORE: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 156

SINGAPORE: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 157

AUSTRALIA: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 158

AUSTRALIA: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 159

REST OF ASIA PACIFIC: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 160

REST OF ASIA PACIFIC: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 161

ROW: MACHINE VISION MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 162

ROW: MACHINE VISION MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 163

ROW: MACHINE VISION MARKET, BY COMPONENT, 2021–2024 (USD MILLION)

TABLE 164

ROW: MACHINE VISION MARKET, BY COMPONENT, 2025–2030 (USD MILLION)

TABLE 165

ROW: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 166

ROW: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 167

MIDDLE EAST: MACHINE VISION MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 168

MIDDLE EAST: MACHINE VISION MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 169

MIDDLE EAST: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 170

MIDDLE EAST: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 171

SOUTH AMERICA: MACHINE VISION MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 172

SOUTH AMERICA: MACHINE VISION MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 173

SOUTH AMERICA: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 174

SOUTH AMERICA: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 175

AFRICA: MACHINE VISION MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 176

AFRICA: MACHINE VISION MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 177

AFRICA: MACHINE VISION MARKET, BY INDUSTRY, 2021–2024 (USD MILLION)

TABLE 178

AFRICA: MACHINE VISION MARKET, BY INDUSTRY, 2025–2030 (USD MILLION)

TABLE 179

MACHINE VISION MARKET: OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS, JANUARY 2021–MARCH 2025

TABLE 180

MACHINE VISION MARKET: DEGREE OF COMPETITION

TABLE 181

MACHINE VISION MARKET: REGION FOOTPRINT

TABLE 182

MACHINE VISION MARKET: SYSTEM TYPE FOOTPRINT

TABLE 183

MACHINE VISION MARKET: COMPONENT FOOTPRINT

TABLE 184

MACHINE VISION MARKET: INDUSTRY FOOTPRINT

TABLE 185

MACHINE VISION MARKET: DETAILED LIST OF KEY STARTUPS/SMES

TABLE 186

MACHINE VISION MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

TABLE 187

MACHINE VISION MARKET: PRODUCT LAUNCHES, JANUARY 2021–MARCH 2025

TABLE 188

MACHINE VISION MARKET: DEALS, JANUARY 2021–MARCH 2025

TABLE 189

COGNEX CORPORATION: COMPANY OVERVIEW

TABLE 190

COGNEX CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 191

COGNEX CORPORATION: PRODUCT LAUNCHES

TABLE 192

BASLER AG: COMPANY OVERVIEW

TABLE 193

BASLER AG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 194

BASLER AG: PRODUCT LAUNCHES

TABLE 195

BASLER AG: DEALS

TABLE 196

KEYENCE CORPORATION: COMPANY OVERVIEW

TABLE 197

KEYENCE CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 198

KEYENCE CORPORATION: PRODUCT LAUNCHES

TABLE 199

TELEDYNE TECHNOLOGIES INC.: COMPANY OVERVIEW

TABLE 200

TELEDYNE TECHNOLOGIES INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 201

TELEDYNE TECHNOLOGIES INC.: PRODUCT LAUNCHES

TABLE 202

OMRON CORPORATION: COMPANY OVERVIEW

TABLE 203

OMRON CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 204

OMRON CORPORATION: PRODUCT LAUNCHES

TABLE 205

OMRON CORPORATION: DEALS

TABLE 206

TKH: COMPANY OVERVIEW

TABLE 207

TKH: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 208

TKH: PRODUCT LAUNCHES

TABLE 209

TKH: DEALS

TABLE 210

SICK AG: COMPANY OVERVIEW

TABLE 211

SICK AG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 212

SICK AG: PRODUCT LAUNCHES

TABLE 213

SICK AG: DEALS

TABLE 214

SONY GROUP CORPORATION: COMPANY OVERVIEW

TABLE 215

SONY GROUP CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 216

SONY GROUP CORPORATION: PRODUCT LAUNCHES

TABLE 217

TEXAS INSTRUMENTS INCORPORATED: COMPANY OVERVIEW

TABLE 218

TEXAS INSTRUMENTS INCORPORATED: PRODUCTS/SOLUTIONS/ SERVICES OFFERED

TABLE 219

TEXAS INSTRUMENTS INCORPORATED: PRODUCT LAUNCHES

TABLE 220

ATLAS COPCO AB: COMPANY OVERVIEW

TABLE 221

ATLAS COPCO AB: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 222

AMETEK.INC.: COMPANY OVERVIEW

TABLE 223

AMETEK.INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 224

EMERSON ELECTRIC CO.: COMPANY OVERVIEW

TABLE 225

EMERSON ELECTRIC CO.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 226

EMERSON ELECTRIC CO.: DEALS

TABLE 227

CANON INC.: COMPANY OVERVIEW

TABLE 228

CANON INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 229

ZEBRA TECHNOLOGIES CORP.: COMPANY OVERVIEW

TABLE 230

ZEBRA TECHNOLOGIES CORP.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

TABLE 231

ZEBRA TECHNOLOGIES CORP.: PRODUCT LAUNCHES

TABLE 232

ZEBRA TECHNOLOGIES CORP.: DEALS

LIST OF FIGURES

FIGURE 1

MACHINE VISION MARKET SEGMENTATION AND REGIONAL SCOPE

FIGURE 2

MACHINE VISION MARKET: RESEARCH DESIGN

FIGURE 3

MACHINE VISION MARKET: RESEARCH APPROACH

FIGURE 4

MACHINE VISION MARKET: BOTTOM-UP APPROACH

FIGURE 5

MACHINE VISION MARKET: TOP-DOWN APPROACH

FIGURE 6

MACHINE VISION MARKET SIZE ESTIMATION METHODOLOGY

FIGURE 7

MACHINE VISION MARKET: DATA TRIANGULATION

FIGURE 8

MACHINE VISION MARKET SIZE, 2021–2030

FIGURE 9

CAMERAS SEGMENT TO ACCOUNT FOR LARGEST SHARE OF MACHINE VISION MARKET FROM 2025 TO 2030

FIGURE 10

SMART CAMERA-BASED SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

FIGURE 11

FOOD & BEVERAGES SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

FIGURE 12

ASIA PACIFIC ACCOUNTED FOR LARGEST SHARE OF MACHINE VISION MARKET IN 2024

FIGURE 13

GROWING AUTOMATION OF INDUSTRIAL PROCESSES TO DRIVE ADOPTION OF MACHINE VISION SOLUTIONS

FIGURE 14

CAMERAS SEGMENT TO ACCOUNT FOR LARGEST SHARE OF MACHINE VISION MARKET DURING FORECAST PERIOD

FIGURE 15

FOOD & BEVERAGES SEGMENT TO BE LARGEST END USER DURING FORECAST PERIOD

FIGURE 16

US DOMINATED NORTH AMERICAN MACHINE VISION MARKET IN 2024

FIGURE 17

INDIA TO EXHIBIT HIGHEST CAGR IN GLOBAL MACHINE VISION MARKET DURING FORECAST PERIOD

FIGURE 18

DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

FIGURE 19

ANNUAL INSTALLATION OF INDUSTRIAL ROBOTICS, 2019–2023

FIGURE 20

IMPACT ANALYSIS: DRIVERS

FIGURE 21

IMPACT ANALYSIS: RESTRAINTS

FIGURE 22

IMPACT ANALYSIS: OPPORTUNITIES

FIGURE 23

IMPACT ANALYSIS: CHALLENGES

FIGURE 24

TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

FIGURE 25

AVERAGE SELLING PRICE TREND OF MACHINE VISION HARDWARE COMPONENT, 2021–2024

FIGURE 26

AVERAGE SELLING PRICE TREND OF MACHINE VISION HARDWARE COMPONENT, BY REGION, 2020−2024

FIGURE 27

MACHINE VISION MARKET: VALUE CHAIN ANALYSIS

FIGURE 28

MACHINE VISION MARKET: ECOSYSTEM ANALYSIS

FIGURE 29

INVESTMENT AND FUNDING SCENARIO, 2021–2024

FIGURE 30

PATENTS APPLIED AND GRANTED, 2015–2024

FIGURE 31

IMPORT DATA FOR HS CODE 852580-COMPLIANT PRODUCTS FOR TOP FIVE COUNTRIES, 2019–2023

FIGURE 32

EXPORT DATA FOR HS CODE 852580-COMPLIANT PRODUCTS FOR TOP FIVE COUNTRIES, 2019–2023

FIGURE 33

MACHINE VISION MARKET: PORTER'S FIVE FORCES ANALYSIS

FIGURE 34

INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE INDUSTRIES

FIGURE 35

KEY BUYING CRITERIA FOR TOP THREE INDUSTRIES

FIGURE 36

AI USE CASES IN MACHINE VISION

FIGURE 37

MACHINE VISION MARKET, BY APPLICATION

FIGURE 38

MACHINE VISION MARKET, BY COMPONENT

FIGURE 39

SOFTWARE SEGMENT TO WITNESS SIGNIFICANT GROWTH DURING FORECAST PERIOD

FIGURE 40

MACHINE VISION MARKET, BY VISION TYPE

FIGURE 41

MACHINE VISION MARKET, BY DEPLOYMENT

FIGURE 42

MACHINE VISION MARKET, BY SYSTEM TYPE

FIGURE 43

SMART CAMERA-BASED SEGMENT TO REGISTER HIGHER CAGR FROM 2025 TO 2030

FIGURE 44

MACHINE VISION MARKET, BY INDUSTRY

FIGURE 45

FOOD & BEVERAGES SEGMENT TO ACCOUNT FOR LARGEST SHARE OF MACHINE VISION MARKET

FIGURE 46

MACHINE VISION MARKET, BY REGION

FIGURE 47

INDIA TO EXHIBIT HIGHEST CAGR IN GLOBAL MACHINE VISION MARKET DURING FORECAST PERIOD

FIGURE 48

NORTH AMERICA: MACHINE VISION MARKET SNAPSHOT

FIGURE 49

US TO DOMINATE NORTH AMERICAN MACHINE VISION MARKET FROM 2025 TO 2030

FIGURE 50

EUROPE: MACHINE VISION MARKET SNAPSHOT

FIGURE 51

GERMANY TO ACCOUNT FOR LARGEST SHARE OF EUROPEAN MACHINE VISION MARKET DURING FORECAST PERIOD

FIGURE 52

ASIA PACIFIC: MACHINE VISION MARKET SNAPSHOT

FIGURE 53

CHINA TO BE LARGEST MACHINE VISION MARKET IN ASIA PACIFIC BETWEEN 2025 AND 2030

FIGURE 54

SOUTH AMERICA TO DOMINATE MACHINE VISION MARKET IN ROW MARKET DURING FORECAST PERIOD

FIGURE 55

MACHINE VISION MARKET: REVENUE ANALYSIS OF FIVE KEY PLAYERS, 2020–2024

FIGURE 56

MACHINE VISION MARKET SHARE ANALYSIS, 2024

FIGURE 57

PRODUCT COMPARISON

FIGURE 58

COMPANY VALUATION

FIGURE 59

FINANCIAL METRICS (EV/EBITDA)

FIGURE 60

MACHINE VISION MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

FIGURE 61

MACHINE VISION MARKET: COMPANY FOOTPRINT

FIGURE 62

MACHINE VISION MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

FIGURE 63

COGNEX CORPORATION: COMPANY SNAPSHOT

FIGURE 64

BASLER AG: COMPANY SNAPSHOT

FIGURE 65

KEYENCE CORPORATION: COMPANY SNAPSHOT

FIGURE 66

TELEDYNE TECHNOLOGIES INC.: COMPANY SNAPSHOT

FIGURE 67

OMRON CORPORATION: COMPANY SNAPSHOT

FIGURE 68

TKH: COMPANY SNAPSHOT

FIGURE 69

SICK AG: COMPANY SNAPSHOT

FIGURE 70

SONY GROUP CORPORATION: COMPANY SNAPSHOT

FIGURE 71

TEXAS INSTRUMENTS INCORPORATED: COMPANY SNAPSHOT

FIGURE 72

ATLAS COPCO AB: COMPANY SNAPSHOT

FIGURE 73

AMETEK.INC.: COMPANY SNAPSHOT

FIGURE 74

EMERSON ELECTRIC CO.: COMPANY SNAPSHOT

FIGURE 75

CANON INC.: COMPANY SNAPSHOT

FIGURE 76

ZEBRA TECHNOLOGIES CORP.: COMPANY SNAPSHOT

Methodology

The study involved four major activities for estimating the current size of the machine vision market. Exhaustive secondary research has been done to collect information on the market. The next step is to validate these findings, assumptions, and size with industry experts across the value chain through primary research. Both the top-down and bottom-up approaches have been employed to estimate the complete market size. After that, market breakdown and data triangulation methods have been used to estimate the market size of the segments and subsegments. Two sources of information, secondary and primary, have been used to identify and collect information for an extensive technical and commercial study of the machine vision market.

Secondary Research

Various secondary sources have been referred to in the secondary research process to identify and collect information important for this study. The secondary sources include annual reports, press releases, and investor presentations of companies; white papers; journals and certified publications; and articles from recognized authors, websites, directories, and databases. Secondary research has been conducted to obtain key information about the industry’s supply chain, the market’s value chain, the total pool of key players, market segmentation according to the industry trends (to the bottom-most level), regional markets, and key developments from market- and technology-oriented perspectives. Secondary data has been collected and analyzed to determine the overall market size, which is further validated through primary research.

Primary Research

Extensive primary research was conducted after gaining knowledge about the current scenario of the machine vision market through secondary research. Several primary interviews were conducted with experts from the demand and supply sides across four major regions North America, Europe, Asia Pacific, and RoW. This primary data was collected through questionnaires, emails, and telephonic interviews.

To know about the assumptions considered for the study, download the pdf brochure

Market Size Estimation

Both the top-down and bottom-up approaches have been used to estimate and validate the total size of the machine vision market. These methods have also been used extensively to estimate the size of various subsegments in the market. The following research methodology has been used to estimate the market size:

- Major players in the market have been identified through extensive secondary research.

- The industry’s value chain and market size (in terms of value) have been determined through primary and secondary research processes.

- All percentage shares, splits, and breakdowns have been determined using secondary sources and verified through primary sources.

Machine Vision Market : Top-Down and Bottom-Up Approach

Data Triangulation

After arriving at the overall size of the machine vision market from the market size estimation process explained above, the total market has been split into several segments and subsegments. Data triangulation and market breakdown procedures have been employed, wherever applicable, to complete the overall market engineering process and arrive at the exact statistics for all segments and subsegments of the market. The data has been triangulated by studying various factors and trends from both the demand and supply sides. Along with this, the market size has been validated using both the top-down and bottom-up approaches.

Market Definition

Machine vision systems use a combination of hardware and software to provide operational guidance to devices in executing their functions. Visual inspections are automated, and product assembly equipment are precisely guided using sensors (cameras), processing hardware, and software algorithms. The system relies on digital sensors installed in cameras with specialized optics to acquire images. These images are then processed, analyzed, and measured by artificial intelligence (AI) technology embedded in the computer hardware for decision-making. AI allows machines to learn from experience, intercept new inputs, and perform human-like tasks. Machine learning and natural language processing (NLP), used to train computers, are also used in machine vision to perform specific tasks by processing large data captured by cameras. Machine vision systems offer fast response, a tailored approach, accurate information, and fewer redundancies—all essential to achieving higher organizational efficiency. Machine vision systems encompass all industrial and non-industrial applications.

Key Stakeholders

- Government bodies and policymakers

- Industry organizations, forums, alliances, and associations

- Raw material suppliers and distributors

- Research institutes and organizations

- Original equipment manufacturers (OEMs)

- Technology, service, and solution providers

- Intellectual property (IP) core and licensing providers

- Market research and consulting firms

Report Objectives

- To describe, segment, and forecast the overall machine vision market by application, vision type, deployment, component, system type, and industry, in terms of value

- To describe and forecast the market for four key regions: North America, Europe, Asia Pacific, and Rest of the World (RoW), along with their respective countries, in terms of value

- To provide an overview of the recent trends in the market

- To provide detailed information regarding the drivers, restraints, opportunities, and challenges influencing the growth of the market

- To analyze the supply chain, trends/disruptions impacting customer business, market/ecosystem map, pricing analysis, and regulatory landscape pertaining to the machine vision market

- To strategically analyze micromarkets with respect to individual growth trends, prospects, and contributions to the overall market size.

- To analyze opportunities in the market for stakeholders and provide a competitive landscape of the market

- To strategically profile the key players and comprehensively analyze their market positions in terms of their ranking and core competencies, along with detailing the competitive landscape for market leaders

- To analyze competitive developments, such as product launches, acquisitions, collaborations, agreements, and partnerships, in the machine vision market

- To provide ecosystem analysis, case study analysis, patent analysis, technology analysis, value chain analysis, trends/disruptions impacting customer business, impact of AI/Gen AI, key conferences and events, pricing analysis, Porter’s five forces analysis, and regulations pertaining to the market under study

- To provide a macroeconomic outlook based on all the regions in the region chapter

Available Customizations:

With the given market data, MarketsandMarkets offers customizations according to the company’s specific needs. The following customization options are available for the report:

Company Information:

- Detailed analysis and profiling of additional market players (up to 5)

Key Questions Addressed by the Report

What is the current size of the Machine Vision Market?

The global Machine Vision Market is estimated at USD 15.83 billion in 2025.

What is the projected market size by 2030?

The market is expected to reach USD 23.63 billion by 2030, driven by increasing industrial automation and AI-powered inspection systems.

What is the CAGR of the Machine Vision Market?

The Machine Vision Market is projected to grow at a CAGR of 8.3% from 2025 to 2030.

What are the key growth drivers of the Machine Vision Market?

Major drivers include industrial automation, automated quality assurance, Industry 4.0 adoption, AI integration, and rising demand for high-precision inspection.

Which industry is the largest adopter of machine vision systems?

The electronics and semiconductor industry is a major adopter due to the need for high-precision inspection and defect detection.

How is AI influencing the Machine Vision Market?

AI and deep learning improve object recognition, defect detection, predictive maintenance, and real-time quality control in manufacturing environments.

Which machine vision technology segment is growing the fastest?

3D machine vision systems are witnessing rapid growth due to their ability to inspect complex shapes and support robotic guidance applications.

Which region dominates the Machine Vision Market?

Asia Pacific holds the largest market share, supported by strong manufacturing activity in China, Japan, South Korea, and India.

Who are the leading companies in the Machine Vision Market?

Key companies include Cognex Corporation, Keyence Corporation, OMRON Corporation, Basler AG, Teledyne Technologies, National Instruments, and SICK AG.

What are the major trends shaping the Machine Vision Market?

Key trends include AI-powered vision systems, smart factory deployment, edge computing, vision-guided robotics, and advanced 3D imaging technologies.

Fact checked

Personalize This Research

- Triangulate with your Own Data

- Get Data as per your Format and Definition

- Gain a Deeper Dive on a Specific Application, Geography, Customer or Competitor

- Any level of Personalization

Let Us Help You

- What are the Known and Unknown Adjacencies Impacting the Machine Vision Market

- What will your New Revenue Sources be?

- Who will be your Top Customer; what will make them switch?

- Defend your Market Share or Win Competitors

- Get a Scorecard for Target Partners

Custom Market Research Services

We Will Customise The Research For You, In Case The Report Listed Above Does Not Meet With Your Requirements

Get 10% Free CustomisationTESTIMONIALS

Tetsuya Ohhira

Business Development Manager-Technology Business

Nikon Corporation,

Leading Japanese MNC specializing in optics and imaging productswww.nikon.com

MarketsandMarkets™ response

is quick. Their attitude is flexible and positive. Analyst Insights are globally considered and

significant. Client Services quickly respond to our inquiry and demand. Their wide range of global

surveys help us make our strategic plan.

We hope Knowledge Store will be easier to search

for a report.

VP - Marketing & Business Development

Leading Provider of Process Control Solutions

We engaged with MarketsandMarkets on a study to perform an analysis and recommend a Go-To-Market strategy for metrology and process control in the semiconductor market. The study was tailored to our targets and needs with well-defined milestones. Our overall experience with the MarketsandMarkets team was very good throughout the project in all aspects including the analysis methodologies used, the quality and depth of primary and secondary data sets, the professionalism and flexibility of the team and the ability to meet the target schedule and milestones. We want to thank MarketsandMarkets team for a job well done.

- US Machine Vision Market

- Canada Machine Vision Market

- Mexico Machine Vision Market

- Germany Machine Vision Market

- UK Machine Vision Market

- France Machine Vision Market

- Italy Machine Vision Market

- Spain Machine Vision Market

- Netherlands Machine Vision Market

- Switzerland Machine Vision Market

- China Machine Vision Market

- Japan Machine Vision Market

- South Korea Machine Vision Market

- India Machine Vision Market

- Indonesia Machine Vision Market

- Singapore Machine Vision Market

- Australia Machine Vision Market

- Nordics Machine Vision Market

- Rest Of Europe Machine Vision Market

- Rest Of Asia Pacific Machine Vision Market

- Bahrain Machine Vision Market

- Kuwait Machine Vision Market

Growth opportunities and latent adjacency in Machine Vision Market

Clark

Apr, 2026

How is deep learning transforming machine vision from rule-based inspection to intelligent decision-making?.

Samuel

Apr, 2026

What�s driving the rapid growth of machine vision in Asia Pacific automation, electronics manufacturing, or labor dynamics?.