Download PDF

Download PDF Request Customisation

Request Customisation

Silicon Photonics Market Size, Share and Trends

Report Code

SE 3137

Published in

Apr, 2025, By MarketsandMarkets™

Silicon Photonics Market Size, Share and Trends by Product (Transceivers, Variable Optical Attenuators, Switches, Sensors and Cables), Components (Lasers, Modulators, Optical Waveguides, Optical Interconnects, Photodetectors) - Global Forecast to 2030

USD 9.65

MARKET SIZE,2030

CAGR 29.5%

(2025-2030)

300

REPORT PAGES

221

MARKET TABLES

Silicon Photonics Market Overview

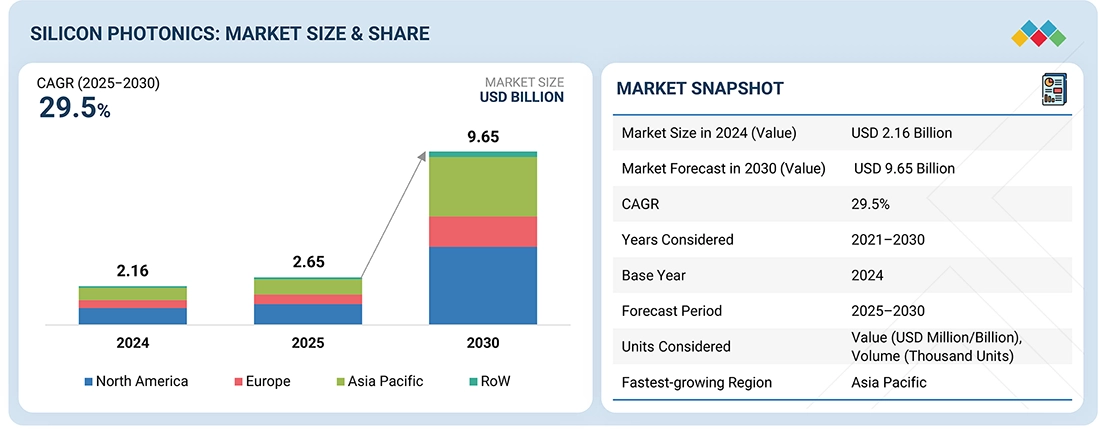

According to Marketsandmarkets, the silicon photonics market size was valued at USD 2.16 billion in 2024 and is projected to reach USD 9.65 billion by 2030, growing at a CAGR of 29.5% from 2025 to 2030. Silicon photonics is experiencing strong growth due to the increasing demand for high-speed data transmission in AI, cloud computing, and quantum technologies. Trends indicate data centres, telecommunication, and healthcare are driving the adoption in a boom, and transceivers and high-performance computing (HPC) are the most positively affected positively.

REPORT SCOPE

| REPORT METRIC | DETAILS |

|---|---|

| Market Size, 2025 (Value) | USD 2.65 Billion |

| Market Forecast, 2030 (Value) | USD 9.65 Billion |

| Growth Rate | CAGR of 29.5% from 2025 to 2030 |

| Years Considered | 2022–2030 |

| Base Year | 2024 |

| Forecast Period | 2025–2030 |

| Units Considered | Value (USD Million/Billion), Volume (Thousand Units) |

| Report Coverage | Revenue Forecast, Company Ranking, Competitive Landscape, Growth Factors, and Trends |

| Top Companies |

|

| Growth Driver |

|

| Segments Covered |

|

| Regions Covered | North America, Asia Pacific, Europe, Rest of the World (RoW) |

Market Size & Forecast

• 2024 Market Size: USD 2.16 Billion

• 2030 Projected Market Size: USD 9.65 Billion

• CAGR (2024-2030): 29.5%

• Data Centers and HPC segment: Highest CAGR

• Asia Pacific: Fastest Growing Region

SILICON PHOTONICS MARKET KEY TAKEAWAYS

-

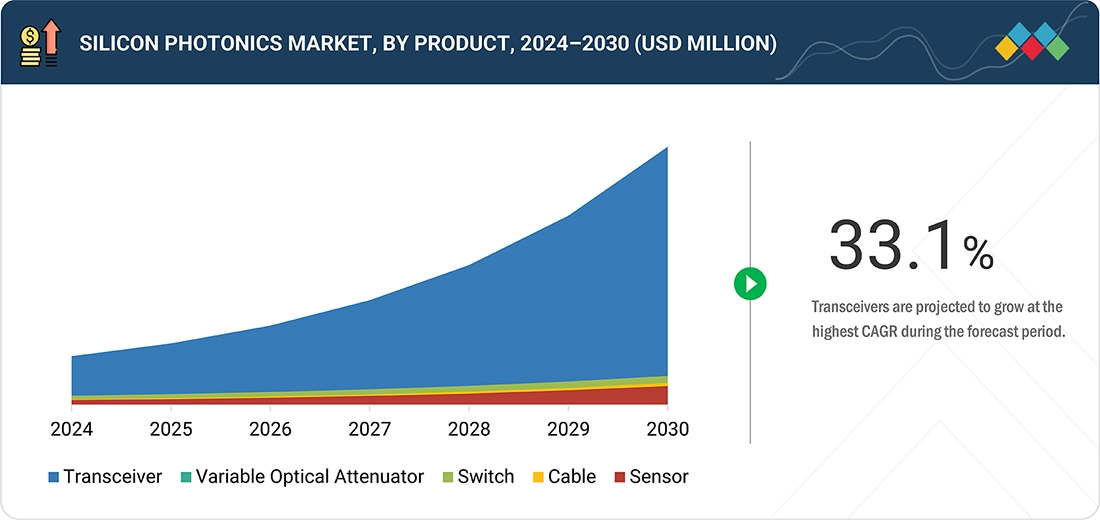

BY PRODUCTTransceivers are expected to have the largest market size during the forecast period. Transceivers are used in various end users, such as data centres and HPC, and telecommunications, owing to the growing need for high-speed data transmission in data center.

-

BY COMPONENTThe market for lasers is expected to grow at the highest CAGR during the forecast period. Lasers are an essential component in silicon photonics as they are used to generate and transmit light signals over long distances. The demand for high-speed data transmission and communication is expected to drive silicon photonics market growth, and lasers will play a critical role in enabling this technology

-

BY END USERThe data centers and HPC segment is projected to grow at the highest CAGR during the forecast period. WAN and LAN are used for metro and long-haul applications in telecommunications, and LAN is used in the data communication end-use segment.

-

BY REGIONNorth America is dominating the silicon photonics market by capturing the largest market share owing to the presence of major players providing silicon photonics technology-based devices in the US and the high adoption of electronic products.

-

COMPETITIVE LANDSCAPECisco Systems, Inc. (US), Intel Corporation (US), MACOM (US), GlobalFoundries Inc. (US), and Lumentum Operations LLC (US) are major players in the market. Major market players have adopted both organic and inorganic strategies, including partnerships and investments.

The silicon photonics market share has been growing strongly as demands for high-bandwidth, low-latency and energy-efficient data communication increase. It is gradually shifting from niche applications into mainstream infrastructure, especially in data center, telecommunications, and AI/ML workloads where traditional copper interconnects are facing power, heat and speed limitations.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

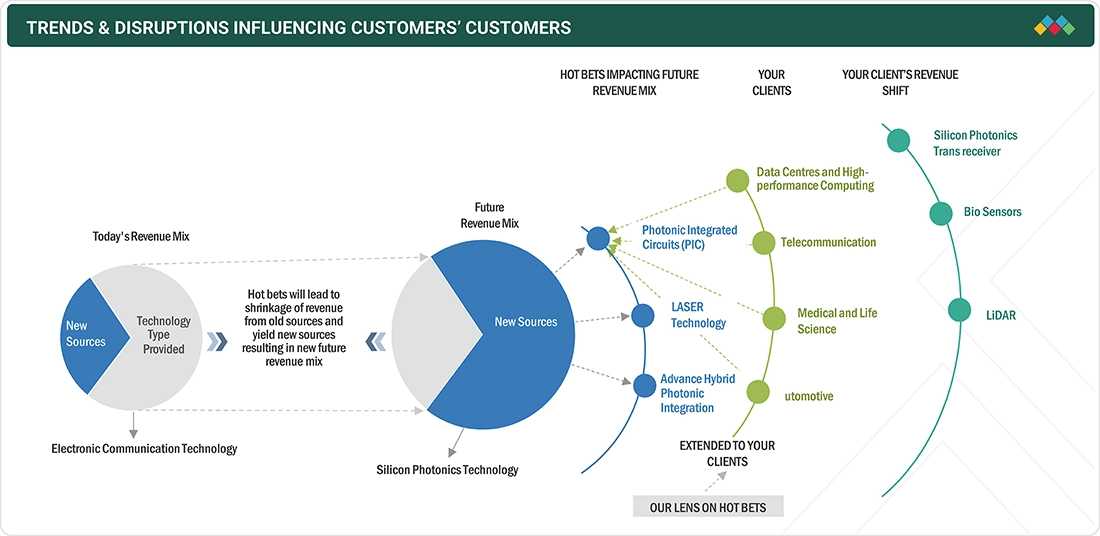

TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' CUSTOMERS

The fig represents the revenue shift expected in the silicon photonics market trends. Communication is happening with electronic components, and electronic technology dominates in terms of value in the silicon photonics market. However, due to technological advancements, there is an increasing demand for high-speed data transmission in data centers and other applications, which is expected to lead to the rise of silicon photonics technology. Data centers, telecommunications, and medical and life sciences are a few industries that will experience a boost in market size. Silicon photonics transceivers, biosensors, and LIDAR demand will increase soon.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

SILICON PHOTONICS MARKET DYNAMICS

Drivers

Impact

Level

Level

-

Growing need for high bandwidth and fast data transfer

-

Growing focus on energy efficiency and lower power costs

RESTRAINTS

Impact

Level

Level

-

Complexities associated with integrating on-chip lasers

OPPORTUNITIES

Impact

Level

Level

-

Ongoing advancements in quantum photonics

-

Expansion of 5G networks

CHALLENGES

Impact

Level

Level

-

Rising thermal effects due to miniaturization of devices

-

Inefficient electroluminescence of bulk crystalline silicon

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Driver: Growing need for high bandwidth and fast data transfer

Rising volumes of streaming, cloud computing and AI workloads are pushing demand for data transfer capacities that far exceed what traditional copper interconnects can efficiently support. Silicon photonics offers a way out of this bottleneck by embedding optical components into silicon chips, enabling much faster and more energy-efficient data exchange, especially in hyperscale data centers and telecom networks. With roll-outs of 5G/6G, advances in photonic integration and economies of scale, the market for silicon photonics is accelerating rapidly as more sectors embrace high-speed, low-latency digital infrastructure.

Restraint: Ongoing advancements in quantum photonics

The integration of on-chip lasers remains a thorny technical hurdle for silicon photonics. Because silicon itself is an indirect bandgap material, it emits light poorly, so achieving efficient, reliable lasers on silicon requires incorporation of III-V semiconductors or complex hybrid techniques—with wafer bonding, flip-chip assembly or epitaxial growth—that complicate fabrication, raise costs and reduce yield. Further challenges like controlling thermal effects, managing reflections, ensuring accurate alignment, and keeping the process CMOS compatible all deepen the difficulty, so many commercial systems still rely on external lasers despite the loss of compactness, power savings, and full integration.

Opportunity: Rising thermal effects due to miniaturization of devices

Quantum photonics presents a powerful frontier for silicon photonics by enabling the generation, control, and manipulation of individual photons on a chip — critical for ultra-secure communications, quantum cryptography, and information processing. Researchers have recently shown progress in creating single-photon emitters in silicon (such as G and W centers) and designing microring or resonator-based sources with high spectral purity, which are steps toward integrating complex quantum circuits. Coupled with the use of mature CMOS-compatible manufacturing and foundry-scale production, these advances promise to bring quantum photonic systems out of the laboratory and into practical, scalable, high-performance applications.

Challenge: Rising thermal effects due to miniaturization of devices

As silicon photonics technology advances towards miniaturization and integration, thermal effects have become a significant challenge. The dense integration of components like modulators, waveguides, and detectors on a single chip leads to localized heating, which can alter the refractive index of silicon, resulting in signal drift, phase errors, or data loss. Unlike electronics, photonic devices are temperature-sensitive and require precise thermal management to maintain control and stability.

SILICON PHOTONICS MARKET SIZE, SHARE & GROWTH: COMMERCIAL USE CASES ACROSS INDUSTRIES

| COMPANY | USE CASE DESCRIPTION | BENEFITS |

|---|---|---|

|

Data center optical transceivers and integrated optical interconnects for AI workloads | High-speed data transfer, reduced latency, improved energy efficiency, scalable optical I/O closer to CPU |

|

High-speed optical interconnects integrated into networking equipment, enabled by Luxtera acquisition | Enhanced bandwidth for data centers and internet infrastructure, faster network speeds, improved network scalability |

|

Silicon photonics-based optical components for telecom and hyperscale data communications | Enables high-capacity optical networking, lower power consumption, increased network reliability |

|

Advanced silicon photonics in software-defined networking and high-speed switches | Improved network performance, efficient bandwidth management, agile data routing |

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

SILICON PHOTONICS MARKET ECOSYSTEM

The silicon photonics market growth ecosystem is characterized by photonic-integrated circuit (PIC) designers, silicon-on-insulator (SOI) substrate providers, epi wafer suppliers, foundries and fabs, transceiver integrators, equipment providers, and end users. PIC designers leverage SOI substrates and epi wafer technologies to integrate optical and electronic functions on a single chip. Foundries and fabs, such as GlobalFoundries and TSMC, play a crucial role by utilizing established semiconductor manufacturing processes to produce advanced PICS. Transceiver integrators incorporate essential optical components, such as modulators, detectors, and waveguides, onto a single silicon substrate. End users are from telecommunications, data centers, and HPC medical & life sciences fields.

Logos and trademarks shown above are the property of their respective owners. Their use here is for informational and illustrative purposes only.

SILICON PHOTONICS MARKET SEGMENTS

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

Silicon Photonics Market, By Produt Type

Transceiver in the product segment to hold largest market share throughout the forecast period.The transceiver industry is the largest in the silicon photonics industry primarily due to its inherent role in delivering high-speed data transmission in high-performance computing, telecommunications, and data centers. Silicon photonic transceivers offer several benefits over traditional electronic transceivers, including higher bandwidth, lower latency, and lower power consumption, that are critical in meeting the rising demand for higher speed and efficient data transmission

Silicon Photonics Market, By Component

Optical interconnects to have the highest CAGR during the forecast period. An optical interconnect is a technology that uses light (photons) transmitted through silicon-based waveguides to transfer data between different parts of an electronic system, such as between chips, servers, or data centers. Unlike traditional electrical interconnects that rely on copper wires to transmit electrical signals, optical interconnects use light, enabling faster and more energy-efficient data transfer with minimal signal loss over long distances.

Silicon Photonics Market, By End User

Data Centers and HPC are expected to have the highest growth rate during the forecast period.Data Centers and HPC include end users such as data centers and HPC Trans receivers, 5G trans receivers, photo processing, CPO, and optical interconnect. A data center and HPC is a facility consisting of networked computers and storage systems that many organizations use to organize, process, store, and disseminate large volumes of data. Businesses rely heavily on services, end users, and data in data centers, making it a critical asset for day-to-day operations.

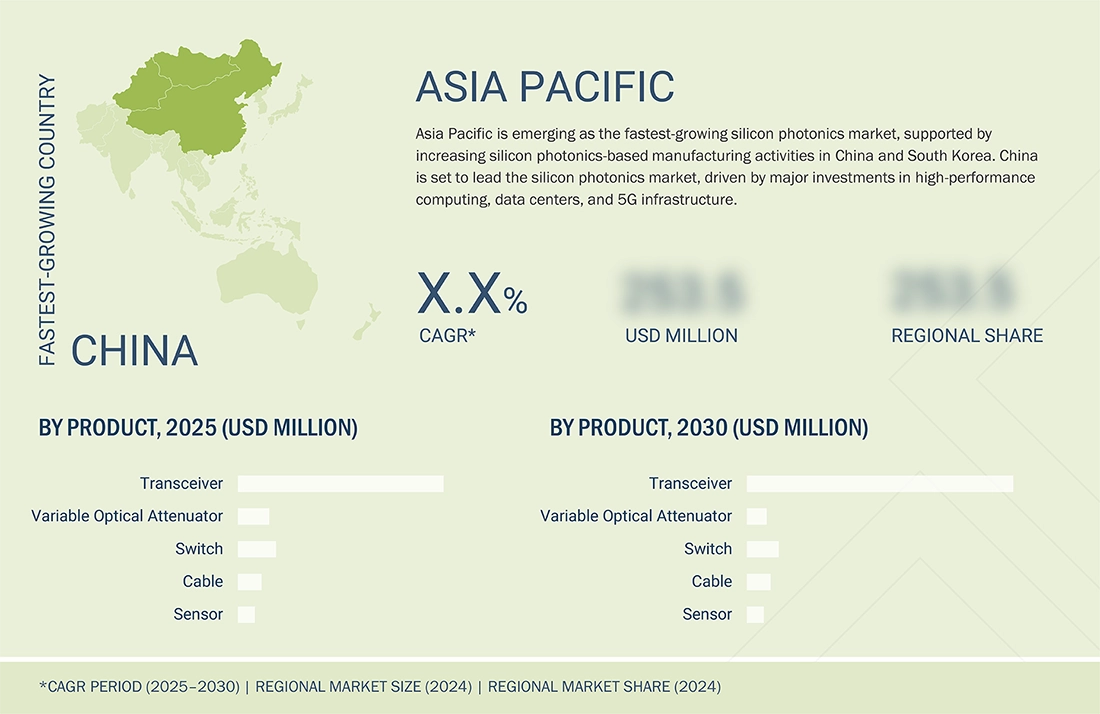

SILICON PHOTONICS MARKET REGION

Asia Pacific to be fastest-growing region in global silicon photonics market during forecast period

The silicon photonics industry in Asia Pacific is expected to grow at the highest rate during the forecast period. The market in Asia Pacific has been segmented into China, Japan, South Korea, and Rest of Asia Pacific. The Rest of Asia Pacific mainly includes India, Australia, New Zealand, Singapore, Malaysia, the Philippines, and Taiwan. China is to record the largest market size within the silicon photonics industry, with revenue forecast to The fast-paced growth is powered by China's aggressive investment in high-performance computing, data centers, and 5G infrastructure, which represent key applications of silicon photonics technology.

The silicon photonics market in North America is projected to reach USD 4.35 billion by 2030, up from USD 1.16 billion in 2030, at a CAGR of 30.2% from 2025 to 2030. Silicon photonics is gaining significant momentum in North America as technology companies and data-center operators increasingly adopt high-speed, low-power optical connectivity. The region benefits from a mature semiconductor ecosystem, substantial R&D investments, and early adoption of AI and cloud computing workloads. Its expanding integration into applications like telecom networks, HPC systems, and advanced sensing further drives market growth.

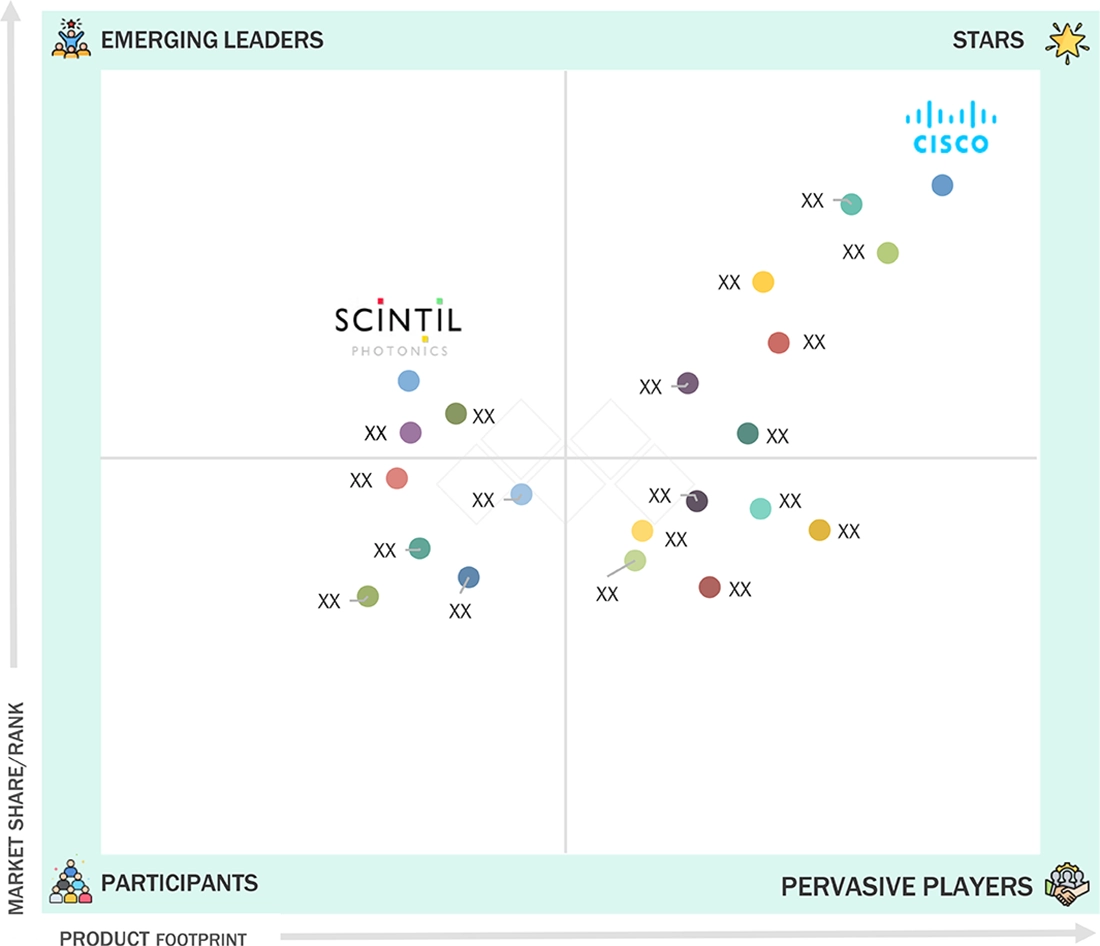

SILICON PHOTONICS MARKET SIZE, SHARE & GROWTH: COMPANY EVALUATION MATRIX

Star companies generally receive high scores for most evaluation criteria. They have a robust product portfolio, strong market presence, high market share, and effective business strategies. Major star companies in the silicon photonics companies are Cisco Systems, Inc. (US). Players categorized as emerging leaders are the vendors who have demonstrated substantial product innovations compared to their competitors. These players mainly depend on investments and funding from other companies. SCINTIL Photonics (France) falls under this category.

Source: Secondary Research, Interviews with Experts, MarketsandMarkets Analysis

SILICON PHOTONICS MARKET KEY PLAYERS

WHAT IS IN IT FOR YOU: Silicon Photonics Market REPORT CONTENT GUIDE

DELIVERED CUSTOMIZATIONS

We have successfully delivered the following deep-dive customizations:

| CLIENT REQUEST | CUSTOMIZATION DELIVERED | VALUE ADDS |

|---|---|---|

| Data Center/Hyperscale OEM |

|

|

| Photonics Component Manufacturer |

|

Pinpoint highest-growth applications, address integration |

| Defense & Government Programs |

|

|

RECENT DEVELOPMENTS

- December 2024 : IBM (US) unveiled a new process for CPO that would enhance data center connectivity by integrating optical waveguides with silicon photonics. This technology was designed to replace traditional electrical interconnects, potentially speeding up data center training for generative AI models by up to five times. The use of polymer optical waveguides (PWGs) allowed for a higher density of optical fibers, up to six times more at the chip edge, improving bandwidth significantly and extending cable lengths from one meter to hundreds of meters.

- November 2024 : Celestial AI (US) acquired Rockley Photonics' (US) silicon photonics intellectual property (IP) portfolio for USD 20 million. This acquisition included worldwide issued and pending patents related to optoelectronic systems-in-package, electro-absorption modulators (EAMs), and optical switch technology. The integration of Rockley's IP enhanced Celestial AI's Photonic Fabric technology platform, which targeted AI data center infrastructure applications.

- October 2024 : Lumentum (US) participated in the European Conference on Optical Communication (ECOC) 2024, highlighting its enhanced 800G ZR+ coherent pluggable transceivers. These transceivers were optimized for extended reach and higher optical power applications, addressing the growing demands of AI infrastructure and long-reach data center interconnects. The transceivers leveraged Lumentum's proprietary indium phosphide technology for superior performance.

- March 2024 : MACOM (US) launched MACOM PURE DRIVE 200 Gbps per lane Liner Drive to enable the development of 1.6 TB linear pluggable optical (LPO) modules.

Table of Contents

![]() Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

Exclusive indicates content/data unique to MarketsandMarkets and not available with any competitors.

TITLE

PAGE NO

1

INTRODUCTION

23

2

RESEARCH METHODOLOGY

27

3

EXECUTIVE SUMMARY

38

4

PREMIUM INSIGHTS

41

5

MARKET OVERVIEW

Silicon photonics market growth fueled by 5G expansion and energy-efficient high-bandwidth solutions.

44

5.1

INTRODUCTION

5.2

MARKET DYNAMICS

5.2.1

DRIVERS

5.2.1.1

SURGING DEMAND FOR CMOS-INTEGRATED SILICON PHOTONICS

5.2.1.2

GROWING FOCUS ON ENERGY EFFICIENCY AND LOWER POWER COSTS

5.2.1.3

RISING DEMAND FOR HIGH BANDWIDTH AND FAST DATA TRANSFER

5.2.1.4

EXPANSION OF BROADBAND SERVICES

5.2.2

RESTRAINTS

5.2.2.1

COMPLEXITIES OF INTEGRATING LASER SOURCES ON SILICON CHIPS

5.2.3

OPPORTUNITIES

5.2.3.1

GOVERNMENT FUNDING FOR DEVELOPING ADVANCED SILICON PHOTONICS-BASED PRODUCTS

5.2.3.2

EXPANSION OF 5G NETWORKS

5.2.3.3

EXPANDING APPLICATIONS OF SILICON PHOTONICS

5.2.3.4

INCREASING USE OF SILICON PHOTONICS IN SHORT-DISTANCE COMMUNICATION

5.2.4

CHALLENGES

5.2.4.1

INEFFICIENT ELECTROLUMINESCENCE OF BULK CRYSTALLINE SILICON

5.2.4.2

THERMAL CHALLENGES IN DEVICE MINIATURIZATION AND COMPLEXITY

5.3

TECHNOLOGY ANALYSIS

5.3.1

KEY TECHNOLOGIES

5.3.1.1

SILICON PHOTONICS TECHNOLOGY

5.3.2

COMPLEMENTARY TECHNOLOGIES

5.3.2.1

AI- AND IOT-INTEGRATED 5G NETWORKS

5.3.3

ADJACENT TECHNOLOGIES

5.3.3.1

LASER TECHNOLOGIES

5.4

TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.5

PRICING ANALYSIS

5.5.1

AVERAGE SELLING PRICE TREND OF TRANSCEIVERS, BY DATA RATE, 2018–2024

5.5.2

AVERAGE SELLING PRICE TREND OF TRANSCEIVERS, BY REGION, 2018–2024

5.6

VALUE CHAIN ANALYSIS

5.7

ECOSYSTEM ANALYSIS

5.8

INVESTMENT AND FUNDING SCENARIO

5.9

PATENT ANALYSIS

5.10

TRADE ANALYSIS

5.10.1

IMPORT SCENARIO (HS CODE 851769)

5.10.2

EXPORT SCENARIO (HS CODE 851769)

5.11

TARIFF AND REGULATORY LANDSCAPE

5.11.1

TARIFF ANALYSIS

5.11.2

REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.11.3

STANDARDS

5.11.3.1

INTERNATIONAL ORGANIZATION FOR STANDARDIZATION STANDARDS

5.11.3.2

EUROPEAN UNION DIRECTIVES

5.11.3.3

FEDERAL COMMUNICATION COMMISSION (FCC)

5.11.3.4

NATIONAL INSTITUTE OF STANDARDS AND TECHNOLOGY GUIDELINES

5.12

KEY CONFERENCES AND EVENTS, 2025–2026

5.13

CASE STUDY ANALYSIS

5.13.1

COHERENT PLUGGABLE TRANSCEIVER HELPS TELIA CARRIER (SWEDEN) ACHIEVE HIGH-SPEED TRANSMISSION

5.13.2

MOLEX DATA CABLES SOLUTION IMPROVES DATA TRANSMISSION ISSUES OF KALINGA GROUP

5.13.3

QSFPTEK'S 100G QSFP28 TRANSCEIVERS HELP EMPOWER CRITICAL BUSINESSES

5.14

PORTER'S FIVE FORCES ANALYSIS

5.14.1

INTENSITY OF COMPETITIVE RIVALRY

5.14.2

BARGAINING POWER OF SUPPLIERS

5.14.3

BARGAINING POWER OF BUYERS

5.14.4

THREAT OF SUBSTITUTES

5.14.5

THREAT OF NEW ENTRANTS

5.15

KEY STAKEHOLDERS AND BUYING CRITERIA

5.15.1

KEY STAKEHOLDERS IN BUYING PROCESS

5.15.2

BUYING CRITERIA

5.16

IMPACT OF AI ON SILICON PHOTONICS MARKET

5.17

IMPACT OF 2025 US TARIFF ON MARKET

5.17.1

INTRODUCTION

5.17.2

KEY TARIFF RATES

5.17.3

PRICE IMPACT ANALYSIS

5.17.4

KEY IMPACTS ON VARIOUS REGIONS

5.17.4.1

US

5.17.4.2

EUROPE

5.17.4.3

ASIA PACIFIC

5.17.5

IMPACT ON END-USE INDUSTRIES

6

WAVEGUIDES IN SILICON PHOTONICS

Silicon photonics waveguides revolutionize healthcare, telecom, and LIDAR with expansive wavelength applications.

80

6.1

INTRODUCTION

6.2

400–1,500 NM

6.2.1

USE IN HEALTHCARE DIAGNOSTICS TO DRIVE MARKET

6.3

1,310–1,550 NM

6.3.1

DEPLOYMENT IN DATA CENTERS AND TELECOMMUNICATIONS TO BOOST MARKET

6.4

900–7,000 NM

6.4.1

UTILIZATION IN LIDAR AND GAS SENSORS TO FUEL MARKET GROWTH

7

SILICON PHOTONICS MARKET, BY COMPONENT

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 14 Data Tables

82

7.1

INTRODUCTION

7.2

LASERS

7.2.1

SURGING UTILIZATION IN PHOTONIC DEVICES TO ENSURE HIGH-SPEED DATA TRANSMISSION TO SPUR DEMAND

7.3

MODULATORS

7.3.1

GROWING REQUIREMENT FOR HIGH-SPEED NETWORKS TO ACCELERATE MARKET GROWTH

7.4

PHOTODETECTORS

7.4.1

STRONG ABSORPTION IN NIR WAVELENGTH RANGE TO SUPPORT MARKET GROWTH

7.5

OPTICAL WAVEGUIDES

7.5.1

INCREASING STRATEGIC DEVELOPMENT BY KEY PLAYERS TO FAVOR MARKET GROWTH

7.6

OPTICAL INTERCONNECTS

7.6.1

HIGH AND MORE EFFICIENT DATA TRANSFER RATES AND HIGH INTERCONNECTION DENSITIES TO AUGMENT MARKET GROWTH

7.7

OTHER COMPONENTS

8

SILICON PHOTONICS MARKET, BY PRODUCT

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million and Units | 56 Data Tables

92

8.1

INTRODUCTION

8.2

TRANSCEIVERS

8.2.1

DATA RATES

8.2.1.1

LESS THAN 10 GBPS

8.2.1.2

UP TO 100 GBPS

8.2.1.3

MORE THAN 100 GBPS

8.3

VARIABLE OPTICAL ATTENUATORS

8.3.1

GROWING ADOPTION OF BROADBAND INTERNET AND DEPLOYMENT OF 5G TO FUEL MARKET GROWTH

8.4

SWITCHES

8.4.1

SURGING USE OF OPTICAL SWITCHES TO ENSURE TRANSMISSION OF LARGE VOLUMES OF DATA IN MINIMAL TIME TO PROPEL MARKET

8.5

CABLES

8.5.1

RISING DEMAND FOR HIGHER BANDWIDTH CAPACITY TO AUGMENT MARKET GROWTH

8.6

SENSORS

8.6.1

ELEVATING DEMAND FOR PORTABLE AND WEARABLE DEVICES TO PROPEL MARKET GROWTH

9

SILICON PHOTONICS MARKET, BY END USER

Market Size & Growth Rate Forecast Analysis to 2030 in USD Million | 22 Data Tables

117

9.1

INTRODUCTION

9.2

DATA CENTERS AND HPC

9.2.1

RAPID GROWTH OF AI AND OTHER MODERN TECHNOLOGIES TO BOOST DEMAND

9.3

TELECOMMUNICATIONS

9.3.1

GROWING NEED TO ACCOMMODATE BANDWIDTH-INTENSIVE PRODUCTS AND SERVICES TO FUEL SEGMENTAL GROWTH

9.4

MILITARY, DEFENSE, AND AEROSPACE

9.4.1

BOOSTING DEFENSE CAPABILITIES WITH CO-PACKAGED OPTICAL INTERCONNECTS TO AUGMENT MARKET GROWTH

9.5

MEDICAL AND LIFE SCIENCES

9.5.1

RISING DEPLOYMENT OF SILICON PHOTONICS IN LAB-ON-CHIP SOLUTIONS TO FUEL DEMAND

9.6

OTHER END USERS

10

SILICON PHOTONICS MARKET, BY REGION

Comprehensive coverage of 10 Regions with country-level deep-dive of 10 Countries | 56 Data Tables.

131

10.1

INTRODUCTION

10.2

NORTH AMERICA

10.2.1

MACROECONOMIC OUTLOOK FOR NORTH AMERICA

10.2.2

US

10.2.2.1

RIGOROUS R&D ACTIVITIES BY KEY INDUSTRY PLAYERS TO DRIVE MARKET

10.2.3

CANADA

10.2.3.1

ACCELERATED DEMAND FOR HIGH-SPEED NETWORKING TO FUEL MARKET GROWTH

10.2.4

MEXICO

10.2.4.1

GOVERNMENT-LED INITIATIVES TO ENSURE CONNECTIVITY WITHIN URBAN CENTERS TO BOOST DEMAND

10.3

EUROPE

10.3.1

MACROECONOMIC OUTLOOK FOR EUROPE

10.3.2

GERMANY

10.3.2.1

GOVERNMENT-LED FUNDING AND INITIATIVES BY VARIOUS RESEARCH INSTITUTES TO FUEL MARKET GROWTH

10.3.3

UK

10.3.3.1

GROWING ADOPTION OF DATA CENTERS AND HPC BY VARIOUS VERTICALS TO FAVOR MARKET GROWTH

10.3.4

FRANCE

10.3.4.1

FEDERAL SUPPORT TO PROMOTE USE OF SILICON PHOTONICS TO AUGMENT MARKET GROWTH

10.3.5

ITALY

10.3.5.1

RISING NUMBER OF DATA CENTERS TO SUPPORT MARKET GROWTH

10.3.6

REST OF EUROPE

10.4

ASIA PACIFIC

10.4.1

MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

10.4.2

CHINA

10.4.2.1

RISING DEMAND FOR SMARTPHONES AND INTERNET USERS TO ACCELERATE MARKET GROWTH

10.4.3

JAPAN

10.4.3.1

EARLY ADOPTION OF SILICON PHOTONICS IN MEDICAL EQUIPMENT TO SUPPORT MARKET GROWTH

10.4.4

SOUTH KOREA

10.4.4.1

TECHNOLOGICAL INNOVATIONS IN SILICON PHOTONICS TO SPUR MARKET GROWTH

10.4.5

REST OF ASIA PACIFIC

10.5

ROW

10.5.1

MACROECONOMIC OUTLOOK FOR ROW

10.5.2

SOUTH AMERICA

10.5.2.1

STRONG GOVERNMENT SUPPORT TO DEVELOP NETWORK INFRASTRUCTURE TO BOOST DEMAND

10.5.3

GCC

10.5.3.1

INCREASING NEED FOR ADVANCED SILICON PHOTONICS-BASED TRANSCEIVERS TO FUEL MARKET GROWTH

10.5.4

REST OF MIDDLE EAST & AFRICA

10.5.4.1

ADOPTION OF 4G IN THE REGION TO DRIVE THE MARKET

11

COMPETITIVE LANDSCAPE

Discover market leaders and emerging contenders reshaping competitive dynamics through strategic growth and innovation.

166

11.1

OVERVIEW

11.2

KEY STRENGTHS/RIGHT TO WIN, 2021–2024

11.3

REVENUE ANALYSIS, 2019–2023

11.4

MARKET SHARE ANALYSIS, 2024

11.5

COMPANY VALUATION AND FINANCIAL METRICS

11.6

PRODUCT/APPLICATION COMPARISON

11.7

COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

11.7.1

STARS

11.7.2

EMERGING LEADERS

11.7.3

PERVASIVE PLAYERS

11.7.4

PARTICIPANTS

11.7.5

COMPANY FOOTPRINT: KEY PLAYERS, 2024

11.7.5.1

COMPANY FOOTPRINT

11.7.5.2

REGION FOOTPRINT

11.7.5.3

COMPONENT FOOTPRINT

11.7.5.4

PRODUCT FOOTPRINT

11.7.5.5

END USER FOOTPRINT

11.8

COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

11.8.1

PROGRESSIVE COMPANIES

11.8.2

RESPONSIVE COMPANIES

11.8.3

DYNAMIC COMPANIES

11.8.4

STARTING BLOCKS

11.8.5

COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

11.8.5.1

DETAILED LIST OF KEY STARTUPS/SMES

11.8.5.2

COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

11.9

COMPETITIVE SCENARIO

11.9.1

PRODUCT LAUNCHES

11.9.2

DEALS

11.9.3

EXPANSIONS

11.9.4

OTHER DEVELOPMENTS

12

COMPANY PROFILES

In-depth Company Profiles of Leading Market Players with detailed Business Overview, Product and Service Portfolio, Recent Developments, and Unique Analyst Perspective (MnM View)

188

12.1

KEY PLAYERS

12.1.1

CISCO SYSTEMS, INC.

12.1.1.1

BUSINESS OVERVIEW

12.1.1.2

PRODUCTS OFFERED

12.1.1.3

RECENT DEVELOPMENTS

12.1.1.4

MNM VIEW

12.1.2

INTEL CORPORATION

12.1.3

MACOM

12.1.4

GLOBAL FOUNDRIES INC.

12.1.5

LUMENTUM HOLDINGS, INC.

12.1.6

MARVELL

12.1.7

COHERENT CORPORATION

12.1.8

IBM

12.1.9

STMICROELECTRONICS

12.1.10

ROCKLEY PHOTONICS HOLDINGS LIMITED

12.2

OTHER PLAYERS

12.2.1

MELLANOX TECHNOLOGIES LTD.

12.2.2

SICOYA GMBH

12.2.3

RANOVUS

12.2.4

BROADCOM INC.

12.2.5

HAMAMATSU PHOTONICS K.K.

12.2.6

MOLEX LLC

12.2.7

FUJITSU LIMITED

12.2.8

CHIRAL PHOTONICS, INC.

12.2.9

EFFECT PHOTONICS

12.2.10

AIO CORE CO., LTD.

12.2.11

NKT PHOTONICS

12.2.12

IPG PHOTONICS CORPORATION

12.2.13

DAS PHOTONICS

12.2.14

TDK CORPORATION

12.2.15

SCINTIL PHOTONICS

12.2.16

TEEM PHOTONICS

12.2.17

LIGHTWAVE LOGIC, INC.

12.2.18

SOURCE PHOTONICS

13

APPENDIX

245

13.1

DISCUSSION GUIDE

13.2

KNOWLEDGESTORE: MARKETSANDMARKETS’ SUBSCRIPTION PORTAL

13.3

CUSTOMIZATION OPTIONS

13.4

RELATED REPORTS

13.5

AUTHOR DETAILS

LIST OF TABLES

TABLE 1

RESEARCH ASSUMPTIONS

TABLE 2

RISK ANALYSIS

TABLE 3

AVERAGE SELLING PRICE TREND OF TRANSCEIVERS, BY DATA RATE, 2018–2023 (USD)

TABLE 4

ROLE OF COMPANIES IN ECOSYSTEM

TABLE 5

SILICON PHOTONICS MARKET: KEY PATENTS, 2020–2024

TABLE 6

IMPORT SCENARIO FOR HS CODE 851769-COMPLIANT PRODUCTS, BY COUNTRY, 2019–2023 (USD THOUSAND)

TABLE 7

EXPORT SCENARIO FOR HS CODE 851769-COMPLIANT PRODUCTS, BY COUNTRY, 2019–2023 (USD THOUSAND)

TABLE 8

TARIFF IMPOSED BY US ON IMPORTS OF TRANSMISSION OR RECEPTION APPARATUS, 2023

TABLE 9

TARIFFS IMPOSED BY UK ON IMPORTS OF TRANSMISSION OR RECEPTION APPARATUS, 2023

TABLE 10

NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 11

EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 12

ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 13

ROW: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

TABLE 14

KEY CONFERENCES AND EVENTS, 2025–2026

TABLE 15

SILICON PHOTONICS MARKET: PORTER'S FIVE FORCES ANALYSIS

TABLE 16

INFLUENCE OF STAKEHOLDERS IN BUYING PROCESS FOR TOP THREE END USERS (%)

TABLE 17

KEY BUYING CRITERIA FOR TOP THREE END USERS

TABLE 18

US ADJUSTED RECIPROCAL TARIFF RATES

TABLE 19

SILICON PHOTONICS MARKET, BY COMPONENT, 2021–2024 (USD MILLION)

TABLE 20

MARKET, BY COMPONENT, 2025–2030 (USD MILLION)

TABLE 21

LASERS: MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 22

LASERS: MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 23

MODULATORS: MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 24

MODULATORS: MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 25

PHOTODETECTORS: MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 26

PHOTODETECTORS: SILICON PHOTONICS MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 27

OPTICAL WAVEGUIDES: MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 28

OPTICAL WAVEGUIDES: MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 29

OPTICAL INTERCONNECTS: MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 30

OPTICAL INTERCONNECTS: MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 31

OTHER COMPONENTS: MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 32

OTHER COMPONENTS: MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 33

SILICON PHOTONICS MARKET, BY PRODUCT, 2021–2024 (USD MILLION)

TABLE 34

MARKET, BY PRODUCT, 2025–2030 (USD MILLION)

TABLE 35

TRANSCEIVERS: MARKET, BY DATA RATE, 2021–2024 (USD MILLION)

TABLE 36

TRANSCEIVERS: MARKET, BY DATA RATE, 2025–2030 (USD MILLION)

TABLE 37

TRANSCEIVERS: MARKET, BY DATA RATE, 2021–2024 (THOUSAND UNITS)

TABLE 38

TRANSCEIVERS: MARKET, BY DATA RATE, 2025–2030 (THOUSAND UNITS)

TABLE 39

TRANSCEIVERS: SILICON PHOTONICS MARKET, BY END USER, 2021–2024 (USD MILLION)

TABLE 40

TRANSCEIVERS: MARKET, BY END USER, 2025–2030 (USD MILLION)

TABLE 41

TRANSCEIVERS: MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 42

TRANSCEIVERS: MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 43

TRANSCEIVERS: MARKET IN DATA CENTERS AND HPC, BY REGION, 2021–2024 (USD MILLION)

TABLE 44

TRANSCEIVERS: MARKET IN DATA CENTERS AND HPC, BY REGION, 2025–2030 (USD MILLION)

TABLE 45

TRANSCEIVERS: SILICON PHOTONICS MARKET IN TELECOMMUNICATIONS, BY REGION, 2021–2024 (USD MILLION)

TABLE 46

TRANSCEIVERS: MARKET IN TELECOMMUNICATIONS, BY REGION, 2025–2030 (USD MILLION)

TABLE 47

TRANSCEIVERS: MARKET IN MILITARY, DEFENSE, AND AEROSPACE, BY REGION, 2021–2024 (USD MILLION)

TABLE 48

TRANSCEIVERS: MARKET IN MILITARY, DEFENSE, AND AEROSPACE, BY REGION, 2025–2030 (USD MILLION)

TABLE 49

VARIABLE OPTICAL ATTENUATORS: MARKET, BY END USER, 2021–2024 (USD MILLION)

TABLE 50

VARIABLE OPTICAL ATTENUATORS: MARKET, BY END USER, 2025–2030 (USD MILLION)

TABLE 51

VARIABLE OPTICAL ATTENUATORS: SILICON PHOTONICS MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 52

VARIABLE OPTICAL ATTENUATORS: MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 53

VARIABLE OPTICAL ATTENUATORS: MARKET IN DATA CENTERS AND HPC, BY REGION, 2021–2024 (USD MILLION)

TABLE 54

VARIABLE OPTICAL ATTENUATORS: SILICON PHOTONICS MARKET IN DATA CENTERS AND HPC, BY REGION, 2025–2030 (USD MILLION)

TABLE 55

VARIABLE OPTICAL ATTENUATORS: MARKET IN TELECOMMUNICATIONS, BY REGION, 2021–2024 (USD MILLION)

TABLE 56

VARIABLE OPTICAL ATTENUATORS: MARKET IN TELECOMMUNICATIONS, BY REGION, 2025–2030 (USD MILLION)

TABLE 57

VARIABLE OPTICAL ATTENUATORS: MARKET IN MILITARY, DEFENSE, AND AEROSPACE, BY REGION, 2021–2024 (USD MILLION)

TABLE 58

VARIABLE OPTICAL ATTENUATORS: MARKET IN MILITARY, DEFENSE, AND AEROSPACE, BY REGION, 2025–2030 (USD MILLION)

TABLE 59

SWITCHES: SILICON PHOTONICS MARKET, BY END USER, 2021–2024 (USD MILLION)

TABLE 60

SWITCHES: MARKET, BY END USER, 2025–2030 (USD MILLION)

TABLE 61

SWITCHES: MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 62

SWITCHES: MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 63

SWITCHES: MARKET IN DATA CENTERS AND HPC, BY REGION, 2021–2024 (USD MILLION)

TABLE 64

SWITCHES: MARKET IN DATA CENTERS AND HPC, BY REGION, 2025–2030 (USD MILLION)

TABLE 65

SWITCHES: MARKET IN TELECOMMUNICATIONS, BY REGION, 2021–2024 (USD MILLION)

TABLE 66

SWITCHES: SILICON PHOTONICS MARKET IN TELECOMMUNICATIONS, BY REGION, 2025–2030 (USD MILLION)

TABLE 67

SWITCHES: MARKET IN MILITARY, DEFENSE, AND AEROSPACE, BY REGION, 2021–2024 (USD MILLION)

TABLE 68

SWITCHES: MARKET IN MILITARY, DEFENSE, AND AEROSPACE, BY REGION, 2025–2030 (USD MILLION)

TABLE 69

CABLES: MARKET, BY END USER, 2021–2024 (USD MILLION)

TABLE 70

CABLES: MARKET, BY END USER, 2025–2030 (USD MILLION)

TABLE 71

CABLES: MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 72

CABLES: MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 73

CABLES: SILICON PHOTONICS MARKET IN DATA CENTERS AND HPC, BY REGION, 2021–2024 (USD MILLION)

TABLE 74

CABLES: MARKET IN DATA CENTERS AND HPC, BY REGION, 2025–2030 (USD MILLION)

TABLE 75

CABLES: MARKET IN TELECOMMUNICATIONS, BY REGION, 2021–2024 (USD MILLION)

TABLE 76

CABLES: MARKET IN TELECOMMUNICATIONS, BY REGION, 2025–2030 (USD MILLION)

TABLE 77

CABLES: MARKET IN MILITARY, DEFENSE, AND AEROSPACE, BY REGION, 2021–2024 (USD MILLION)

TABLE 78

CABLES: MARKET IN MILITARY, DEFENSE, AND AEROSPACE, BY REGION, 2025–2030 (USD MILLION)

TABLE 79

SENSORS: SILICON PHOTONICS MARKET, BY END USER, 2021–2024 (USD MILLION)

TABLE 80

SENSORS: MARKET, BY END USER, 2025–2030 (USD MILLION)

TABLE 81

SENSORS: MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 82

SENSORS: MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 83

SENSORS: MARKET IN MILITARY, DEFENSE, AND AEROSPACE, BY REGION, 2021–2024 (USD MILLION)

TABLE 84

SENSORS: MARKET IN MILITARY, DEFENSE, AND AEROSPACE, BY REGION, 2025–2030 (USD MILLION)

TABLE 85

SENSORS: MARKET IN MEDICAL AND LIFE SCIENCES, BY REGION, 2021–2024 (USD MILLION)

TABLE 86

SENSORS: SILICON PHOTONICS MARKET IN MEDICAL AND LIFE SCIENCES, BY REGION, 2025–2030 (USD MILLION)

TABLE 87

SENSORS: SILICON PHOTONICS IN OTHER END USERS, BY REGION, 2021–2024 (USD MILLION)

TABLE 88

SENSORS: SILICON PHOTONICS IN OTHER END USERS, BY REGION, 2025–2030 (USD MILLION)

TABLE 89

SILICON PHOTONICS MARKET, BY END USER, 2021–2024 (USD MILLION)

TABLE 90

MARKET, BY END USER, 2025–2030 (USD MILLION)

TABLE 91

DATA CENTERS AND HPC: MARKET, BY PRODUCT, 2021–2024 (USD MILLION)

TABLE 92

DATA CENTERS AND HPC: MARKET, BY PRODUCT, 2025–2030 (USD MILLION)

TABLE 93

DATA CENTERS AND HPC: MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 94

DATA CENTERS AND HPC: MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 95

TELECOMMUNICATIONS: SILICON PHOTONICS MARKET, BY PRODUCT, 2021–2024 (USD MILLION)

TABLE 96

TELECOMMUNICATIONS: MARKET, BY PRODUCT, 2025–2030 (USD MILLION)

TABLE 97

TELECOMMUNICATIONS: MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 98

TELECOMMUNICATIONS: MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 99

MILITARY, DEFENSE, AND AEROSPACE: MARKET, BY PRODUCT, 2021–2024 (USD MILLION)

TABLE 100

MILITARY, DEFENSE, AND AEROSPACE: MARKET, BY PRODUCT, 2025–2030 (USD MILLION)

TABLE 101

MILITARY, DEFENSE, AND AEROSPACE: SILICON PHOTONICS MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 102

MILITARY, DEFENSE, AND AEROSPACE: MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 103

MEDICAL AND LIFE SCIENCES: MARKET, BY PRODUCT, 2021–2024 (USD MILLION)

TABLE 104

MEDICAL AND LIFE SCIENCES: MARKET, BY PRODUCT, 2025–2030 (USD MILLION)

TABLE 105

MEDICAL AND LIFE SCIENCES: MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 106

MEDICAL AND LIFE SCIENCES: MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 107

OTHER END USERS: SILICON PHOTONICS MARKET, BY PRODUCT, 2021–2024 (USD MILLION)

TABLE 108

OTHER END USERS: MARKET, BY PRODUCT, 2025–2030 (USD MILLION)

TABLE 109

OTHER END USERS: MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 110

OTHER END USERS: MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 111

SILICON PHOTONICS MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 112

MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 113

NORTH AMERICA: MARKET, BY PRODUCT, 2021–2024 (USD MILLION)

TABLE 114

NORTH AMERICA: MARKET, BY PRODUCT, 2025–2030 (USD MILLION)

TABLE 115

NORTH AMERICA: MARKET, BY END USER, 2021–2024 (USD MILLION)

TABLE 116

NORTH AMERICA: MARKET, BY END USER, 2025–2030 (USD MILLION)

TABLE 117

NORTH AMERICA: SILICON PHOTONICS MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 118

NORTH AMERICA: MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 119

US: MARKET, BY END USER, 2021–2024 (USD MILLION)

TABLE 120

US: MARKET, BY END USER, 2025–2030 (USD MILLION)

TABLE 121

CANADA: MARKET, BY END USER, 2021–2024 (USD MILLION)

TABLE 122

CANADA: MARKET, BY END USER, 2025–2030 (USD MILLION)

TABLE 123

MEXICO: SILICON PHOTONICS MARKET, BY END USER, 2021–2024 (USD MILLION)

TABLE 124

MEXICO: MARKET, BY END USER, 2025–2030 (USD MILLION)

TABLE 125

EUROPE: MARKET, BY PRODUCT, 2021–2024 (USD MILLION)

TABLE 126

EUROPE: MARKET, BY PRODUCT, 2025–2030 (USD MILLION)

TABLE 127

EUROPE: MARKET, BY END USER, 2021–2024 (USD MILLION)

TABLE 128

EUROPE: MARKET, BY END USER, 2025–2030 (USD MILLION)

TABLE 129

EUROPE: SILICON PHOTONICS MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 130

EUROPE: MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 131

GERMANY: MARKET, BY END USER, 2021–2024 (USD MILLION)

TABLE 132

GERMANY: MARKET, BY END USER, 2025–2030 (USD MILLION)

TABLE 133

UK: MARKET, BY END USER, 2021–2024 (USD MILLION)

TABLE 134

UK: MARKET, BY END USER, 2025–2030 (USD MILLION)

TABLE 135

FRANCE: MARKET, BY END USER, 2021–2024 (USD MILLION)

TABLE 136

FRANCE: MARKET, BY END USER, 2025–2030 (USD MILLION)

TABLE 137

ITALY: SILICON PHOTONICS MARKET, BY END USER, 2021–2024 (USD MILLION)

TABLE 138

ITALY: MARKET, BY END USER, 2025–2030 (USD MILLION)

TABLE 139

REST OF EUROPE: MARKET, BY END USER, 2021–2024 (USD MILLION)

TABLE 140

REST OF EUROPE: MARKET, BY END USER, 2025–2030 (USD MILLION)

TABLE 141

ASIA PACIFIC: MARKET, BY PRODUCT, 2021–2024 (USD MILLION)

TABLE 142

ASIA PACIFIC: MARKET, BY PRODUCT, 2025–2030 (USD MILLION)

TABLE 143

ASIA PACIFIC: SILICON PHOTONICS MARKET, BY END USER, 2021–2024 (USD MILLION)

TABLE 144

ASIA PACIFIC: MARKET, BY END USER, 2025–2030 (USD MILLION)

TABLE 145

ASIA PACIFIC: MARKET, BY COUNTRY, 2021–2024 (USD MILLION)

TABLE 146

ASIA PACIFIC: MARKET, BY COUNTRY, 2025–2030 (USD MILLION)

TABLE 147

CHINA: MARKET, BY END USER, 2021–2024 (USD MILLION)

TABLE 148

CHINA: SILICON PHOTONICS MARKET, BY END USER, 2025–2030 (USD MILLION)

TABLE 149

JAPAN: MARKET, BY END USER, 2021–2024 (USD MILLION)

TABLE 150

JAPAN: MARKET, BY END USER, 2025–2030 (USD MILLION)

TABLE 151

SOUTH KOREA: MARKET, BY END USER, 2021–2024 (USD MILLION)

TABLE 152

SOUTH KOREA: MARKET, BY END USER, 2025–2030 (USD MILLION)

TABLE 153

REST OF ASIA PACIFIC: SILICON PHOTONICS MARKET, BY END USER, 2021–2024 (USD MILLION)

TABLE 154

REST OF ASIA PACIFIC: MARKET, BY END USER, 2025–2030 (USD MILLION)

TABLE 155

ROW: MARKET, BY PRODUCT, 2021–2024 (USD MILLION)

TABLE 156

ROW: MARKET, BY PRODUCT, 2025–2030 (USD MILLION)

TABLE 157

ROW: MARKET, BY END USER, 2021–2024 (USD MILLION)

TABLE 158

ROW: SILICON PHOTONICS MARKET, BY END USER, 2025–2030 (USD MILLION)

TABLE 159

ROW: MARKET, BY REGION, 2021–2024 (USD MILLION)

TABLE 160

ROW: MARKET, BY REGION, 2025–2030 (USD MILLION)

TABLE 161

SOUTH AMERICA: MARKET, BY END USER, 2021–2024 (USD MILLION)

TABLE 162

SOUTH AMERICA: SILICON PHOTONICS MARKET, BY END USER, 2025–2030 (USD MILLION)

TABLE 163

GCC COUNTRIES: MARKET, BY END USER, 2021–2024 (USD MILLION)

TABLE 164

GCC COUNTRIES: MARKET, BY END USER, 2025–2030 (USD MILLION)

TABLE 165

REST OF MIDDLE EAST & AFRICA: MARKET, BY END USER, 2021–2024 (USD MILLION)

TABLE 166

REST OF MIDDLE EAST & AFRICA: MARKET, BY END USER, 2025–2030 (USD MILLION)

TABLE 167

SILICON PHOTONICS MARKET: OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS, 2021–2024

TABLE 168

MARKET: DEGREE OF COMPETITION, 2024

TABLE 169

MARKET: REGION FOOTPRINT

TABLE 170

MARKET: COMPONENT FOOTPRINT

TABLE 171

SILICON PHOTONICS MARKET: PRODUCT FOOTPRINT

TABLE 172

MARKET: END USER FOOTPRINT

TABLE 173

STARTUP MATRIX: DETAILED LIST OF KEY STARTUPS/SMES

TABLE 174

MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

TABLE 175

MARKET: PRODUCT LAUNCHES, MARCH 2020–FEBRUARY 2025

TABLE 176

SILICON PHOTONICS MARKET: DEALS, MARCH 2020–FEBRUARY 2025

TABLE 177

MARKET: EXPANSIONS, MARCH 2020–FEBRUARY 2025

TABLE 178

MARKET: OTHER DEVELOPMENTS, MARCH 2020–FEBRUARY 2025

TABLE 179

CISCO SYSTEMS INC.: COMPANY OVERVIEW

TABLE 180

CISCO SYSTEMS, INC.: PRODUCTS OFFERED

TABLE 181

CISCO SYSTEMS, INC.: PRODUCT LAUNCHES

TABLE 182

CISCO SYSTEMS, INC.: DEALS

TABLE 183

INTEL CORPORATION: COMPANY OVERVIEW

TABLE 184

INTEL CORPORATION: PRODUCTS OFFERED

TABLE 185

INTEL CORPORATION: PRODUCT LAUNCHES

TABLE 186

INTEL CORPORATION: DEALS

TABLE 187

MACOM: COMPANY OVERVIEW

TABLE 188

MACOM: PRODUCTS OFFERED

TABLE 189

MACOM: PRODUCT LAUNCHES

TABLE 190

MACOM: DEALS

TABLE 191

MACOM: OTHER DEVELOPMENTS

TABLE 192

GLOBALFOUNDRIES INC.: COMPANY OVERVIEW

TABLE 193

GLOBALFOUNDRIES INC.: PRODUCTS OFFERED

TABLE 194

GLOBALFOUNDRIES INC.: PRODUCT LAUNCHES

TABLE 195

GLOBALFOUNDRIES INC.: DEALS

TABLE 196

GLOBALFOUNDRIES INC.: OTHER DEVELOPMENTS

TABLE 197

LUMENTUM HOLDINGS, INC.: COMPANY OVERVIEW

TABLE 198

LUMENTUM HOLDINGS, INC.: PRODUCTS OFFERED

TABLE 199

LUMENTUM HOLDINGS, INC.: PRODUCT LAUNCHES

TABLE 200

LUMENTUM HOLDINGS, INC.: DEALS

TABLE 201

LUMENTUM HOLDINGS, INC.: EXPANSIONS

TABLE 202

MARVELL: COMPANY OVERVIEW

TABLE 203

MARVELL: PRODUCTS OFFERED

TABLE 204

MARVELL: PRODUCT LAUNCHES

TABLE 205

MARVELL: DEALS

TABLE 206

MARVELL: EXPANSIONS

TABLE 207

COHERENT CORPORATION: COMPANY OVERVIEW

TABLE 208

COHERENT CORPORATION: PRODUCTS OFFERED

TABLE 209

COHERENT CORPORATION: PRODUCT LAUNCHES

TABLE 210

COHERENT CORPORATION: DEALS

TABLE 211

IBM: COMPANY OVERVIEW

TABLE 212

IBM: PRODUCTS OFFERED

TABLE 213

IBM: PRODUCT LAUNCHES

TABLE 214

STMICROELECTRONICS: COMPANY OVERVIEW

TABLE 215

STMICROELECTRONICS: PRODUCTS OFFERED

TABLE 216

STMICROELECTRONICS: PRODUCT LAUNCHES

TABLE 217

STMICROELECTRONICS: DEALS

TABLE 218

ROCKLEY PHOTONICS HOLDINGS LIMITED: COMPANY OVERVIEW

TABLE 219

ROCKLEY PHOTONICS: PRODUCTS OFFERED

TABLE 220

ROCKLEY PHOTONICS HOLDINGS LIMITED: PRODUCT LAUNCHES

TABLE 221

ROCKLEY PHOTONICS HOLDINGS LIMITED: DEALS

LIST OF FIGURES

FIGURE 1

SILICON PHOTONICS MARKET SEGMENTATION

FIGURE 2

MARKET: RESEARCH FLOW

FIGURE 3

MARKET: RESEARCH DESIGN

FIGURE 4

MARKET SIZE ESTIMATION METHODOLOGY

FIGURE 5

BOTTOM-UP APPROACH

FIGURE 6

TOP-DOWN APPROACH

FIGURE 7

SILICON PHOTONICS MARKET: DATA TRIANGULATION

FIGURE 8

TRANSCEIVERS TO REGISTER HIGHEST CAGR IN MARKET DURING FORECAST PERIOD

FIGURE 9

LASER SEGMENT TO ACCOUNT FOR LARGEST SHARE OF MARKET DURING FORECAST PERIOD

FIGURE 10

DATA CENTERS AND HPC TO REGISTER HIGHEST CAGR IN MARKET DURING FORECAST PERIOD

FIGURE 11

NORTH AMERICA ACCOUNTED FOR LARGEST SHARE OF SILICON PHOTONICS MARKET IN 2024

FIGURE 12

RISING DEMAND FOR SILICON PHOTONICS TECHNOLOGY-BASED PRODUCTS FROM DATA CENTERS AND HPC TO DRIVE MARKET

FIGURE 13

DATA CENTERS AND HPC SEGMENT ACCOUNTED FOR LARGEST MARKET SHARE IN 2024

FIGURE 14

US ACCOUNTED FOR LARGEST SHARE OF MARKET IN NORTH AMERICA IN 2024

FIGURE 15

LASERS TO DOMINATE MARKET DURING FORECAST PERIOD

FIGURE 16

CHINA TO EXHIBIT HIGHEST CAGR IN GLOBAL SILICON PHOTONICS MARKET DURING FORECAST PERIOD

FIGURE 17

MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

FIGURE 18

MARKET DRIVERS AND THEIR IMPACT

FIGURE 19

GLOBAL Y-O-Y GROWTH OF INTERNET USERS, 2014–2024

FIGURE 20

SILICON PHOTONICS MARKET RESTRAINTS AND THEIR IMPACT

FIGURE 21

MARKET OPPORTUNITIES AND THEIR IMPACT

FIGURE 22

MARKET CHALLENGES AND THEIR IMPACT

FIGURE 23

TRENDS/DISRUPTIONS INFLUENCING CUSTOMER BUSINESS

FIGURE 24

AVERAGE SELLING PRICE TREND OF TRANSCEIVERS, BY DATA RATE, 2018–2024

FIGURE 25

AVERAGE SELLING PRICE TREND FOR TRANSCEIVERS FOR DIFFERENT DATA RATES, BY KEY PLAYERS, 2024

FIGURE 26

AVERAGE SELLING PRICE TREND OF TRANSCEIVERS, BY REGION, 2018–2024

FIGURE 27

SILICON PHOTONICS MARKET: VALUE CHAIN ANALYSIS

FIGURE 28

MARKET: ECOSYSTEM ANALYSIS

FIGURE 29

FUNDING SCENARIO FOR TRANSCEIVERS, 2019–2024

FIGURE 30

PATENTS APPLIED AND GRANTED, 2014–2025

FIGURE 31

IMPORT DATA FOR HS CODE 851769-COMPLIANT PRODUCTS FOR TOP FIVE COUNTRIES, 2019–2023

FIGURE 32

EXPORT DATA FOR HS CODE 851769-COMPLIANT PRODUCTS FOR TOP FIVE COUNTRIES, 2019–2023

FIGURE 33

SILICON PHOTONICS MARKET: PORTER'S FIVE FORCES ANALYSIS

FIGURE 34

INFLUENCE OF STAKEHOLDERS IN BUYING PROCESS FOR TOP THREE END USERS

FIGURE 35

KEY BUYING CRITERIA FOR TOP THREE END USERS

FIGURE 36

SILICON PHOTONICS MARKET: IMPACT OF AI

FIGURE 37

MARKET, BY COMPONENT

FIGURE 38

OPTICAL WAVEGUIDE SEGMENT TO WITNESS HIGHEST CAGR IN MARKET DURING FORECAST PERIOD

FIGURE 39

SILICON PHOTONICS MARKET, BY PRODUCT

FIGURE 40

TRANSCEIVERS SEGMENT TO REGISTER HIGHEST CAGR IN MARKET DURING FORECAST PERIOD

FIGURE 41

MARKET, BY END USER

FIGURE 42

DATA CENTERS AND HPC SEGMENT TO WITNESS HIGHEST CAGR DURING FORECAST PERIOD

FIGURE 43

SILICON PHOTONICS MARKET: BY REGION

FIGURE 44

CHINA TO REGISTER HIGHEST CAGR IN GLOBAL MARKET FROM 2025 TO 2030

FIGURE 45

NORTH AMERICA: SILICON PHOTONICS MARKET, BY COUNTRY

FIGURE 46

NORTH AMERICA: MARKET SNAPSHOT

FIGURE 47

EUROPE: MARKET, BY COUNTRY

FIGURE 48

EUROPE: SILICON PHOTONICS MARKET SNAPSHOT

FIGURE 49

ASIA PACIFIC: MARKET, BY COUNTRY

FIGURE 50

ASIA PACIFIC: MARKET SNAPSHOT

FIGURE 51

MARKET: REVENUE ANALYSIS OF TOP FIVE KEY PLAYERS, 2019–2023

FIGURE 52

SILICON PHOTONICS MARKET SHARE ANALYSIS, 2024

FIGURE 53

COMPANY VALUATION, 2025

FIGURE 54

EV/EBITDA OF KEY VENDORS, 2025

FIGURE 55

SILICON PHOTONICS MARKET: PRODUCT/APPLICATION COMPARISON

FIGURE 56

MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2023

FIGURE 57

MARKET: COMPANY FOOTPRINT

FIGURE 58

SILICON PHOTONICS MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

FIGURE 59

CISCO SYSTEMS INC.: COMPANY SNAPSHOT

FIGURE 60

INTEL CORPORATION: COMPANY SNAPSHOT

FIGURE 61

MACOM: COMPANY SNAPSHOT

FIGURE 62

GLOBALFOUNDRIES INC.: COMPANY SNAPSHOT

FIGURE 63

LUMENTUM HOLDINGS, INC.: COMPANY SNAPSHOT

FIGURE 64

MARVELL: COMPANY SNAPSHOT

FIGURE 65

COHERENT CORPORATION: COMPANY SNAPSHOT

FIGURE 66

IBM: COMPANY SNAPSHOT

FIGURE 67

STMICROELECTRONICS: COMPANY SNAPSHOT

Methodology

The study involved four major activities in estimating the current size of the global Silicon Photonics market—exhaustive secondary research collected information on the market and its peer and parent markets. The next step was to validate these findings, assumptions, and sizing with industry experts across the value chain through primary research. Both top-down and bottom-up approaches were employed to estimate the total market size. After that, market breakdown and data triangulation were used to estimate the market size of segments and subsegments.

Secondary Research

Various secondary sources have been referred to in the secondary research process to identify and collect important information for this study. These secondary sources include silicon photonics technology journals and magazines, annual reports, press releases, investor presentations of companies, white papers, certified publications and articles from recognized authors, and directories and databases such as Factiva, Hoovers, and OneSource.

Primary Research

Various primary sources from the supply and demand sides have been interviewed in the primary research process to obtain qualitative and quantitative information important for this report. The primary sources from the supply side included industry experts such as CEOs, VPs, marketing directors, technology and innovation directors, and related executives from key companies and organizations operating in the silicon photonics market. After complete market engineering (including calculations regarding market statistics, market breakdown, market size estimations, market forecasting, and data triangulation), extensive primary research was conducted to gather information as well as to verify and validate the critical numbers arrived at.

Note: Other designations include sales, marketing, and product managers. Tier 1 = USD 1 billion, Tier 2 = USD 0.5–1.0 billion, and Tier 3 = USD 0.5 billion.

To know about the assumptions considered for the study, download the pdf brochure

Market Size Estimation

In the complete market engineering process, top-down and bottom-up approaches and several data triangulation methods have been implemented to estimate and validate the size of the silicon photonics market and other dependent submarkets listed in this report.

- Extensive secondary research has identified key players in the industry and market.

- In terms of value, the industry’s supply chain and market size have been determined through primary and secondary research processes.

- All percentage shares, splits, and breakdowns have been determined using secondary sources and verified through primary sources.

Silicon Photonics Market : Top-Down and Bottom-Up Approach

Data Triangulation

After arriving at the overall market size from the estimation process explained above, the global market has been split into several segments and subsegments. Market breakdown and data triangulation procedures have been employed wherever applicable to complete the overall market engineering process and arrive at exact statistics for all segments and subsegments. The data has been triangulated by studying various factors and trends identified from both the demand and supply sides.

Market Definition

Silicon photonics is a technique that employs semiconductor-grade silicon to integrate photonic circuits and electronic components on a single microchip. This method minimizes system power consumption while increasing transmission bandwidth by employing silicon as an optical medium. Instead of electrical impulses, the technology transfers data using optical beams, which may send enormous amounts of data at a faster rate than electrical signals.

Key Stakeholders

- Component and material providers

- Semiconductor foundries

- Silicon photonics platform developers

- Silicon photonics product manufacturers and suppliers

- Assembly and testing vendors

- Original equipment manufacturers

- Research organizations and consulting companies

- Technology investors

- Associations, alliances, and organizations related to silicon photonics

- Analysts and strategic business planners

- End users

Report Objectives

- To describe and forecast the silicon photonics market size, in terms of value, by product, component, end user, and region

- To describe and forecast the market size across four key regions, namely, North America, Europe, Asia Pacific, and the Rest of the World (RoW), along with their respective country-level market size, in terms of value

- To provide details regarding the silicon photonic waveguide range

- To provide detailed information regarding the drivers, restraints, opportunities, and challenges of the silicon photonics market

- To strategically analyze the micromarkets1 concerning the individual growth trends, prospects, and their contribution to the silicon photonics market

- To map competitive intelligence based on company profiles, key player strategies, and key developments

- To provide a detailed overview of the silicon photonics value chain and ecosystem

- To provide information about the key technology trends and patents related to the silicon photonics market

- To provide information regarding trade data related to the silicon photonics market

- To analyze opportunities in the market for stakeholders by identifying high-growth segments of the silicon photonics ecosystem

- To benchmark the market players using the proprietary company evaluation matrix framework, which analyzes them on various parameters within the broad categories of market ranking/share and product portfolio

- To analyze competitive developments such as contracts, acquisitions, product launches and developments, collaborations, and partnerships, along with research & development (R&D), in the silicon photonics market

- To analyze the impact of the recession on the growth of the silicon photonics market

Available Customizations

With the given market data, MarketsandMarkets offers customizations according to a company’s specific needs. The following customization options are available for the report:

Company Information:

- Detailed analysis and profiling of additional market players (up to 5)

Key Questions Addressed by the Report

What is the current size of the Silicon Photonics Market?

The global Silicon Photonics Market was valued at approximately USD 2.16 billion in 2024 and is expected to grow significantly over the forecast period due to increasing demand for high-speed optical communication technologies.

What is the projected market size of the Silicon Photonics Market by 2030?

The market is projected to reach USD 9.65 billion by 2030, growing at a CAGR of 29.5% during 2025–2030.

What are the major growth drivers of the Silicon Photonics Market?

Key growth drivers include rising demand for high-bandwidth data transmission, expansion of AI and cloud computing infrastructure, increasing deployment of data centers, growth of 5G networks, and demand for energy-efficient communication systems.

Which product segment holds the largest share of the Silicon Photonics Market?

Transceivers are expected to account for the largest market share because of their extensive use in data centers, high-performance computing (HPC), and telecommunications applications.

Which component segment is expected to grow the fastest?

The lasers segment is projected to witness the highest CAGR during the forecast period due to its critical role in generating and transmitting optical signals for high-speed communication networks.

Which end-user industry is expected to grow at the highest rate?

Data Centers & High-Performance Computing (HPC) are expected to register the highest growth rate due to increasing AI workloads, cloud services, and demand for ultra-fast optical interconnects.

Which region dominates the Silicon Photonics Market?

North America currently holds the largest market share, supported by strong semiconductor ecosystems, leading technology companies, substantial R&D investments, and widespread adoption of cloud and AI technologies.

Which region is expected to witness the fastest growth during the forecast period?

Asia Pacific is expected to be the fastest-growing region, driven by investments in data centers, 5G infrastructure, high-performance computing, and semiconductor manufacturing, particularly in China, Japan, South Korea, and India.

Who are the leading companies operating in the Silicon Photonics Market?

Major players include Cisco Systems, Intel Corporation, MACOM, GlobalFoundries, and Lumentum Operations LLC. These companies are actively investing in product innovation, partnerships, and capacity expansion.

What are the key trends shaping the Silicon Photonics Market?

Major trends include adoption of optical interconnects, AI-driven data center expansion, co-packaged optics (CPO), quantum computing applications, energy-efficient networking, CMOS-integrated photonics, and next-generation high-speed optical modules.

Need a Tailored Report?

Customize this report to your needs

Get 10% FREE Customization

Customize This Report

Fact checked

Personalize This Research

- Triangulate with your Own Data

- Get Data as per your Format and Definition

- Gain a Deeper Dive on a Specific Application, Geography, Customer or Competitor

- Any level of Personalization

Let Us Help You

- What are the Known and Unknown Adjacencies Impacting the Silicon Photonics Market

- What will your New Revenue Sources be?

- Who will be your Top Customer; what will make them switch?

- Defend your Market Share or Win Competitors

- Get a Scorecard for Target Partners

Custom Market Research Services

We Will Customise The Research For You, In Case The Report Listed Above Does Not Meet With Your Requirements

Get 10% Free CustomisationTESTIMONIALS

Tetsuya Ohhira

Business Development Manager-Technology Business

Nikon Corporation,

Leading Japanese MNC specializing in optics and imaging productswww.nikon.com

MarketsandMarkets™ response

is quick. Their attitude is flexible and positive. Analyst Insights are globally considered and

significant. Client Services quickly respond to our inquiry and demand. Their wide range of global

surveys help us make our strategic plan.

We hope Knowledge Store will be easier to search

for a report.

VP - Marketing & Business Development

Leading Provider of Process Control Solutions

We engaged with MarketsandMarkets on a study to perform an analysis and recommend a Go-To-Market strategy for metrology and process control in the semiconductor market. The study was tailored to our targets and needs with well-defined milestones. Our overall experience with the MarketsandMarkets team was very good throughout the project in all aspects including the analysis methodologies used, the quality and depth of primary and secondary data sets, the professionalism and flexibility of the team and the ability to meet the target schedule and milestones. We want to thank MarketsandMarkets team for a job well done.

- US Silicon Photonics Market

- Canada Silicon Photonics Market

- Mexico Silicon Photonics Market

- Germany Silicon Photonics Market

- UK Silicon Photonics Market

- France Silicon Photonics Market

- Italy Silicon Photonics Market

- China Silicon Photonics Market

- Japan Silicon Photonics Market

- South Korea Silicon Photonics Market

Growth opportunities and latent adjacency in Silicon Photonics Market

VITTORIO

Oct, 2009

Dear Team Members, as an interviewed expert for this matter, I ask you to receive a PDF copy of the summary for this report. .

Angelica

Jan, 2019

I work in the field of silicon photonics components, and I am interested in receiving report specifically mentioning the market size for sensing component and automotive end user vertical. .

Bruce

Apr, 2026

Why is silicon photonics important for modern Data Centers and high-performance computing (HPC)?.

Brian

Apr, 2026

How does silicon photonics improve bandwidth and energy efficiency compared to traditional electronic interconnects?.

Kenneth

Apr, 2026

What are the key applications of silicon photonics in telecommunications, healthcare, and defense sectors?.

richard

Dec, 2009

Interested in silicon photonics market. Your report may receive beneficial publicity in a feature that I am due to write very soon. But I need free access for a limited period for this to happen..

richard

Mar, 2015

Need information on silicon photonic companies and their business models - service or product oriented ? .

Rapha�l

Sep, 2019

My objective is to assess the market in which I'll soon work into, see which business segment is likely to grow the most, and how fast?.

Suzanne

Aug, 2018

Dear sir/madam, just a quick question about the report. We would like to know if we are mentioned in this report. Could you provide me with that information? .

Jeremy

Aug, 2011

I'm a student interested in photonics and learning about the field and what opportunities there are within it. I'm interested in the building blocks of silicon photonics, silicon photonics technology trends, a general market overview. I'm also interested in silicon optical interconnects and photovoltaics, as well as information on HP, Intel, Oracle, and Translucent. .

Yung

Mar, 2019

As an optical engineer, I am very much interested in the market of SIP. I believe this report can help us to analyze that if it is worth to develop the SIP in our own company..

Giuseppe

Feb, 2014

Need information on Silicon Photonics Market by Products (Silicon Optical Interconnects & Wavelength Division Multiplexer Filters & Others), Applications (Telecommunication, Datacom, High Performance Computing & Others) & Geography - Analysis & Forecast (2013 - 2020)..

Jaci

Jun, 2010

We are looking for the following on the Overall Photonics Market: market size, market growth, major players, various segments within Photonics (& their relative sizes and growth)..

Carlos

Nov, 2018

Hello, I would like to buy the corporate license of the silicon photonics report so that I can share it with all the members of our association. I am interested in acquiring 3-6 reports per year from you..

Linda

Oct, 2015

I would like to obtain an old report on this topic from 2010-2014 for research purposes. .

Sevil

Oct, 2022

I need this analysis in order to make an impactful presentation and a review paper on silicon photonics. .

Christian

Jul, 2015

My group is working in the area of silicon photonics and integrated optics, and we are analyzing the potential of commercializing our research. To this end, a copy of the report of an executive summary would be extremely helpful. .

Rudy

Jan, 2019

Objective is to obtain a better market picture of how silicon photonics technology will impact fiber data center links..